Wells Fargo 2009 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2009 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

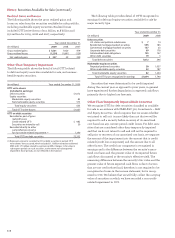

Note 1: Summary of Significant Accounting Policies (continued)

is indicated if the sum of undiscounted estimated future

net cash flows is less than the carrying value of the asset.

Impairment is permanently recognized by writing down the

asset to the extent that the carrying value exceeds the

estimated fair value.

Operating Lease Assets

Operating lease rental income for leased assets is recognized

in other income on a straight-line basis over the lease term.

Related depreciation expense is recorded on a straight-line

basis over the life of the lease, taking into account the esti-

mated residual value of the leased asset. On a periodic basis,

leased assets are reviewed for impairment. Impairment loss is

recognized if the carrying amount of leased assets exceeds

fair value and is not recoverable. The carrying amount of

leased assets is not recoverable if it exceeds the sum of the

undiscounted cash flows expected to result from the lease

payments and the estimated residual value upon the eventual

disposition of the equipment. Leased assets are written down

to the fair value of the collateral less cost to sell when 120

days past due.

Pension Accounting

We account for our defined benefit pension plans using

an actuarial model required by accounting guidance on

retirement benefits. This model allocates pension costs over

the service period of employees in the plan. The underlying

principle is that employees render service ratably over this

period and, therefore, the income statement effects of

pensions should follow a similar pattern.

In 2008, we began measuring our plan assets and benefit

obligations using a year-end measurement date. The change

in the accounting provisions for retirement benefits did

not change the amount of net periodic benefit expense

recognized in our income statement.

One of the principal components of the net periodic

pension expense calculation is the expected long-term rate

of return on plan assets. The use of an expected long-term

rate of return on plan assets may cause us to recognize

pension income returns that are greater or less than the

actual returns of plan assets in any given year.

The expected long-term rate of return is designed to

approximate the actual long-term rate of return over time

and is not expected to change significantly. Therefore, the

pattern of income/expense recognition should closely match

the stable pattern of services provided by our employees over

the life of our pension obligation. To ensure that the expected

rate of return is reasonable, we consider such factors as

(1) long-term historical return experience for major asset

class categories (for example, large cap and small cap

domestic equities, international equities and domestic fixed

income), and (2) forward-looking return expectations for

these major asset classes. Differences between expected and

actual returns in each year, if any, are included in our net

actuarial gain or loss amount, which is recognized in OCI.

We generally amortize any net actuarial gain or loss in excess

of a 5% corridor in net periodic pension expense calculations

over the next 13 years.

We use a discount rate to determine the present value of

our future benefit obligations. The discount rate reflects the

rates available at the measurement date on long-term high-

quality fixed-income debt instruments and is reset annually

on the measurement date. In 2008, we changed our measure-

ment date from November 30 to December 31 as required by

accounting guidance on retirement benefits.

Income Taxes

We file consolidated and separate company federal income

tax returns, foreign tax returns and various combined and

separate company state tax returns.

We account for income taxes in accordance with the

Income Taxes topic of the Codification, which requires two

components of income tax expense: current and deferred.

Current income tax expense approximates taxes to be paid

or refunded for the current period and includes income tax

expense related to our uncertain tax positions. We determine

deferred income taxes using the balance sheet method. Under

this method, the net deferred tax asset or liability is based on

the tax effects of the differences between the book and tax

bases of assets and liabilities, and recognizes enacted

changes in tax rates and laws in the period in which they

occur. Deferred income tax expense results from changes in

deferred tax assets and liabilities between periods. Deferred

tax assets are recognized subject to management’s judgment

that realization is more likely than not. A tax position that

meets the “more likely than not” recognition threshold is

measured to determine the amount of benefit to recognize.

The tax position is measured at the largest amount of benefit

that is greater than 50% likely of being realized upon settle-

ment. Foreign taxes paid are generally applied as credits to

reduce federal income taxes payable. Interest and penalties

are recognized as a component of income tax expense.

Stock-Based Compensation

We have stock-based employee compensation plans as more

fully discussed in Note 18 in this Report. Under accounting

guidance for stock compensation, compensation cost recog-

nized includes cost for all share-based awards.

Earnings Per Common Share

We compute earnings per common share by dividing net

income (after deducting dividends on preferred stock) by the

average number of common shares outstanding during the

year. We compute diluted earnings per common share by

dividing net income (after deducting dividends and related

accretion on preferred stock) by the average number of

common shares outstanding during the year, plus the effect

of common stock equivalents (for example, stock options,

restricted share rights, convertible debentures and warrants)

that are dilutive.