SunTrust 2009 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

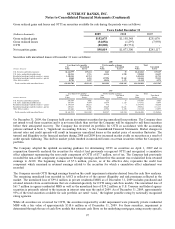

Accordingly, the Company calculated net income available to common shareholders pursuant to the two-class method,

whereby net income is allocated between common shareholders and participating securities. In periods of net loss, no

allocation is made to participating securities as they are not contractually required to fund net losses.

Net income available to common shareholders represents net income/(loss) after preferred stock dividends, accretion of the

discount on preferred stock issuances, income impact of any repurchases of preferred stock, and dividends and allocation of

undistributed earnings to the participating securities. For additional information on the Company’s EPS, refer to Note 13,

“Earnings Per Share,” to the Consolidated Financial Statements.

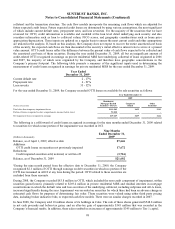

Guarantees

The Company recognizes a liability at the inception of a guarantee, in an amount equal to the estimated fair value of the

obligation. A guarantee is defined as a contract that contingently requires a company to pay a guaranteed party upon changes

in an underlying asset, liability or equity security of the guaranteed party, or upon failure of a third-party to perform under a

specified agreement. The Company considers the following arrangements to be guarantees: certain asset purchase

agreements, standby letters of credit and financial guarantees, certain indemnification agreements included within third-party

contractual arrangements and certain derivative contracts. For additional information on the Company’s guarantor

obligations, refer to Note 18, “Reinsurance Arrangements and Guarantees,” to the Consolidated Financial Statements.

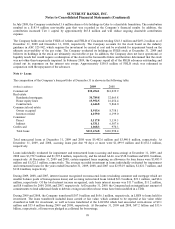

Derivative Financial Instruments

The Company records all contracts that satisfy the definition of a derivative, at fair value in the Consolidated Balance Sheets.

The Company enters into various derivatives in a dealer capacity to facilitate client transactions and as a risk management

tool. Derivatives entered into in a dealer capacity and those that either do not qualify for, or for which the Company has

elected not to apply, hedge accounting are accounted for as freestanding derivatives. In addition to freestanding derivative

instruments, the Company evaluates contracts such as brokered deposits and short-term debt to determine whether any

embedded derivatives exist and whether any of those embedded derivatives are required to be bifurcated and separately

accounted for as freestanding. If embedded derivatives are not bifurcated, then the entire contract is valued at fair value. In

addition, as a normal part of its operations, the Company enters into certain IRLCs on mortgage loans that are accounted for

as freestanding derivatives. Changes in the fair value of freestanding derivatives are recorded in noninterest income.

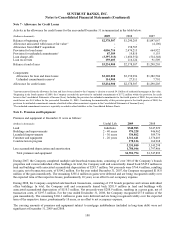

Where derivatives have been used in client transactions, the Company generally manages the risk associated with these contracts

within the framework of its VAR approach that monitors total exposure daily and seeks to manage the exposure on an overall

basis. Derivatives are used as a risk management tool to hedge the Company’s exposure to changes in interest rates or other

identified market risks. The Company accounts for some of these derivatives as hedging instruments based on hedge accounting

provisions. The Company prepares written hedge documentation for all derivatives which are designated as (1) a hedge of the

fair value of a recognized asset or liability (fair value hedge) or (2) a hedge of a forecasted transaction, such as, the variability of

cash flows to be received or paid related to a recognized asset or liability (cash flow hedge). The written hedge documentation

includes identification of, among other items, the risk management objective, hedging instrument, hedged item and

methodologies for assessing and measuring hedge effectiveness and ineffectiveness, along with support for management’s

assertion that the hedge will be highly effective. Methodologies related to hedge effectiveness and ineffectiveness are consistent

between similar types of hedge transactions and have included (i) statistical regression analysis of changes in the cash flows of

the actual derivative and a perfectly effective hypothetical derivative, (ii) statistical regression analysis of changes in the fair

values of the actual derivative and the hedged item and (iii) comparison of the critical terms of the hedged item and the hedging

derivative. For designated hedging relationships, the Company performs retrospective and prospective effectiveness testing

using quantitative methods and generally does not assume perfect effectiveness through the matching of critical terms. Changes

in the fair value of a derivative that is highly effective and that has been designated and qualifies as a fair value hedge are

recorded in current period earnings, along with the changes in the fair value of the hedged item that are attributable to the

hedged risk. Changes in the fair value of a derivative that is highly effective and that has been designated and qualifies as a cash

flow hedge are initially recorded in AOCI and reclassified to earnings in the same period that the hedged item impacts earnings;

and any ineffective portion is recorded in current period earnings. Assessments of hedge effectiveness and measurements of

hedge ineffectiveness are performed at least quarterly for ongoing effectiveness. Hedge accounting ceases on transactions that

are no longer deemed effective, or for which the derivative has been terminated or de-designated. For discontinued fair value

hedges where the hedged item remains outstanding, the hedged item would cease to be remeasured at fair value attributable to

changes in the hedged risk and any existing basis adjustment would be recognized as a yield adjustment over the remaining life

of the hedged item. For discontinued cash flow hedges where the hedged transaction remains probable to occur as originally

designated, the unrealized gains and losses recorded in AOCI would be reclassified to earnings in the period when the

previously designated hedged cash flows occur. If the previously designated transaction were no longer probable of occurring,

any unrealized gains and losses in AOCI would be immediately reclassified to earnings.

91