SunTrust 2009 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

created by the assets and liabilities of each segment. The mismatch between funds credits and funds charges at the

segment level resides in Reconciling Items. The change in the matched maturity funds mismatch is generally

attributable to the corporate balance sheet management strategies.

•Provision for credit losses - Represents net charge-offs by segment. The difference between the segment net

charge-offs and the consolidated provision for credit losses is reported in Reconciling Items.

•Provision/(benefit) for income taxes - Calculated using a nominal income tax rate for each segment. This

calculation includes the impact of various income adjustments, such as the reversal of the FTE gross up on

tax-exempt assets, tax adjustments, and credits that are unique to each business segment. The difference between

the calculated provision/(benefit) for income taxes at the segment level and the consolidated provision/(benefit) for

income taxes is reported in Reconciling Items.

The Company continues to augment its internal management reporting methodologies. Currently, the segment’s financial

performance is comprised of direct financial results as well as various allocations that for internal management reporting

purposes provide an enhanced view of analyzing the segment’s financial performance. The internal allocations include the

following:

•Operational Costs – Expenses are charged to the segments based on various statistical volumes multiplied by

activity based cost rates. As a result of the activity based costing process, planned residual expenses are also

allocated to the segments. The recoveries for the majority of these costs are in the Corporate Other and Treasury

segment.

•Support and Overhead Costs – Expenses not directly attributable to a specific segment are allocated based on

various drivers (e.g., number of full-time equivalent employees and volume of loans and deposits). The recoveries

for these allocations are in Corporate Other and Treasury.

•Sales and Referral Credits – Segments may compensate another segment for referring or selling certain products.

The majority of the revenue resides in the segment where the product is ultimately managed.

The application and development of management reporting methodologies is a dynamic process and is subject to periodic

enhancements. The implementation of these enhancements to the internal management reporting methodology may

materially affect the results disclosed for each segment with no impact on consolidated results. Whenever significant changes

to management reporting methodologies take place, the impact of these changes is quantified and prior period information is

reclassified wherever practicable.

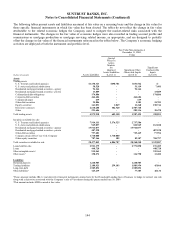

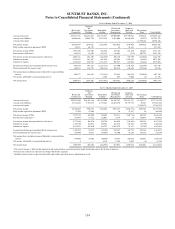

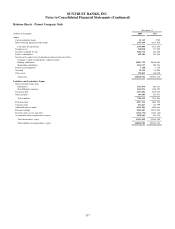

Twelve Months Ended December 31, 2009

(Dollars in thousands)

Retail and

Commercial

Corporate

and

Investment

Banking

Household

Lending

Wealth and

Investment

Management

Corporate

Other and

Treasury

Reconciling

Items Consolidated

Average total assets $56,409,092 $30,897,635 $51,221,820 $8,984,057 $26,690,861 $1,238,958 $175,442,423

Average total liabilities 93,395,855 14,571,273 3,935,072 11,356,812 29,750,582 146,736 153,156,330

Average total equity - - - - - 22,286,093 22,286,093

Net interest income $2,345,576 $316,759 $780,190 $303,954 $419,581 $299,630 $4,465,690

Fully taxable-equivalent adjustment (FTE) 37,269 72,530 - 17 14,054 (581) 123,289

Net interest income (FTE)12,382,845 389,289 780,190 303,971 433,635 299,049 4,588,979

Provision for credit losses21,175,241 298,164 1,683,450 79,166 1,690 826,203 4,063,914

Net interest income after provision for credit losses 1,207,604 91,125 (903,260) 224,805 431,945 (527,154) 525,065

Noninterest income 1,362,990 700,073 727,682 748,551 202,155 (31,173) 3,710,278

Noninterest expense 3,292,965 559,718 1,785,327 863,061 92,908 (31,571) 6,562,408

Income/(loss) before provision/(benefit) for income taxes (722,371) 231,480 (1,960,905) 110,295 541,192 (526,756) (2,327,065)

Provision/(benefit) for income taxes3(241,060) 86,893 (593,021) 42,434 128,563 (199,303) (775,494)

Net income/(loss) including income attributable to

noncontrolling interest (481,311) 144,587 (1,367,884) 67,861 412,629 (327,453) (1,551,571)

Net income attributable to noncontrolling interest - - 2,971 (7) 9,148 - 12,112

Net income/(loss) ($481,311) $144,587 ($1,370,855) $67,868 $403,481 ($327,453) ($1,563,683)

153