Wells Fargo 2009 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2009 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

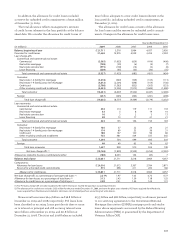

|

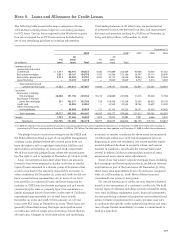

|

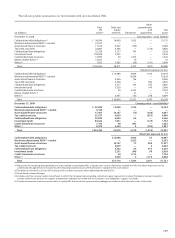

December 31,

(in millions) 2009 2008

Commercial and commercial real estate:

Commercial $187,319 195,507

Real estate mortgage 5,138 6,536

Real estate construction 9,385 19,063

Total commercial and

commercial real estate 201,842 221,106

Consumer:

Real estate 1-4 family first mortgage 33,460 36,964

Real estate 1-4 family junior lien mortgage 63,338 78,417

Credit card 65,952 75,776

Other revolving credit and installment 20,778 22,231

Total consumer 183,528 213,388

Foreign 4,468 4,817

Total unfunded loan commitments $389,838 439,311

Note 6: Loans and Allowance for Credit Losses (continued)

A commitment to extend credit is a legally binding agree-

ment to lend funds to a customer, usually at a stated interest

rate and for a specified purpose. These commitments have

fixed expiration dates and generally require a fee. When we

make such a commitment, we have credit risk. The liquidity

requirements or credit risk will be lower than the contractual

amount of commitments to extend credit because a signifi-

cant portion of these commitments are expected to expire

without being used. Certain commitments are subject to loan

agreements with covenants regarding the financial perfor-

mance of the customer or borrowing base formulas that must

be met before we are required to fund the commitment. We

use the same credit policies in extending credit for unfunded

commitments and letters of credit that we use in making

loans. See Note 14 in this Report for information on standby

letters of credit.

In addition, we manage the potential risk in credit commit-

ments by limiting the total amount of arrangements, both by

individual customer and in total, by monitoring the size and

maturity structure of these portfolios and by applying the

same credit standards for all of our credit activities.

The total of our unfunded loan commitments, net of all

funds lent and all standby and commercial letters of credit

issued under the terms of these commitments, is summarized

by loan category in the following table:

We have an established process to determine the adequacy

of the allowance for credit losses that assesses the risks and

losses inherent in our portfolio. While we attribute portions

of the allowance to specific loan categories as part of our ana-

lytical process, the entire allowance is used to absorb credit

losses inherent in the total loan portfolio.

At December 31, 2009, the portion of the allowance for

credit losses estimated at a pooled level for consumer loans

and some segments of commercial small business loans was

$16.7 billion. For purposes of determining the allowance for

credit losses, we pool certain loans in our portfolio by product

type, primarily for the auto, credit card and real estate mortgage

portfolios. To achieve greater accuracy, we further segment

selected portfolios. As appropriate, the business groups may

attempt to achieve greater accuracy through segmentation by

sub-product, origination channel, vintage, loss type, geography

and other predictive characteristics. For example, credit cards

are segmented by origination channel and the Home Equity

portfolios into liquidating and nonliquidating portfolios. In the

case of residential mortgages, we segment the liquidating Pick-

a-Pay portfolio, and further segment the remainder of the

residential mortgage portfolio based on origination channel.

To measure losses inherent in consumer loans and some

commercial small business loans, we use loss models and

other quantitative, mathematical techniques. Each business

group estimates losses for loans as of the balance sheet date

over the loss emergence period. During fourth quarter 2008,

we conformed our loss emergence period for these portfolios

to cover 12 months of estimated losses, which is within

Federal Financial Institutions Examination Council (FFIEC)

guidelines and resulted in a $2.7 billion increase to the

allowance for credit losses in 2008.

In determining the appropriate allowance attributable

to our residential real estate portfolios, the loss rates used

in our analysis include the impacts of our established loan

modification programs. When modifications occur or are

probable to occur, our allowance considers the impact of

these modifications, taking into consideration the associated

credit cost, including re-defaults of modified loans and pro-

jected loss severity. The loss content associated with existing

and probable loan modifications has been considered in our

allowance reserving methodology.

The portion of the allowance for commercial, CRE,

and foreign loans and lease financing was $8.3 billion at

December 31, 2009. We initially estimate this portion of the

allowance by applying historical loss factors statistically

derived from tracking losses associated with actual portfolio

movements over a specified period of time, for each specific

loan grade. Based on this process, we assign loss factors to

each pool of graded loans and a loan equivalent amount for

unfunded loan commitments and letters of credit. These esti-

mates are then adjusted or supplemented where necessary

from additional analysis of long-term average loss experience,

external loss data or other risks identified from current condi-

tions and trends in selected portfolios, including management’s

judgment for imprecision and uncertainty.

We also assess and account for certain nonaccrual

commercial, CRE, and foreign loan exposures that are over

$5 million and certain consumer, commercial, CRE, and for-

eign loans whose terms have been modified in a TDR as

impaired. We include the impairment on these nonperforming

loans in the allowance unless it has already been recognized as

a loss. At December 31, 2009, we included $2.8 billion in the

allowance related to these impaired loans, which is included

in other components of the allowance described above.

Reflected in the portions of the allowance previously

described is an amount for imprecision or uncertainty that

incorporates the range of probable outcomes inherent in

estimates used for the allowance, which may change from

period to period. This amount is the result of our judgment

of risks inherent in the portfolios, economic uncertainties,

historical loss experience and other subjective factors,

including industry trends, calculated to better reflect our

view of risk in each loan portfolio.