SunTrust 2009 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

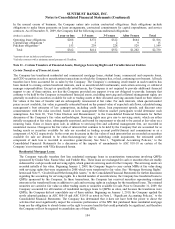

Three Pillars Funding, LLC

SunTrust assists in providing liquidity to select corporate clients by directing them to a multi-seller CP conduit, Three

Pillars. Three Pillars provides financing for direct purchases of financial assets originated and serviced by SunTrust’s

corporate clients by issuing highly rated CP.

The Company’s involvement with Three Pillars includes the following activities: services related to the administration

of Three Pillars’ activities and client referrals to Three Pillars; the issuing of letters of credit, which provide partial

credit protection to the CP holders; and providing liquidity arrangements that would provide funding to Three Pillars in

the event it can no longer issue CP or in certain other circumstances. The Company’s activities with Three Pillars

generated total fee revenue for the Company, net of direct salary and administrative costs incurred by the Company, of

approximately $58.8 million, $48.2 million, and $28.7 million for the years ended December 31, 2009, December 31,

2008, and December 31, 2007, respectively.

Three Pillars has issued a subordinated note to a third party, which matures in March 2015; however, the note holder

may declare the note due and payable upon an event of default, which includes any loss drawn on the note funding

account that remains unreimbursed for 90 days. The subordinated note holder absorbs the first dollar of loss in the event

of nonpayment of any of Three Pillars’ assets. Only the remaining balance of the first loss note, after any incurred

losses, would be due. The outstanding and committed amounts of the subordinated note were $20.0 million at

December 31, 2009 and December 31, 2008, and no losses had been incurred through December 31, 2009. Subsequent

to December 31, 2009, Three Pillars repaid and extinguished the subordinated note.

The Company has determined that Three Pillars is a VIE, as Three Pillars has not issued sufficient equity at risk. The

Company and the holder of the subordinated note are the two significant VI holders in Three Pillars. The Company and

this note holder are not related parties or de facto agents of one another. The Company uses a mathematical model that

calculates the expected losses and expected residual returns of Three Pillars’ assets and operations, based on a Monte

Carlo simulation, and allocates each to the Company and the holder of the subordinated note. The results of this model,

which the Company evaluates monthly, have shown that the holder of the subordinated note absorbs the majority of the

variability of Three Pillars’ expected losses. The Company believes the subordinated note is sized in an amount

sufficient to absorb the expected loss of Three Pillars based on current commitment levels and the forecasted growth in

Three Pillars’ assets; as such, the Company has concluded it is not Three Pillars’ primary beneficiary and is not required

to consolidate Three Pillars. See Note 1, “Significant Accounting Policies,” to the Consolidated Financial Statements for

a discussion of the impacts of the amendments to ASC 810-10 on the Company’s involvement with Three Pillars.

As of December 31, 2009 and December 31, 2008, Three Pillars had assets not included on the Company’s

Consolidated Balance Sheets of approximately $1.8 billion and $3.5 billion, respectively, consisting primarily of

secured loans. Funding commitments and outstanding receivables extended by Three Pillars to its customers totaled $3.7

billion and $1.7 billion, respectively, as of December 31, 2009, almost all of which renew annually, as compared to $5.9

billion and $3.5 billion, respectively, as of December 31, 2008. The majority of the commitments are backed by trade

receivables and commercial loans that have been originated by companies operating across a number of industries

which collateralize 50% and 18%, respectively, of the outstanding commitments, as of December 31, 2009, as compared

to 47% and 20%, respectively, as of December 31, 2008. Assets supporting those commitments have a weighted average

life of 1.25 years and 1.52 years at December 31, 2009 and December 31, 2008, respectively. At December 31, 2009,

Three Pillars’ outstanding CP used to fund the assets totaled approximately $1.8 billion, with remaining weighted

average lives of 5.9 days and maturities through February 2010.

Each transaction added to Three Pillars is typically structured to a minimum implied A/A2 rating according to

established credit and underwriting policies as approved by credit risk management and monitored on a regular basis to

ensure compliance with each transaction’s terms and conditions. Typically, transactions contain dynamic credit

enhancement features that provide increased credit protection in the event asset performance deteriorates. If asset

performance deteriorates beyond predetermined covenant levels, the transaction could become ineligible for continued

funding by Three Pillars. This could result in the transaction being amended with the approval of credit risk

management, or Three Pillars could terminate the transaction and enforce any rights or remedies available, including

amortization of the transaction or liquidation of the collateral. In addition, Three Pillars has the option to fund under the

liquidity facility provided by the Bank in connection with the transaction and may be required to fund under the

liquidity facility if the transaction remains in breach. In addition, each commitment renewal requires credit risk

management approval. The Company is not aware of unfavorable trends related to Three Pillars assets for which the

Company expects to suffer material losses. During the years ended December 31, 2009 and 2008, there were no write-

downs of Three Pillars’ assets.

109