Wells Fargo 2009 Annual Report Download

Download and view the complete annual report

Please find the complete 2009 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Wells Fargo & Company Annual Report 2009

The vision

that works

Table of contents

-

Page 1

Wells Fargo & Company Annual Report 2009 The vision that works -

Page 2

...services company - community-based and relationship-oriented. Our corporate headquarters is in San Francisco, but all our "convenience points" - stores, regional commercial banking centers, ATMs, Wells Fargo Phone Bank,SM internet - are headquarters for satisfying all our customers' ï¬nancial needs... -

Page 3

... The Vision That Works: For Our Communities 31 Board of Directors, Senior Leaders 33 Financial Review 88 Controls and Procedures 90 Financial Statements 186 Report of Independent Registered Public Accounting Firm 191 Stock Performance We want to satisfy all our customers' ï¬nancial needs and help... -

Page 4

... had two other successful stock offerings since November 2008 totaling $21.2 billion, showing strong shareholder support for our company's business model and earnings potential. Total raised in 14 months: $33 billion. • • • Helped reduce mortgage payments for 1.2 million homeowners through... -

Page 5

... auto loans, part of our home equity portfolio, small business loans and lines of consumer credit. Wells Fargo-Wachovia merger: better than expected We're now in the middle innings of the integration of Wachovia and Wells Fargo - the largest, most complex banking merger in U.S. history. It's adding... -

Page 6

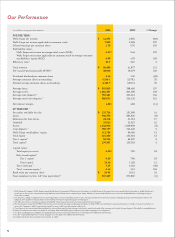

... Diluted average common shares outstanding Average loans Average assets Average core deposits 5 Average retail core deposits 6 Net interest margin AT YEAR END Securities available for sale Loans Allowance for loan losses Goodwill Assets Core deposits 5 Wells Fargo stockholders' equity Total equity... -

Page 7

... Wachovia product across Community Banking - our Way2Save® account. It's a savings account that can be linked to checking, turning purchases into automatic savings by transferring $1 from checking to the Way2Save® account each time you make a check card purchase or use Wells Fargo Bill Pay. Credit... -

Page 8

... attracted new customers and earned more business from current customers. When the economy picks up, so will loan demand, and we'll earn even more of our customers' business. Our Wholesale team leads our company in cross-sell. Our average Wholesale relationship (legacy Wells Fargo) has 6.4 products... -

Page 9

... teams, sales centers and online resources. The result: 280,000 customers purchased personal insurance online (up 90 percent from 2008). On the commercial front, we serve some 40,000 businesses, including almost one of every ï¬ve Fortune 1,000 companies. With Wachovia's insurance brokerage team... -

Page 10

... lines, often coast to coast. They buy goods and services globally by mail and on the internet. Good for them and good for our economy. Our customers want to bank wherever they are and however they wish, by internet, telephone, in our banking stores or our ATMs. It's taken years to carefully balance... -

Page 11

... us in a position for future growth - because of our vision and values, time-tested business model, team member talent, liquidity, capital, ability to generate revenue from such a diversity of businesses and geographies, and because of the success to date of the Wells Fargo-Wachovia merger. John... -

Page 12

... their needs. Helping them compare investment options for a secure retirement. Making sure they understand lending requirements so they can qualify for a home mortgage. Saving them money on insurance. Helping companies grow by raising new capital. Here's how a vision should work ...for our customers... -

Page 13

... her customer her banking statement. She asked a simple question: "How much are you paying in auto insurance?" Nguyen asked if she had time right now to see if Wells Fargo could offer a better deal. Together, they called a Wells Fargo Insurance agent. An hour later, the customer saved $400 a year in... -

Page 14

...experts for personal loans, or mortgages or other services. We're a gateway into Wells Fargo." Jamie Berthiaume Team Member, Colorado Springs, Colorado n Illinois customer was on wellsfargo.com checking out a home equity loan last fall when a little box showed on his screen. It was an invitation to... -

Page 15

...with Jesus and Guadalupe Robles, then started a 72-hour marathon to help the family get their home mortgage. They were already Wells Fargo banking customers, so a personal banker veriï¬ed their accounts, while other team members helped them understand lending requirements and veriï¬ed their income... -

Page 16

... for our company, helping us succeed in many ways," said David Wolf, Berry's chief ï¬nancial o cer (below). "Now that we can turn to Wells Fargo to tap capital markets, we've deepened and strengthened our long-term relationship." D The vision that works Long-time customer, new-found service 14 -

Page 17

... is a long-time customer of Wells Fargo with a dozen products and services. He's also a big online-banking fan. When he saw the redesigned Wells Fargo Retirement Online Center, he dug in, researching information that he and his family need to plan a secure retirement. "I'm also using the site to... -

Page 18

...From day one, we put the customer ï¬rst and we delivered as one team." Corrie Bowman and Lynn Love Team Members, Los Angeles, California n mid-2008, the city of Los Angeles decided to do business with both Wachovia and Wells Fargo. Months later, the two companies announced their agreement to merge... -

Page 19

... Wells Fargo Home Mortgage store in their new hometown of Fayetteville, Arkansas. A year after getting a mortgage for their new home, however, expenses began to get tight: Cindy was in college working part-time and they needed to free up cash to cover some health expenses. They again turned to Wells... -

Page 20

... and team member Sherry Walker enrolled employees in Wells Fargo Membership® Banking (including free checking, savings accounts and credit cards). "It starts with asking for their business, then providing outstanding service, and now we're helping both a company and its employees be ï¬nancially... -

Page 21

...a new mortgage for their business by day's end or face $15,000 in prepayment penalties from another lender. One problem: They were vacationing in Florida, and the papers were 2,200 miles away with team member Sheila Chacon (below, left) in Phoenix. The solution: With no Wells Fargo location anywhere... -

Page 22

... North Carolina, had been saving for retirement. Now they needed a plan just for them. Renee's employer held a beneï¬ts fair where she spoke to Paul Irving (inset, below), a Wells Fargo ï¬nancial advisor at the Wachovia booth. We managed the company's 401(k) retirement plan. Irving said, "Brad and... -

Page 23

... to get accounts set up and ask questions," Loar said. Testing continues on the online Make an AppointmentSM service, now available to customers in parts of California and Arizona. It's another example of how Wells Fargo stores, ATMs, wellsfargo.com and Wells Fargo Phone Bank all work together to... -

Page 24

... its 8,000 employees continue to rely on Wells Fargo for its stock transfer business and so much more: trust and custody services, treasury management applications, hedging opportunities, the placement of equity and helping arrange lines of credit to meet the capital needs of the company, and other... -

