SunTrust 2009 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

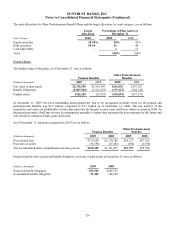

Cash Flow Hedges

The Company utilizes a comprehensive risk management strategy to monitor sensitivity of earnings to movements in

interest rates. Specific types of funding and principal amounts hedged are determined based on prevailing market

conditions and the shape of the yield curve. In conjunction with this strategy, the Company employs various interest rate

derivatives as risk management tools to hedge interest rate risk from recognized assets and liabilities or from forecasted

transactions. The terms and notional amounts of derivatives are determined based on management’s assessment of

future interest rates, as well as other factors. The Company establishes parameters for derivative usage, including

identification of assets and liabilities to hedge, derivative instruments to be utilized, and notional amounts of hedging

relationships. At December 31, 2009, the Company’s only outstanding interest rate hedging relationships relate to

interest rate swaps that have been designated as cash flow hedges of probable forecasted transactions related to

recognized floating rate loans.

Interest rate swaps have been designated as hedging the exposure to the benchmark interest rate risk associated with

floating rate loans. The maximum range of hedge maturities for hedges of floating rate loans is approximately one to

five years, with the weighted average being approximately 3.3 years. Ineffectiveness on these hedges was de minimis

during the year ended December 31, 2009. As of December 31, 2009, $346.7 million, net of tax, of the deferred net

gains on derivatives that are recorded in AOCI are expected to be reclassified to net interest income over the next twelve

months in connection with the recognition of interest income on these hedged items.

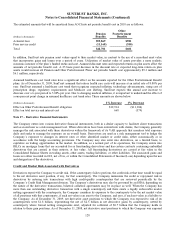

During the third quarter of 2008, the Company executed The Agreements on 30 million common shares of Coke. A

consolidated subsidiary of SunTrust owns approximately 22.9 million Coke common shares and a consolidated

subsidiary of SunTrust Bank owns approximately 7.1 million Coke common shares. These two subsidiaries entered into

separate Agreements on their respective holdings of Coke common shares with a large, unaffiliated financial institution

(the “Counterparty”). Execution of The Agreements (including the pledges of the Coke common shares pursuant to the

terms of The Agreements) did not constitute a sale of the Coke common shares under U.S. GAAP for several reasons,

including that ownership of the common shares was not legally transferred to the Counterparty. The Agreements

resulted in zero cost equity collars which are derivatives in their entirety. The Company has designated The Agreements

as cash flow hedges of the Company’s probable forecasted sales of its Coke common shares, which are expected to

occur in approximately six and a half and seven years from The Agreements’ effective date, for overall price volatility

below the strike prices on the floor (purchased put) and above the strike prices on the ceiling (written call). Although the

Company is not required to deliver its Coke common shares under The Agreements, the Company has asserted that it is

probable that it will sell all of its Coke common shares at or around the settlement date of The Agreements. The Federal

Reserve’s approval for Tier 1 capital was significantly based on this expected disposition of the Coke common shares

under The Agreements or in another market transaction. Both the sale and the timing of such sale remain probable to

occur as designated. At least quarterly, the Company assesses hedge effectiveness and measures hedge ineffectiveness

with the effective portion of the changes in fair value of The Agreements recorded in AOCI and any ineffective portions

recorded in trading account profits and commissions. None of the components of The Agreements’ fair values are

excluded from the Company’s assessments of hedge effectiveness. Potential sources of ineffectiveness include changes

in market dividends and certain early termination provisions. The Company did not recognize any ineffectiveness

during 2008, but did recognize approximately $0.6 million of ineffectiveness during the year ended December 31, 2009,

which was recorded in trading account profits and commissions.Other than potential measured hedge ineffectiveness,

no amounts will be reclassified from AOCI over the next twelve months and any remaining amounts recorded in AOCI

will be reclassified to earnings when the probable forecasted sales of the Coke common shares occur.

Economic Hedging and Trading Activities

In addition to designated hedging relationships, the Company also enters into derivatives as an end user as a risk

management tool to economically hedge risks associated with certain non-derivative and derivative instruments, along

with entering into derivatives in a trading capacity with its clients.

The primary risks that the Company economically hedges are interest rate risk, foreign exchange risk, and credit risk.

The economic hedging activities are accomplished by entering into individual derivatives or by using derivatives on a

macro basis, and generally accomplish the Company’s goal of mitigating the targeted risk. To the extent that specific

derivatives are associated with specific hedged items, the notional amounts, fair values, and gains/(losses) on the

derivatives are illustrated in the tables above.

133