SunTrust 2009 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

Parent Company Liquidity. We measure Parent Company liquidity by comparing sources of liquidity from short-term assets,

such as unencumbered and other investment securities and cash, relative to short-term liabilities, which include overnight

sweep funds, seasoned long-term debt, and CP. As of December 31, 2009, the Parent Company had $2.6 billion in such

sources compared to short-term debt of $1.6 billion. As of December 31, 2009, the Parent Company also had approximately

$5 billion in U.S. Treasury securities that were purchased in the fourth quarter of 2009 in anticipation of repayment of TARP.

We also manage the Parent Company’s liquidity by structuring its maturity schedule to minimize the amount of debt

maturing within a short period of time. Approximately $300 million of Parent Company debt matured in October 2009 and

$300 million is scheduled to mature during 2010. Much of the Parent Company’s liabilities are long-term in nature, coming

from the proceeds of our capital securities and long-term senior and subordinated notes.

The primary uses of Parent Company liquidity include debt service, dividends on capital instruments, the periodic purchase

of investment securities, and loans to our subsidiaries. We believe the Parent Company holds ample cash to satisfy these

working capital needs. We fund corporate dividends primarily with dividends from our banking subsidiary. We are subject to

both state and federal banking regulations that limit our ability to pay common stock dividends in certain circumstances. In

the context of the recent economic recession and credit market turmoil, we reduced our quarterly common stock dividend.

Effective for the quarterly dividend paid in September 2009, the common stock dividend was $0.01 per share. It is not likely

that we will increase our quarterly dividend until we have returned to profitability and obtained the consent from our

applicable regulators.

Recent Market and Regulatory Developments. Financial market conditions remained under a state of stress during much of

2009. As a result, the federal banking regulatory agencies reviewed the nineteen largest U.S. banks pursuant to the SCAP,

which is discussed in greater detail in the “Capital Resources” section of this MD&A.

Pursuant to the SCAP results, we executed several transactions as part of a formalized capital plan approved by the Federal

Reserve that increased Tier 1 common equity by $2.3 billion and incidentally raised liquidity at both the Parent Company

and the Bank. The transactions included the sale of $1.8 billion of common stock, a $750 million cash tender for certain

hybrid debt securities, and the sale of various corporate assets. The sale of additional shares of common stock, through both

“at-the-market” and marketed offerings, provided substantial additional long-term liquidity to the Parent Company. The

purchase of hybrid debt securities used approximately $525.0 million of Parent Company liquidity since these hybrid

securities were obligations of the Parent Company. The net effect of these capital actions was to increase Parent Company

liquidity by approximately $1.3 billion. Moreover, the aforementioned asset sales also generated $0.1 billion of liquidity at

the Bank.

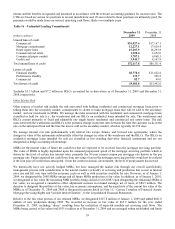

Other Liquidity Considerations. As detailed in Table 16, we had an aggregate potential obligation of $72.1 billion to our

clients in unused lines of credit at December 31, 2009. Commitments to extend credit are arrangements to lend to clients who

have complied with predetermined contractual obligations. We also had $9.0 billion in letters of credit as of December 31,

2009, most of which are standby letters of credit, which require that we provide funding if certain future events occur. Our

lines and letters of credit have declined since December 31, 2008 due to our decision to reduce exposure to certain higher

risk areas, as well as due to clients’ decision not to renew their lines and letters of credit as a result of their decreased need

for these facilities as they pay down their debt and reduce their need for working capital. Approximately $5.5 billion of these

letters as of December 31, 2009 supported VRDOs, as previously discussed. In addition, at December 31, 2009, lines of

credit totaling approximately $3.8 billion supported CP issued by Three Pillars to investors not affiliated with us or Three

Pillars. No amounts are currently outstanding related to Three Pillars’ lines of credit. For more information about Three

Pillars, see Note 11, “Certain Transfers of Financial Assets, Mortgage Servicing Rights and Variable Interest Entities,” to the

Consolidated Financial Statements.

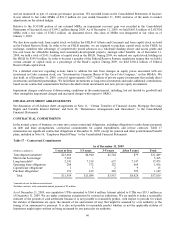

In the third quarter of 2009, the FDIC, in response to the need to replenish DIF balances that declined as a result of recent

bank failures, announced details of a plan to restore DIF balances. The restoration plan, as subsequently approved, required

all FDIC insured banks to prepay their risk-based assessments for the years 2010, 2011, and 2012. The assessments, usually

due quarterly, were instead required to be estimated for the three future years and paid prior to December 31, 2009. In

conjunction with the adoption of this rule, the FDIC also approved a three-basis point increase in assessment rates effective

on January 1, 2011. Our estimate of three future years of assessments under this restoration plan was $924.8 million with the

estimated assessment for 2010 calculated at current rates. We paid that assessment to the FDIC on December 29, 2009 and

concurrently recorded a prepaid asset in that amount within other assets in the Consolidated Balance Sheets. We anticipate

funding any differences between our prepayment and actual amounts due each quarter using our existing available liquidity.

Certain provisions of long-term debt agreements and the lines of credit prevent us from creating liens on, disposing of, or

issuing (except to related parties) voting stock of subsidiaries. Further, there are restrictions on mergers, consolidations,

certain leases, sales or transfers of assets, and minimum shareholders’ equity ratios. As of December 31, 2009, we were and

expect to remain in compliance with all covenants and provisions of these debt agreements.

As of December 31, 2009, our cumulative UTBs amounted to $160.6 million. Interest related to UTBs was $39.3 million as

of December 31, 2009. These UTBs represent the difference between tax positions taken or expected to be taken in our tax

58