Page 25

23 -

Page 26

... That means we're "in and of" every community in which we do business. We were local ï¬rst, then national. We weren't born as a national bank that decided to be local. We were born as a local bank in one community that grew to be national. Here's how a vision should work ...for our communities. 24 -

Page 27

...district budgets are tight, our company can help ï¬ll the gap to keep literacy a priority." "When school district budgets are tight, our company can help ï¬ll the gap to keep literacy a priority." Carlos Carmona Team Member, Alexandria, Virginia The vision that works Fostering a love of reading... -

Page 28

"By investing just a few hours a month, we can help young adults build on skills that will help them in school and as they pursue careers." Bernard Bermudez Team Member, Las Vegas, Nevada Y oung people need strong adult role models to build character and skills. Cultivating our relationship with ... -

Page 29

... panels supply about 20 percent of the stores' electricity." S "Our coast-to-coast bankingstore conversion gives Wells Fargo a huge opportunity to live our environmental commitment." Sheri Elbert Team Member, San Francisco, California The vision that works The energy to integrate differently 27 -

Page 30

"The time I spent with customers was emotional, but it was rewarding to see how we could make an immediate di erence for so many people and neighborhoods." Shawn Gatewood Team Member, Frederick, Maryland ells Fargo Home Mortgage customers faced with the challenge of keeping up with monthly payments... -

Page 31

... structured a multimillion-dollar ï¬nancing plan for the nonproï¬t to buy and preserve the building and protect residents from potential rent hikes. Team member Katy Patricelli (pictured) of Portland worked with Community Development investment manager Kevin Gardiner in Salt Lake City to help make... -

Page 32

... week The vision that works $550,000 every day Where we give $23,000 every hour Education Community Development Human Services Arts and Culture 30% 26% 24% 11% 4% 1% 4% Investing in our communities Civic Environmental Other $42 million donated by team members during annual Community Support and... -

Page 33

... York (Accounting) Robert K. Steel 2, 3 Former President, CEO Wachovia Corporation Charlotte, North Carolina (Financial services) Susan E. Engel 2, 3, 5 Chief Executive Officer Portero, Inc. Armonk, New York (Online luxury retailer) John G. Stumpf Chairman, President, CEO Wells Fargo & Company... -

Page 34

... Paulsen, Wells Capital Management Inc. Karla M. Rabusch, Wells Fargo Funds Management, LLC Diversiï¬ed Products Group Michael R. James Marc L. Bernstein, Small Business Segment and Business Direct Lending Jerry Bowen, Auto Dealer Commercial Services Kevin Moss, Home Equity Lending David J. Rader... -

Page 35

... Variable Interest Entities 9 Mortgage Banking Activities 10 Intangible Assets 11 Deposits 12 Short-Term Borrowings 13 Long-Term Debt 14 Guarantees and Legal Actions 15 Derivatives 16 Fair Values of Assets and Liabilities 17 Preferred Stock 18 Common Stock and Stock Plans 19 Employee Beneï¬ts and... -

Page 36

... at the end of this Report. Financial Review Overview Wells Fargo & Company is a $1.2 trillion diversified financial services company providing banking, insurance, trust and investments, mortgage banking, investment banking, retail banking, brokerage and consumer finance through banking stores, the... -

Page 37

... common share Balance sheet (at year end) Securities available for sale Loans Allowance for loan losses Goodwill Assets Core deposits (1) Long-term debt Wells Fargo stockholders' equity Noncontrolling interests Total equity $ merger expenses, $1.0 billion through goodwill under purchase accounting... -

Page 38

... Share Data Year ended December 31 , 2009 Profitability ratios Wells Fargo net income to average assets (ROA) 0.97% Net income to average assets 1.00 Wells Fargo net income applicable to common stock to average Wells Fargo common stockholders' equity (ROE) 9.88 Net income to average total equity... -

Page 39

..., primarily mortgage banking and trust and investment fees; • the integration of Wachovia, which increased our expenses to align staffing models with those of Wells Fargo in our service and product distribution channels, as well as to align or enhance our various systems, business line support and... -

Page 40

... Net interest income Noninterest income Service charges on deposit accounts Trust and investment fees Card fees Other fees Mortgage banking Insurance Net gains from trading activities Net gains (losses) on debt securities available for sale Net gains (losses) from equity investments Operating leases... -

Page 41

... estate 1-4 family junior lien mortgage Credit card Other revolving credit and installment Total consumer Foreign Total loans (2) Other Total earning assets Funding sources Deposits: Interest-bearing checking Market rate and other savings Savings certificates Other time deposits Deposits in foreign... -

Page 42

... estate 1-4 family junior lien mortgage Credit card Other revolving credit and installment Total consumer Foreign Total loans (6) Other Total earning assets Funding sources Deposits: Interest-bearing checking Market rate and other savings Savings certiï¬cates Other time deposits Deposits in foreign... -

Page 43

... loans and securities. The federal statutory tax rate was 35% for the periods presented. (8) See Note 7 (Premises, Equipment, Lease Commitments and Other Assets) to Financial Statements in this Report for detail of balances of other noninterest-earning assets at December 31, 2009 and 2008. 41 -

Page 44

... in average volume and average rate. Year ended December 31, 2009 over 2008 (in millions) Increase (decrease) in net interest income: Federal funds sold, securities purchased under resale agreements and other short-term investments Trading assets Debt securities available for sale: Securities... -

Page 45

...$379 billion acquired from Wachovia) at December 31, 2008. At December 31, 2009, the ratio of MSRs to related loans serviced for others was 0.91%. Net gains on mortgage loan origination/sales activities of $6.2 billion for 2009 were up from $1.2 billion a year ago, due to strong business performance... -

Page 46

... as retail brokerage, asset management and investment banking. As part of our integration investment to enhance both the short- and long-term benefits to our customers, we added sales and service team members to align Wachovia's banking stores and other distribution channels with Wells Fargo's model... -

Page 47

... and small businesses including investment, insurance and trust services in 39 states and D.C., and mortgage and home equity loans in all 50 states and D.C. Wachovia added expanded product capability as well as expanded channels to better serve our customers. Community Banking includes Wells Fargo... -

Page 48

... very strong and balanced growth in loans, deposits and fee-based products. We achieved positive operating leverage (revenue growth of 6%; expense decline of 1%), the best among large bank peers. Wells Fargo net income for 2008 of $2.7 billion included an $8.1 billion (pre tax) credit reserve build... -

Page 49

... in long-term yields and narrowing of credit spreads. With the application of purchase accounting at December 31, 2008, for the Wachovia portfolio, the net unrealized losses in cumulative other comprehensive income (OCI), a component of common equity, related entirely to the legacy Wells Fargo... -

Page 50

... - Net Interest Income" earlier in this Report; year-end balances and other loan related information are in Note 6 (Loans and Allowance for Credit Losses) to Financial Statements in this Report. During 2009, we further refined our preliminary purchase accounting adjustments related to loans from... -

