SunTrust 2009 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

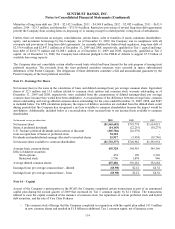

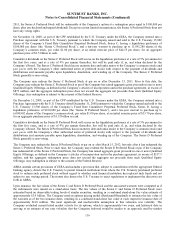

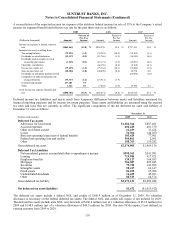

Maturities of long-term debt are: 2010 – $2,142.5 million; 2011 – $4,548.8 million; 2012 – $2,982.6 million; 2013 – $633.9

million; 2014 – $25.3 million; and thereafter—$7,156.4 million. Restrictive provisions of several long-term debt agreements

prevent the Company from creating liens on, disposing of, or issuing (except to related parties) voting stock of subsidiaries.

Further, there are restrictions on mergers, consolidations, certain leases, sales or transfers of assets, minimum shareholders’

equity, and maximum borrowings by the Company. As of December 31, 2009, the Company was in compliance with all

covenants and provisions of long-term debt agreements. As currently defined by federal bank regulators, long-term debt of

$2,356.4 million and $2,847.3 million as of December 31, 2009 and 2008, respectively, qualified as Tier 1 capital and long-

term debt of $2,817.9 million and $3,008.3 million as of December 31, 2009 and 2008, respectively, qualified as Tier 2

capital. As of December 31, 2009, the Company had collateral pledged to the FHLB of Atlanta to support $7.2 billion of

available borrowing capacity.

The Company does not consolidate certain wholly-owned trusts which had been formed for the sole purpose of issuing trust

preferred securities. The proceeds from the trust preferred securities issuances were invested in junior subordinated

debentures of the Parent Company. The obligations of these debentures constitute a full and unconditional guarantee by the

Parent Company of the trust preferred securities.

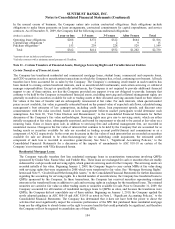

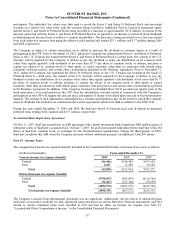

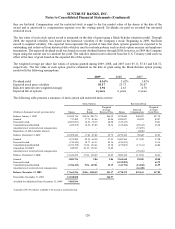

Note 13 - Earnings Per Share

Net income/(loss) is the same in the calculation of basic and diluted earnings/(loss) per average common share. Equivalent

shares of 32.5 million and 33.5 million related to common stock options and common stock warrants outstanding as of

December 31, 2009 and 2008, respectively, were excluded from the computations of diluted earnings/(loss) per average

common share because they would have been antidilutive. A reconciliation of the difference between average basic common

shares outstanding and average diluted common shares outstanding for the years ended December 31, 2009, 2008, and 2007

is included below. For EPS calculation purposes, the impact of dilutive securities are excluded from the diluted share count

during periods that the Company has recognized a net loss available to common shareholders because the impact would be

anti-dilutive. Additionally, included below is a reconciliation of net income/(loss) to net income/(loss) available to common

shareholders.

(In thousands, except per share data) 2009 2008 2007

Net income/(loss) ($1,563,683) $795,774 $1,634,015

Series A preferred dividends (14,143) (22,255) (30,275)

U.S. Treasury preferred dividends and accretion of discount (265,786) (26,579) -

Gain on repurchase of Series A preferred stock 94,318 --

Dividends and undistributed earnings allocated to unvested shares 15,917 (5,958) (10,786)

Net income/(loss) available to common shareholders ($1,733,377) $740,982 $1,592,954

Average basic common shares 435,328 348,919 349,346

Effect of dilutive securities:

Stock options 452 190 2,396

Restricted stock 1,706 1,074 946

Average diluted common shares 437,486 350,183 352,688

Earnings/(loss) per average common share - diluted ($3.98) $2.12 $4.52

Earnings/(loss) per average common share - basic ($3.98) $2.12 $4.56

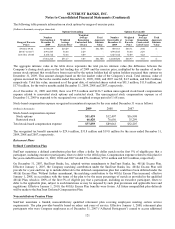

Note 14 – Capital

As part of the Company’s participation in the SCAP, the Company completed certain transactions as part of an announced

capital plan during the second quarter of 2009 that increased its Tier 1 common equity by $2.1 billion. The transactions

utilized to raise the capital consisted of the issuance of common stock, the repurchase of certain preferred stock and hybrid

debt securities, and the sale of Visa Class B shares.

• The common stock offerings that the Company completed in conjunction with the capital plan added 141.9 million

in new common shares and resulted in $1.8 billion in additional Tier 1 common equity, net of issuance costs.

114