SunTrust 2009 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

Accounting Policies Recently Adopted and Pending Accounting Pronouncements

In June 2009, the FASB issued an update to ASC 105-10, “Generally Accepted Accounting Principles”.This standard

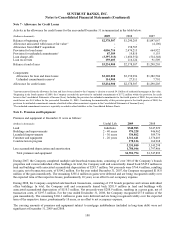

establishes the ASC as the source of authoritative U.S. GAAP recognized by the FASB for nongovernmental entities. The

ASC is effective for interim and annual periods ending after September 15, 2009. The ASC is a reorganization of existing

U.S. GAAP and does not change existing U.S. GAAP. The Company adopted this standard during the third quarter of 2009.

The adoption had no impact on the Company’s financial position, results of operations, and EPS.

In June 2009, the FASB issued ASU 2009-16, an update to ASC 860-10, “Transfers and Servicing,” and ASU 2009-17, an

update to ASC 810-10, “Consolidation”. These updates are effective for the first interim reporting period of 2010. The update

to ASC 860-10 amends the guidance to eliminate the concept of a QSPE and changes some of the requirements for

derecognizing financial assets. The amendments to ASC 810-10 will (a) eliminate the exemption for existing QSPEs from

U.S. GAAP, (b) shift the determination of which enterprise should consolidate a VIE to a current control approach, such that

an entity that has both the power to make decisions and right to receive benefits or absorb losses that could potentially be

significant to the VIE will consolidate a VIE, and (c) change when it is necessary to reassess who should consolidate a VIE.

The Company has analyzed the impacts of these amendments on all QSPEs and VIE structures with which it is involved.

Based on this analysis, the Company expects to consolidate its multi-seller conduit, Three Pillars, and a CLO entity. The

Company will consolidate these entities because certain subsidiaries of the Company have significant decision-making rights

and own VIs that could potentially be significant to these VIEs. The primary balance sheet impacts from consolidating Three

Pillars and the CLO on January 1, 2010, will be increases in loans and leases, the related allowance for loan losses, LHFS,

long-term debt, and other short-term borrowings. The consolidations of Three Pillars and the CLO will have no impact on the

Company’s earnings or cash flows that result from its involvement with these VIEs, but the Company’s Consolidated

Statements of Income/(Loss) will generally reflect a reduction in noninterest income and an increase in net interest income

and noninterest expense due to the consolidations. For additional information on the Company’s VIE structures, refer to

Note 11, “Certain Transfers of Financial Assets, Mortgage Servicing Rights and Variable Interest Entities,” to the

Consolidated Financial Statements.

The combined impact of consolidating Three Pillars and the CLO on January 1, 2010 were incremental total assets and total

liabilities of approximately $2 billion, respectively, and an insignificant impact on shareholders’ equity. No additional

funding requirements with respect to these entities are expected to significantly impact the liquidity position of the Company.

Upon adoption, the Company consolidated the assets and liabilities of Three Pillars at their unpaid principal amounts and will

subsequently account for these assets and liabilities on an accrual basis. Upon adoption, the Company consolidated the assets

and liabilities of the CLO based on their estimated fair values and made an irrevocable election to carry all of the financial

assets and financial liabilities of the CLO at fair value. The pro forma impact on certain of the Company’s regulatory capital

ratios as a result of consolidating Three Pillars and the CLO is not significant.

The Company does not currently believe that it is the primary beneficiary of any other significant off-balance sheet entities

with which it is involved; however, the accounting guidance requires an entity to reassess whether it is the primary

beneficiary at least quarterly. The Company does not currently expect to consolidate additional VIEs in future periods.

In January 2010, the FASB voted to finalize an ASU that would defer the amendments to ASC 810-10 for certain investment

entities that have the attributes of entities subject to the “Investment Company Guide” and for MMMF that comply with or

operate in accordance with requirements that are similar to those included in Rule 2a-7 of the Investment Company Act of

1940. Certain of the Company’s wholly-owned subsidiaries provide investment advisor services for various private

placement and publicly registered investment funds. The Company expects that the deferral will apply to all of these funds.

93