Page 51

... due to: Loans resolved by payment in full (1) Loans resolved by sales to third parties (2) Loans with improving cash ï¬,ows reclassiï¬ed to accretable yield (3) Use of nonaccretable difference due to: Losses from loan resolutions and write-downs (4) Balance at December 31, 2009 Pick-a-Pay (26,485... -

Page 52

... at December 31, 2008. High-rate CDs of $109 billion at Wachovia matured in 2009 and were replaced by $62 billion in checking, savings or lower-cost CDs. We continued to gain new deposit customers and deepen our relationships with existing customers. December 31, % of total deposits 22% 8 49 12... -

Page 53

... were not obligated to support such funds. The FASB issued new guidance for accounting for offbalance sheet transactions with QSPEs and VIEs effective January 1, 2010, that replaces the current consolidation model for VIEs. For further information and the impact of the application of this guidance... -

Page 54

... (FAS 167). See the "Current Accounting Developments" section in this Report for our estimate of the nonconforming mortgages that may potentially be consolidated under this guidance. (2) Includes investment funds that are subject to deferral from application of ASU 2009-17 (FAS 167). Guarantees and... -

Page 55

...Short-Term Borrowings) and Note 19 (Employee Benefits and Other Expenses) to Financial Statements in this Report. (in millions) Contractual payments by period: Deposits Long-term debt (2) Operating leases Unrecognized tax obligations Purchase obligations (3) Total contractual obligations 1-3 years... -

Page 56

... models (AVMs) to support property values. AVMs are computer-based tools used to estimate the market value of homes. AVMs are a lower-cost alternative to appraisals and support valuations of large numbers of properties in a short period of time. AVMs estimate property values based on processing... -

Page 57

... 31, 2009. December 31, 2009 Real estate mortgage Nonaccrual Outstanding loans balance (1) Real estate construction Nonaccrual Outstanding loans balance (1) Total Nonaccrual Outstanding loans balance (1) % of total loans (in millions) By state: PCI loans: Florida California North Carolina Georgia... -

Page 58

..., we acquired residential first and home equity loans that are very similar to the Wells Fargo core originated portfolio. We also acquired the Pick-a-Pay portfolio, which is composed primarily of option payment adjustable-rate mortgage and fixed-rate mortgage products. Under purchase accounting for... -

Page 59

... and currently successful modification efforts as well as improving delinquency roll rate trends and further stabilization in the housing market. Pick-a-Pay option payment loans may be adjustable or fixed rate. They are home mortgages on which the customer has the option each month to select... -

Page 60

... of the date when the loan balance reaches its principal cap, or the 10-year anniversary of the loan. There exists a small population of Pick-a-Pay loans for which recast occurs at the Table 24: Pick-a-Pay Portfolio five-year anniversary. After a recast, the customers' new payment terms are reset... -

Page 61

... of 30 days or more were 5.5% of credit card outstandings at December 31, 2009, up from 5.0% a year ago. Net charge-offs were 10.8% for 2009, up from 7.2% in 2008, reflecting high bankruptcy filings and the current economic environment. We have tightened underwriting criteria and imposed credit line... -

Page 62

... loans as PCI loans at year-end 2008. This purchase accounting resulted in reclassifying all but $97 million of Wachovia's nonaccruing loans to accruing status, virtually eliminating all nonaccrual loans as of our merger date, and limiting comparability of this metric and related credit ratios... -

Page 63

... estate 1-4 family ï¬rst mortgage Real estate 1-4 family junior lien mortgage Other revolving credit and installment Total consumer Foreign Total nonaccrual loans Foreclosed assets: GNMA loans All other Total foreclosed assets Real estate and other nonaccrual investments Total nonaccrual loans and... -

Page 64

... troubled loans and work with the customer to modify to more affordable terms before their loan reaches nonaccrual status. Accordingly, during 2009 most consumer loans were in accrual status at the time of TDR and therefore most of our consumer TDR loans are in accrual status at the end of the year... -

Page 65

...56 1.54% (1) Annualized Net charge-offs in 2009 were $18.2 billion (2.21% of average total loans outstanding) compared with $7.8 billion (1.97%) in 2008. The year over year increase in net charge-offs is significantly impacted by the merger as the 2008 totals reflect only Wells Fargo loss results... -

Page 66

..., borrower credit strength and the value and marketability of collateral. Over half of nonaccrual loans were home mortgages, auto and other consumer loans at December 31, 2009. The ratio of the allowance for loan losses to annual net charge-offs was 135%, 268% and 150% at December 31, 2009, 2008 and... -

Page 67

... balance sheet date. Our process for determining the adequacy of the allowance for credit losses is discussed in the "Critical Accounting Policies - Allowance for Credit Losses" section and Note 6 (Loans and Allowance for Credit Losses) to Financial Statements in this Report. RESERVE FOR MORTGAGE... -

Page 68

...rates paid on checking and savings deposit accounts by an amount that is less than the general decline in market interest rates); • short-term and long-term market interest rates may change by different amounts (for example, the shape of the yield curve may affect new loan yields and funding costs... -

Page 69

... available market prices existed to reliably support fair value pricing models used for these loans. At December 31, 2008, we measured at fair value similar MHFS acquired from Wachovia. Loan origination fees on these loans are recorded when earned, and related direct loan origination costs and fees... -

Page 70

.... In 2009, a $1.5 billion decrease in the fair value of our MSRs and $6.8 billion of gains on free-standing derivatives used to hedge the MSRs resulted in a net gain of $5.3 billion. This net gain was largely due to hedge-carry income reflecting the current low short-term interest rate environment... -

Page 71

... at December 31, 2009 and 2008, respectively. Principal investments are carried at fair value with net unrealized gains and losses reported in noninterest income. As part of our business to support our customers, we trade public equities, listed/OTC equity derivatives and convertible bonds. We have... -

Page 72

...secured funding. Investors in the long-term capital markets generally will consider, among other factors, a company's debt rating in making investment decisions. Wells Fargo Bank, N.A. is rated "Aa2," by Moody's Investors Service, and "AA," by Standard & Poor's (S&P) Rating Services. Rating agencies... -

Page 73

... will also be used for general corporate purposes. The Parent also issues commercial paper from time to time, subject to its short-term debt limit. Wells Fargo Bank, N.A. Wells Fargo Bank, N.A. is authorized by its board of directors to issue $100 billion in outstanding short-term debt and $50... -

Page 74

...Statements in this Report for additional information. Current regulatory RBC rules are based primarily on broad credit-risk considerations and limited market related risks, but do not take into account other types of risk a financial company may be exposed to. Our capital adequacy assessment process... -

