SunTrust 2009 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

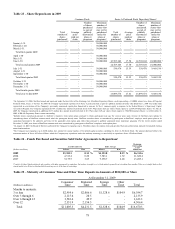

Provision for credit losses was $1.7 billion, an increase of $790.3 million, or 88.5%, principally due to higher consumer

mortgage and home equity line charge-offs.

Total noninterest income was $727.7 million, a $246.4 million, or 51.2%, increase driven by higher mortgage production and

servicing income. Total mortgage production income increased $190.2 million, or 105.4%, principally due to income from

higher loan production volume at improved margins partially offset by higher reserves for repurchased loans. Total mortgage

loan production for the year ended December 31, 2009 was $50.1 billion, up 37.6% from $36.4 billion the prior year. Total

servicing income increased $519.6 million primarily due to a $199.2 million recovery in 2009 on MSRs carried at the

LOCOM compared to a $370.0 million impairment charge in 2008. The 2008 MSR impairment was offset by net securities

gains of $410.7 million in the fourth quarter of 2008 from the sale of available for sale securities that were held in

conjunction with our risk management strategies associated with economically hedging the value of MSRs. At December 31,

2009 total mortgage loans serviced were $178.9 billion, up $16.9 billion, or 10.4%, from $162.0 billion at December 31,

2008.

Total noninterest expense was $1.8 billion, an increase of $254.1 million, or 16.6%. The increase was primarily due to a

$451.9 million non-cash goodwill impairment charge recorded in first quarter of 2009. Credit-related expense including other

real estate, credit service, and collection costs also increased $125.4 million, or 61.0%. The increases were partially offset by

a $373.7 million decrease in operating losses primarily due to a change in classification related to borrower misrepresentation

and claim denials. Beginning in 2009, these losses were recorded as charge-offs against the allowance for loan losses and

were included in the overall allowance for loan losses. Additionally, personnel expense was up $115.8 million principally

due to higher commission expense resulting from higher loan production.

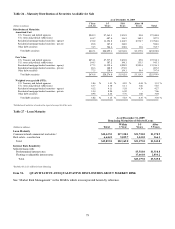

Wealth and Investment Management

Wealth and Investment Management’s net income for the twelve months ended December 31, 2009 was $67.9 million, a

decrease of $106.5 million compared to the same period in 2008. The decrease in net income was primarily due to the gains

from the sales of First Mercantile and Lighthouse Investment Partners in 2008 and the resulting reduction in noninterest

income partially offset by lower noninterest expense in 2009. Net income in 2008 included a $63.8 million market valuation

loss on an acquired security primarily in the third quarter and a $45.0 million impairment charge on a client-based intangible

asset in the second quarter.

Net interest income was $304.0 million, a decrease of $21.1 million, or 6.5%, as higher average loan and deposit balances

were more than offset by spread compression. Average loans increased slightly while net interest income on loans declined

$6.3 million, or 4.6%, due to compressed spreads. Average deposits increased $1.5 billion, or 16.0%, while deposit-related

net interest income decreased $13.3 million, or 6.6%, due to a change in mix, a decrease in the relative value of demand

deposits, and spread compression in NOW and money market accounts.

Provision for credit losses were $79.2 million, an increase of $52.3 million primarily due to higher consumer and commercial

loan net charge-offs.

Total noninterest income was $748.6 million, a $200.6 million, or 21.1%, decrease primarily due to an $89.4 million gain on

sale of a minority interest in Lighthouse Investment Partners in the first quarter of 2008, $50.1 million net decline due to the

sale of First Mercantile in the second quarter of 2008, and lower trust income and retail investment income. Trust income

decreased $102.9 million, or 17.5%, primarily due to lower market valuations on managed equity assets, investment advisory

fee waivers on managed liquidity funds, migration of money market fund assets into deposits, and the sale of First

Mercantile. Retail investment income declined $71.3 million, or 25.5%, due to lower annuity sales and market driven

declines in assets in managed accounts. Partially offsetting those declines, trading gains and losses increased $78.4 million

primarily due to a $63.8 million market valuation loss on a security purchased from our RidgeWorth subsidiary recorded in

the third quarter of 2008.

As of December 31, 2009, assets under management were approximately $119.5 billion compared to $113.1 billion as of

December 31, 2008. Assets under management include individually managed assets, the RidgeWorth Funds, managed

institutional assets, and participant-directed retirement accounts. SunTrust’s total assets under advisement were

approximately $205.4 billion, which includes $119.5 billion in assets under management, $46.0 billion in non-managed trust

assets, $31.8 billion in retail brokerage assets, and $8.1 billion in non-managed corporate trust assets.

Total noninterest expense was $863.1 million, down $106.8 million, or 11.0%, primarily due to the sale of First Mercantile in

2008 and a $45.0 million impairment charge on a client based intangible incurred in the second quarter of 2008. Employee

compensation declined $63.2 million, or 13.4%, resulting from reduced headcount and lower incentive payments.

Discretionary expenses including other staff, advertising, and customer development declined $12.3 million, or 36.4%. Other

expense also declined $21.6 million primarily due to the sale of First Mercantile and reduced clearing costs related to retail

investment income. These decreases were partially offset by higher operating losses, other real estate expense, indirect

support cost, and FDIC expense.

71