Page 75

... the capital position of financial services companies. Tier 1 common equity includes total Wells Fargo stockholders' equity, less preferred equity, goodwill and intangible assets (excluding MSRs), net of related deferred taxes, adjusted for specified Tier 1 regulatory capital limitations covering... -

Page 76

... and/or segmentation method that fits the credit risk characteristics of its portfolio. We use both internally developed and vendor supplied models in this process. We often use roll rate/net flow models for near-term loss projections, and vintage-based models, behavior score models, and time series... -

Page 77

... that calculates the present value of estimated future net servicing income. The model incorporates assumptions that market participants use in estimating future net servicing income, including estimates of prepayment speeds (including housing price volatility), discount rate, default rates, cost to... -

Page 78

... the model - is the annual rate at which borrowers are forecasted to repay their mortgage loan principal. The discount rate used to determine the present value of estimated future net servicing income - another key assumption in the model-is the required rate of return investors in the market would... -

Page 79

...to merge the Pension Plan into the qualified Cash Balance Plan. These actions became effective on July 1, 2009. We use four key variables to calculate our annual pension cost: size and characteristics of the employee population, actuarial assumptions, expected long-term rate of return on plan assets... -

Page 80

...-TERM RATE OF RETURN ON PLAN ASSETS DISCOUNT RATE We use a discount rate to determine the present value of our future benefit obligations. The discount rate reflects the current rates available on long-term high-quality fixed-income debt instruments, and is reset annually on the measurement date... -

Page 81

... accounted for as a sale be initially recognized at fair value. This pronouncement is effective for us as of January 1, 2010, with adoption applied prospectively for transfers that occur on and after the effective date. ASU 2009-17 (FAS 167) amends several key consolidation provisions related... -

Page 82

... Estimated Impact of Initial 2010 Application of ASU 2009-16 (FAS 166) and ASU 2009-17 (FAS 167) by Balance Sheet Classification (in billions) Net increase (decrease) Trading assets Securities available for sale Loans, net (1) Short-term borrowings Long-term debt Other Cumulative other comprehensive... -

Page 83

... value of, and return on, an investment in the Company. We refer you to the Financial Review section and Financial Statements (and related Notes) in this Report for more information about credit, interest rate, market and litigation risks and to the "Regulation and Supervision" section of our 2009... -

Page 84

...new or updated information that provided a better estimate of the fair value at merger date. We recorded at fair value all PCI loans acquired in the merger based on the present value of their expected cash flows. We estimated cash flows using internal credit, interest rate and prepayment risk models... -

Page 85

... sources of funding. Higher funding costs reduce our net interest margin and net interest income. As discussed above, the integration of Wells Fargo and Wachovia may result in the loss of customer deposits. We sell most of the mortgage loans we originate in order to reduce our credit risk and... -

Page 86

... incremental cost of the new coverage for certain loans depending on the terms of our servicing agreement with the investor and other circumstances. Similarly, some of the mortgage loans we hold for investment or for sale carry mortgage insurance. If a mortgage insurer is unable to meet its credit... -

Page 87

... brokerage services business. For more information, refer to the "Risk Management - Asset/ Liability Management - Market Risk - Equity Markets" section in this Report. We may elect to provide capital support to our mutual funds relating to investments in structured credit products. The money market... -

Page 88

... trading assets and liabilities, available-for-sale securities, certain loans, MSRs, private equity investments, structured notes and certain repurchase and resale agreements, among other items, require a determination of their fair value in order to prepare our financial statements. Where quoted... -

Page 89

..., including: • general business and economic conditions; • recommendations by securities analysts; • new technology used, or services offered, by our competitors; • operating and stock price performance of other companies that investors deem comparable to us; • news reports relating to... -

Page 90

... as of December 31, 2009, the Company's internal control over financial reporting was effective. KPMG LLP, the independent registered public accounting firm that audited the Company's financial statements included in this Annual Report, issued an audit report on the Company's internal control over... -

Page 91

..., changes in equity and comprehensive income, and cash flows for each of the years in the three-year period ended December 31, 2009, and our report dated February 26, 2010, expressed an unqualified opinion on those consolidated financial statements. San Francisco, California February 26, 2010 89 -

Page 92

... Short-term borrowings Long-term debt Other interest expense Total interest expense Net interest income Provision for credit losses Net interest income after provision for credit losses Noninterest income Service charges on deposit accounts Trust and investment fees Card fees Other fees Mortgage... -

Page 93

Wells Fargo & Company and Subsidiaries Consolidated Balance Sheet December 31, (in millions, except shares) Assets Cash and due from banks Federal funds sold, securities purchased under resale agreements and other short-term investments Trading assets Securities available for sale Mortgages held ... -

Page 94

Wells Fargo & Company and Subsidiaries Consolidated Statement of Changes in Equity and Comprehensive Income (in millions, except shares) Balance December 31, 2006 Cumulative effect from change in accounting for leveraged leases Balance January 1, 2007 Comprehensive income: Net income Other ... -

Page 95

Wells Fargo stockholders' equity Additional paid-in capital 7,739 7,739 Retained earnings 35,215 (71) 35,144 8,057 23 (164) 322 242 Cumulative other comprehensive income 302 302 Treasury stock (3,203) (3,203) Unearned ESOP shares (411) (411) Total Wells Fargo stockholders' equity 45,814 (71) 45,743 ... -

Page 96

... and accretion Tax beneï¬t upon exercise of stock options Stock option compensation expense Net change in deferred compensation and related plans Net change Balance December 31, 2009 The accompanying notes are an integral part of these statements. Preferred stock Shares Amount 10,111,821 $ 31,332... -

Page 97

Wells Fargo stockholders' equity Additional paid-in capital 36,026 Retained earnings 36...026) 18 221 (99) 12,043 114,359 Treasury stock (4,666) Unearned ESOP shares (555) Total Wells Fargo stockholders' equity 99,084 Noncontrolling interests 3,232 Total equity 102,316 5 390 (4,500) (265) 1,440 (79... -

Page 98

... entities Net cash acquired from (paid for) acquisitions Proceeds from sales of foreclosed assets Changes in MSRs from purchases and sales Other, net Net cash provided (used) by investing activities Cash ï¬,ows from ï¬nancing activities: Net change in: Deposits Short-term borrowings Long-term debt... -

Page 99

... (consolidated). Wells Fargo & Company (the Parent) is a financial holding company and a bank holding company. We also hold a majority interest in a retail brokerage subsidiary and a real estate investment trust, which has publicly traded preferred stock outstanding. Our accounting and reporting... -

Page 100

... of Generally Accepted Accounting Principles - a replacement of FASB Statement No. 162). In fourth quarter 2009, we adopted the following new accounting guidance: • Accounting Standards Update (ASU or Update) 2009-12, Investments in Certain Entities That Calculate Net Asset Value per Share (or... -

Page 101

..., at their fair values as of that date, with limited exceptions. The acquirer is not permitted to recognize a separate valuation allowance as of the acquisition date for loans and other assets acquired in a business combination. The revised statement requires acquisition-related costs to be expensed... -

Page 102

... consolidated financial statements. See Note 16 in this Report for disclosures related to certain alternative investments. ASU 2009-5 describes the valuation techniques companies should use to measure the fair value of liabilities for which there is limited observable market data. If a quoted price... -

Page 103

...measured using independent pricing models or other model-based valuation techniques such as the present value of future cash flows, adjusted for the security's credit rating, prepayment assumptions and other factors such as credit loss assumptions and market liquidity. See Note 16 in this Report for... -

Page 104

... in mortgage banking noninterest income upon sale of the loan. Our lines of business are authorized to originate heldfor-investment loans that meet or exceed established loan product profitability criteria, including minimum positive net interest margin spreads in excess of funding costs. When... -

Page 105

... LOANS (CLOSED END) UNSECURED LOANS (OPEN END) We generally place loans on nonaccrual status when: • the full and timely collection of interest or principal becomes uncertain; • they are 90 days (120 days with respect to real estate 1-4 family first and junior lien mortgages and auto loans... -

Page 106

... inherent in the loan portfolio at the balance sheet date. Evidence of credit quality deterioration as of the purchase date may include statistics such as past due and nonaccrual status, recent borrower credit scores and recent loan-to-value percentages. Generally, acquired loans that meet our... -

Page 107

...model that market participants use in estimating future net servicing income, including estimates of prepayment speeds (including housing price volatility), discount rate, default rates, cost to service (including delinquency and foreclosure costs), escrow account earnings, contractual servicing fee... -

Page 108

... in the accounting provisions for retirement benefits did not change the amount of net periodic benefit expense recognized in our income statement. One of the principal components of the net periodic pension expense calculation is the expected long-term rate of return on plan assets. The use of an... -

Page 109

... net income in the same financial statement category as the hedged item. For free-standing derivatives, we report changes in the fair values in current period noninterest income. For fair value and cash flow hedges qualifying for hedge accounting, we formally document at inception the relationship... -

Page 110

Note 1: Summary of Significant Accounting Policies (continued) SUPPLEMENTAL CASH FLOW INFORMATION Noncash investing and financing activities are presented below, including information on transfers affecting MHFS, LHFS, and MSRs. Year ended December 31, (in millions) Transfers from trading assets ... -

Page 111

...and services to customers through 3,300 financial centers in 21 states from Connecticut to Florida and west to Texas and California, and nationwide retail brokerage, mortgage lending and auto finance businesses. In the merger, we exchanged 0.1991 shares of our common stock for each outstanding share... -

Page 112

... related 129 354 (139) 344 Total 199 1,011 (453) 757 (1) Certain purchase accounting adjustments have been refined during 2009 as additional information became available. We regularly explore opportunities to acquire financial services companies and businesses. Generally, we do not make a public... -

Page 113

... our subsidiary banks maintain reserve balances on deposit with the Federal Reserve Banks. The average required reserve balance was $2.4 billion in 2009 and $2.6 billion in 2008. Federal law restricts the amount and the terms of both credit and non-credit transactions between a bank and its nonbank... -

Page 114

...auto leases or loans and cash reserves with a cost basis and fair value of $8.2 billion and $8.5 billion, respectively, at December 31, 2009, and $8.3 billion and $7.9 billion, respectively, at December 31, 2008. Also included in the "Other" category are assetbacked securities collateralized by home... -

Page 115

... rates and not due to the credit quality of the securities. The fair value of these investments is almost exclusively investment grade. The securities were generally underwritten in accordance with our own investment standards prior to the decision to purchase, without relying on a bond insurer... -

Page 116

... securities, which are primarily backed by auto, home equity and student loans. The losses are primarily driven by higher projected collateral losses, wider credit spreads and changes in interest rates. We assess for credit impairment using a cash ï¬,ow model. The key assumptions include default... -

Page 117

... value of debt and perpetual preferred securities available for sale by those rated investment grade and those rated less than investment grade, according to their lowest credit rating by Standard & Poor's Rating Services (S&P) or Moody's Investors Service (Moody's). Credit ratings express opinions... -

Page 118

...-for-sale portfolio, including marketable equity securities. Realized losses included OTTI write-downs of $1.1 billion, $1.8 billion and $50 million for 2009, 2008 and 2007, respectively. Year ended December 31, (in millions) Gross realized gains Gross realized losses Net realized gains 2009 $ 1,601... -

Page 119

... example, 56% of credit impairment losses recognized in earnings for the year ended December 31, 2009, had expected remaining life of loan loss assumptions of 0 to 10%. (5) Calculated by weighting the relevant input/assumption for each individual security by current outstanding amortized cost basis... -

Page 120

...-average yield is computed using the contractual coupon of each security weighted based on the fair value of each security. (2) Information for December 31, 2008, has been revised to conform the determination of remaining contractual principal maturities and weighted-average yields to the current... -

Page 121

... PCI loans. Certain loans acquired in the Wachovia acquisition are accounted for as PCI loans and are included below, net of any remaining purchase accounting adjustments. Outstanding balances of all other loans are presented net of unearned income, net deferred loan fees, and unamortized discount... -

Page 122

... consumer loans and some commercial small business loans, we use loss models and other quantitative, mathematical techniques. Each business group estimates losses for loans as of the balance sheet date over the loss emergence period. During fourth quarter 2008, we conformed our loss emergence period... -

Page 123

...losses includes $333 million for the year ended December 31, 2009, and none for prior years related to PCI loans acquired from Wachovia. Loans acquired from Wachovia are included in total loans, net of related purchase accounting net write-downs. Nonaccrual loans were $24.4 billion and $6.8 billion... -

Page 124

... loans whose terms have been modiï¬ed in a TDR. The recorded investment in impaired loans and the methodology used to measure impairment was: December 31, (in millions) Impairment measurement based on: Collateral value method Discounted cash ï¬,ow method (1) Total (2) 2009 $ 561 15,217 $15,778 2008... -

Page 125

...-owned life insurance Accounts receivable Interest receivable Core deposit intangibles Customer relationship and other intangibles Net deferred taxes Foreclosed assets: GNMA loans (3) Other Operating lease assets Due from customers on acceptances Other Total other assets 2009 2008 $ 3,808 5,985... -

Page 126

...in which it may engage. For example, a QSPE's activities are generally limited to purchasing assets, passing along the cash ï¬,ows of those assets to its investors, servicing its assets and, in certain transactions, issuing liabilities. Among other restrictions on a QSPE's activities, a QSPE may not... -

Page 127

... held for sale Loans (3) Mortgage servicing rights (4) Other assets Total assets Short-term borrowings Accrued expenses and other liabilities (4) Long-term debt Noncontrolling interests Total liabilities and noncontrolling interests Net assets December 31, 2009 Cash Trading account assets Securities... -

Page 128

...most current information available. (2) Excludes certain debt securities held related to loans serviced for FNMA, FHLMC and GNMA. (3) Certain balances have been revised to reflect additionally identified residential mortgage QSPEs, as well as to reflect removal of commercial mortgage asset transfers... -

Page 129

... Purchases of delinquent assets Net servicing advances (1) Represents cash ï¬,ow data for all loans securitized in the period presented. For securitizations completed in 2009 and 2008, we used the following weighted-average assumptions to determine the fair value of residential mortgage servicing... -

Page 130

... 14,317 Net charge-offs (3) Year ended December 31, 2009 3,111 833 959 209 5,112 4,420 4,692 2,528 2,775 14,415 197 19,724 2008 1,539 26 175 52 1,792 902 2,115 1,416 1,819 6,252 196 8,240 (1) Represents loans in the balance sheet or that have been securitized and includes residential mortgages sold... -

Page 131

... funds Credit-linked note structures Money market funds (4) Other (5) Total December 31, 2009 Collateralized debt obligations Wachovia administered ABCP (3) conduit Asset-based ï¬nance structures Tax credit structures Collateralized loan obligations Investment funds Credit-linked note structures... -

Page 132

... of highly rated commercial paper to third party investors. The primary source of repayment of the commercial paper is the cash ï¬,ows from the conduit's assets or the re-issuance of commercial paper upon maturity. The conduit's assets are structured with deal-speciï¬c credit enhancements generally... -

Page 133

... 31, 2009 Funded asset composition Commercial and middle market loans Auto loans Equipment loans Leases Trade receivables Credit cards Other Total 42.3% 26.8 18.5 4.2 3.3 1.7 3.2 100.0% Total committed exposure 35.6 29.2 16.8 3.2 10.3 2.7 2.2 100.0 December 31, 2008 (1) Funded asset composition... -

Page 134

... in these funds. INVESTMENT FUNDS MONEY MARKET FUNDS In 2008 we entered into a capital support agreement for up to $130 million related to an investment in a structured investment vehicle (SIV) held by AAArated money market funds we sponsor in order to maintain a AAA credit rating and a NAV... -

Page 135

... loans Residential mortgage securitizations Total secured borrowings Consolidated VIEs: Structured asset ï¬nance Investment funds Other Total consolidated VIEs Total secured borrowings and consolidated VIEs December 31, 2009 Secured borrowings: Municipal tender option bond securitizations Auto loan... -

Page 136

... commercial mortgage originations and servicing. The changes in residential MSRs measured using the fair value method were: Year ended December 31, (in millions) Fair value, beginning of year Purchases Acquired from Wachovia (1) Servicing from securitizations or asset transfers Sales Net additions... -

Page 137

...Total servicing income, net Net gains on mortgage loan origination/sales activities All other Total mortgage banking noninterest income Market-related valuation changes to MSRs, net of hedge results (1) + (3) 2009 $ 3,942 (1,534) (3,436) (4,970) (264) 6,849 5,557 6,152 319 $12,028 $ 5,315 2008 3,855... -

Page 138

... our initial acquisition date purchase accounting. Wealth, Brokerage and Consolidated Retirement Company 368 - - - 368 5 - 373 13,106 (1) 9,532 (10) 22,627 2,178 7 24,812 (in millions) December 31, 2007 Reduction in goodwill related to divested businesses Goodwill from business combinations Foreign... -

Page 139

...were included as loan balances at December 31, 2009 and 2008, respectively. Note 12: Short-Term Borrowings The table below shows selected information for short-term borrowings, which generally mature in less than 30 days. At December 31, 2009, we had $500 million available in lines of credit. These... -

Page 140

... - Parent (15) Total long-term debt - Parent Wells Fargo Bank, N.A. and its subsidiaries (WFB, N.A.) Senior Fixed-rate notes Floating-rate notes Fixed-rate advances - Federal Home Loan Bank (FHLB) (1) Market-linked notes (5) Obligations of subsidiaries under capital leases (Note 7) Total senior debt... -

Page 141

... was ï¬led as Exhibit 99.1 to the Company's Current Report on Form 8-K ï¬led May 25, 2007. (8) On March 12, 2008, Wells Fargo Capital XII issued 7.875% Enhanced Trust Preferred Securities (Enhanced TRUPS®) (the First 2008 Capital Securities) and used the proceeds to purchase from the Parent 7.875... -

Page 142

....1 to the Company's Current Report on Form 8-K ï¬led September 10, 2008. (11) On February 15, 2007, Wachovia Capital Trust IV issued 6.375% Trust Preferred Securities (the First Wachovia Trust Securities) and used the proceeds to purchase from Wachovia 6.375% Extendible Long-Term Subordinated Notes... -

Page 143

... our long-term and short-term borrowing arrangements, we are subject to various ï¬nancial and operational covenants. Some of the agreements under which debt has been issued have provisions that may limit the merger or sale of certain subsidiary banks and the issuance of capital stock or convertible... -

Page 144

... liquidity to certain off-balance sheet entities that hold securitized ï¬xedrate municipal bonds and consumer or commercial assets that are partially funded with the issuance of money market and other short-term notes. See Note 8 in this Report for additional information on these arrangements... -

Page 145

... of New York on behalf of employees of Wachovia and its afï¬liates who held shares of Wachovia common stock in their Wachovia Savings Plan accounts. On June 18, 2009, the U.S. District Court for the Southern District of New York entered a Memorandum and Order transferring these consolidated cases... -

Page 146

... cost mortgages. Illinois also alleges that Wells Fargo Financial Illinois, Inc. misled Illinois customers about the terms of mortgage loans. Illinois' complaint against all Wells Fargo defendants is based on LE-NATURE'S INC. Wachovia Bank, N.A. is the administrative agent on a $285 million credit... -

Page 147

... of Wells Fargo & Company as a defendant. All of the cases are being coordinated in the Southern District of New York. PAYMENT PROCESSING CENTER On February 17, 2006, the U.S. Attorney's Ofï¬ce for the Eastern District of Pennsylvania ï¬led a civil fraud complaint against a former Wachovia Bank... -

Page 148

... 2008. Wachovia Bank, N.A. is cooperating with government ofï¬cials to administer the OCC settlement and in their continued investigation of this matter. OUTLOOK Based on information currently available, advice of counsel, available insurance coverage and established reserves, Wells Fargo believes... -

Page 149

... value of residential MSRs, MHFS, interest rate lock commitments and other interests held. (4) Customer accommodation, trading and other free-standing derivatives are included in trading assets or other liabilities. (5) Represents netting of derivative asset and liability balances, and related cash... -

Page 150

... for sale, short-term borrowings and long-term debt, representing the portion of derivative gain or loss excluded from assessment of hedge effectiveness (time value). Cash Flow Hedges We hedge ï¬,oating-rate debt against future interest rate increases by using interest rate swaps, caps, ï¬,oors... -

Page 151

... on customer accommodation, trading and other free-standing derivatives Interest rate contracts (2) Recognized in noninterest income: Mortgage banking Other Commodity contracts Equity contracts Foreign exchange contracts Credit contracts Other Subtotal Net gains recognized related to derivatives... -

Page 152

... amount Protection Protection sold - purchased nonwith investment identical grade underlyings (B) Net protection sold (A)-(B) (in millions) December 31, 2008 Credit default swaps on: Corporate bonds Structured products Credit protection on: Credit default swap index Commercial mortgagebacked... -

Page 153

...Report. Under fair value option accounting guidance, we elected to measure MHFS at fair value prospectively for new prime residential MHFS originations, for which an active secondary market and readily available market prices existed to reliably support fair value pricing models used for these loans... -

Page 154

.... These letters of credit are included in trading account assets or liabilities. Assets SHORT-TERM FINANCIAL ASSETS Short-term ï¬nancial assets include cash and due from banks, federal funds sold and securities purchased under resale agreements and due from customers on acceptances. These... -

Page 155

... as Level 2. for credit loss estimates, using discount rates that reï¬,ect our current pricing for loans with similar characteristics and remaining maturity. For real estate 1-4 family ï¬rst and junior lien mortgages, fair value is calculated by discounting contractual cash ï¬,ows, adjusted for... -

Page 156

... calculated based on the discounted value of contractual cash ï¬,ows. The discount rate is estimated using the rates currently offered for like wholesale deposits with similar remaining maturities. Short-term ï¬nancial liabilities are carried at historical cost and include federal funds purchased... -

Page 157

... cost. However, we are required to estimate the fair value of long-term debt in accordance with accounting guidance on ï¬nancial instruments. Generally, the discounted cash ï¬,ow method is used to estimate the fair value of our long-term debt. Contractual cash ï¬,ows are discounted using rates... -

Page 158

... Total marketable equity securities Total securities available for sale Mortgages held for sale Mortgage servicing rights (residential) Net derivative assets and liabilities Other assets (excluding derivatives) Other liabilities (excluding derivatives) Year ended December 31, 2008 Trading assets... -

Page 159

... related to sales, in 2008 and 2007, respectively. (6) Included in mortgage banking, trading activities and other noninterest income in the income statement. For certain assets and liabilities, we obtain fair value measurements from independent brokers or independent third party pricing services... -

Page 160

... adjustment has been included in the income statement, relating to assets held at period end. Year ended December 31, (in millions) Mortgages held for sale Loans held for sale Loans (1) Private equity investments Foreclosed assets (2) Operating lease assets Total $ 2009 (22) 158 (13,083) (112) (91... -

Page 161

... statement line item, below. Year ended December 31, 2009 Mortgages held for sale $4,891 - Loans held for sale - 99 Other interests held - 117 Mortgages held for sale 2,111 - 2008 Other interests held - (109) (in millions) Mortgage banking noninterest income: Net gains on mortgage loan origination... -

Page 162

..., the carrying value and fair value at December 31, 2008 were the same. Year ended December 31, 2009 (in millions) Financial assets Mortgages held for sale (1) Loans held for sale (2) Loans, net (3) Nonmarketable equity investments (cost method) Financial liabilities Deposits Long-term debt... -

Page 163

... were converted into shares of a corresponding series of Wells Fargo preferred stock having substantially the same rights and preferences. The carrying value is par value adjusted to fair value in purchase accounting. In addition to the preferred stock issued and outstanding described in the table... -

Page 164

... date of issuance. Prior to the December 23, 2009 redemption, the discount on the preferred stock was being accreted to par value using a constant effective yield of 7.2% over a ï¬ve-year term, which was the expected life of the preferred stock. All shares of our ESOP (Employee Stock Ownership Plan... -

Page 165

... purchase shares of our common stock at fair market value by reinvesting dividends and/or making optional cash payments, under the plan's terms. Employee Stock Plans We offer the stock based employee compensation plans described below. We measure the cost of employee services received in exchange... -

Page 166

... investment in Wells Fargo in December 2009. For various acquisitions and mergers, we converted employee and director stock options of acquired or merged companies into stock options to purchase our common stock based on the terms of the original stock option plan and the agreed-upon exchange ratio... -

Page 167

.... Various factors determine the amount and timing of our share repurchases, including our capital requirements, the number of shares we expect to issue for acquisitions and employee beneï¬t plans, market conditions (including the trading price of our stock), and regulatory and legal considerations... -

Page 168

...Fargo & Company 401(k) Plan (the 401(k) Plan) and the Wachovia Savings Plan (the Savings Plan), deï¬ned contribution plans with an ESOP feature, these plans may borrow money to purchase our preferred or common stock. From 1994 through 2008, we have loaned money to the 401(k) Plan to purchase shares... -

Page 169

... after June 30, 2009. Investment credits continue to be allocated to participants based on their accumulated balances. Employees become vested in their Cash Balance Plan accounts after completing three years of vesting service. Freezing and merging the above plans effective July 1, 2009, resulted in... -

Page 170

...of year Actual return on plan assets Employer contribution Plan participants' contributions Beneï¬ts paid Foreign exchange impact Acquisitions Measurement date adjustment (1) Fair value of plan assets at end of year Funded status at end of year Amounts recognized in the balance sheet at end of year... -

Page 171

..., 2009 and 2008, respectively. We seek to achieve the expected long-term rate of return with a prudent level of risk given the beneï¬t obligations of the pension plans and their funded status. Our overall investment strategy is designed to provide our Cash Balance Plan with a balance of long-term... -

Page 172

... long-term rate of return on plan assets is highly quantitative by nature. We evaluate the current asset allocations and expected returns under two sets of conditions: projected returns using several forward-looking capital market assumptions, and historical returns for the main asset classes dating... -

Page 173

...-cap stocks (2) Domestic mid-cap stocks Domestic small-cap stocks (3) International stocks (4) Emerging market stocks Real estate/timber (5) Multi-strategy hedge funds (6) Private equity Other Total pension plan investments Payable upon return of securities loaned Net receivables Total pension plan... -

Page 174

... income Domestic large-cap stocks (2) Domestic mid-cap stocks Domestic small-cap stocks International stocks (3) Emerging market stocks Real estate/timber Multi-strategy hedge funds Private equity Other Total other beneï¬ts plan investments Payable upon return of securities loaned Total other bene... -

Page 175

...investments traded on the OTC market and listed securities for which no sale was reported on that date; both are valued at the average of the last reported bid and ask prices. Also includes investments in collective investment funds described above. Domestic, International and Emerging Market Stocks... -

Page 176

... difference in investments PCI loans Mark to market, net Net unrealized losses on securities available for sale Net operating loss and tax credit carry forwards Other Total deferred tax assets Deferred tax assets valuation allowance Deferred tax liabilities Mortgage servicing rights Leasing Basis... -

Page 177

...: For tax positions related to the current year For tax positions related to prior years For tax positions from business combinations (1) Reductions: For tax positions related to prior years Lapse of statute of limitations Settlements with tax authorities Balance at end of year 2009 $ 7,521 438... -

Page 178

... to purchase 13.8 million shares were antidilutive. Year ended December 31, (in millions, except per share amounts) Wells Fargo net income Less: Preferred stock dividends and accretion (1) Wells Fargo net income applicable to common stock (numerator) Earnings per common share Average common shares... -

Page 179

..., 2006 Net change Balance, December 31, 2007 Net change Balance, December 31, 2008 Net change Balance, December 31, 2009 Translation adjustments $ 29 23 52 (58) (6) 73 $ 67 Securities available for sale 562 (164) 398 (6,610) (6,212) 9,753 3,541 (1) Adoption of accounting change related to pension... -

Page 180

... capital ï¬nancing, cash management, payroll services, retirement plans, Health Savings Accounts and merchant payment processing. Consumer and business deposit products include checking accounts, savings deposits, market rate accounts, Individual Retirement Accounts, time deposits and debit cards... -

Page 181

... and Wells Fargo net income for the Consolidated Company. (3) Includes integration expenses and the elimination of items that are included in both Community Banking and Wealth, Brokerage and Retirement, largely representing wealth management customers serviced and products sold in the stores. 179 -

Page 182

...in millions) Year ended December 31, 2009 Dividends from subsidiaries: Bank Nonbank Interest income from loans Interest income from subsidiaries Other interest income Total interest income Deposits Short-term borrowings Long-term debt Other interest expense Total interest expense Net interest income... -

Page 183

... Parent, WFFI, Other and Wells Fargo net income (loss) Year ended December 31, 2007 Dividends from subsidiaries: Bank Nonbank Interest income from loans Interest income from subsidiaries Other interest income Total interest income Deposits Short-term borrowings Long-term debt Total interest expense... -

Page 184

... for sale Mortgages and loans held for sale Loans Loans to subsidiaries: Bank Nonbank Allowance for loan losses Net loans Investments in subsidiaries: Bank Nonbank Other assets Total assets Liabilities and equity Deposits Short-term borrowings Accrued expenses and other liabilities Long-term debt... -

Page 185

... on notes/ loans made to subsidiaries Net decrease (increase) in investment in subsidiaries Net cash acquired from (paid for) acquisitions Other, net Net cash provided (used) by investing activities Cash ï¬,ows from ï¬nancing activities: Net change in: Deposits Short-term borrowings Long-term debt... -

Page 186

... net Net cash used by investing activities Cash ï¬,ows from ï¬nancing activities: Net change in: Deposits Short-term borrowings Long-term debt: Proceeds from issuance Repayment Common stock: Proceeds from issuance Repurchased Cash dividends paid Excess tax beneï¬ts related to stock option payments... -

Page 187

... 31, 2009. The junior subordinated debentures held by the Trusts were included in the Company's long-term debt. See Note 13 in this Report for additional information on trust preferred securities. Under the guidelines, capital is compared with the relative risk related to the balance sheet. To... -

Page 188

Report of Independent Registered Public Accounting Firm The Board of Directors and Stockholders Wells Fargo & Company: We have audited the accompanying consolidated balance sheet of Wells Fargo & Company and Subsidiaries (the Company) as of December 31, 2009 and 2008, and the related consolidated ... -

Page 189

...Noninterest income Service charges on deposit accounts Trust and investment fees Card fees Other fees Mortgage banking Insurance Net gains (losses) from trading activities Net gains (losses) on debt securities available for sale Net gains (losses) from equity investments Operating leases Other Total... -

Page 190

... estate 1-4 family junior lien mortgage Credit card Other revolving credit and installment Total consumer Foreign Total loans (5) Other Total earning assets Funding sources Deposits: Interest-bearing checking Market rate and other savings Savings certiï¬cates Other time deposits Deposits in foreign... -

Page 191

... loans with evidence of credit deterioration accounted for under FASB ASC 310-30 (AICPA Statement of Position 03-3) Pre-tax pre-provision proï¬t Qualifying special purpose entity Risk-based capital Wells Fargo net income to average total assets Wells Fargo net income applicable to common stock... -

Page 192

...Whether Instruments Granted in Share-Based Payment Transactions are Participating Securities FAS 114, Accounting by Creditors for Impairment of A Loan, an Amendment of FASB Statements No. 5 and 15, and AICPA SOP 03-3, Accounting for Certain Loans or Debt Securities Acquired in a Transfer FSP FAS 115... -

Page 193

... Wells Fargo's common stock, the KBW Bank Index and the S&P 500 Index. Five Year Performance Graph $140 $120 S&P 500 $100 $ 80 $ 60 $ 40 2004 $100 100 100 2005 $104 105 103 2006 $122 121 121 2007 $107 128 94 2008 $110 81 49 2009 $104 102 49 5-year CAGR 1% 0% -13% Wells Fargo S&P 500 KBW Bank Index... -

Page 194

Wells Fargo & Company Common stock Wells Fargo & Company is listed and trades on the New York Stock Exchange: WFC 5,178,624,593 common shares outstanding (12/31/09) Independent registered public accounting ï¬rm KPMG LLP San Francisco, California 1-415-963-5100 Barron's Among World's 50 Most ... -

Page 195

... Wells Fargo Phone Bank 3 500+ million customer contacts a year Our market leadership #1 Community banking stores #1 Retail banking deposits 1 #1 Deposit market share in 17 of our 39 Community Banking states and Washington D.C. 1 #1 Home mortgage originator and #2 mortgage servicer #1 Mortgage... -

Page 196

Wells Fargo & Company 420 Montgomery Street San Francisco, California 94104 1-866-878- 86 wellsfargo.com Our Vision: Satisfy all our customers' ï¬nancial needs and help them succeed ï¬nancially. Nuestra Vision: Deseamos satisfacer todas las necesidades ï¬nancieras de nuestros clientes y ...