SunTrust 2009 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2009 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

Securities Available for Sale and Trading Assets

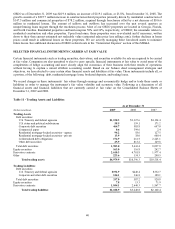

Our level 3 securities available for sale totals approximately $1.3 billion at December 31, 2009, including FHLB and

Federal Reserve Bank stock, as well as certain municipal bond securities, some of which are only redeemable with the

issuer at par and cannot be traded in the market; as such, no significant observable market data for these instruments is

available. These nonmarketable securities total approximately $836.9 million at December 31, 2009. Level 3 trading

assets total approximately $390.1 million at December 31, 2009. The remaining level 3 securities, both trading assets

and available for sale securities, are predominantly private MBS and collateral debt obligations, including interests

retained from Company-sponsored securitizations or purchased from third-party securitizations and investments in

SIVs. We have also increased our exposure to bank trust preferred ABS, student loan ABS, and municipal securities due

to our purchase of certain ARS as a result of failed auctions. For all of the Level 3 securities, little or no market activity

exists for either the security or the underlying collateral and therefore the significant assumptions used to value the

securities are not market observable. Approximately half of the collateral in the remaining level 3 securities includes

direct or repackaged exposure to residential mortgages which is predominantly secured by 2007 vintage prime first lien

mortgage loans, however, there is also exposure to prime first and second lien mortgages, as well as subprime first and

second lien mortgages that were originated from 2003 through 2007. Level 3 trading liabilities consists of the Coke

derivative valued at approximately $45.9 million at December 31, 2009.

ARS purchased since the auction rate market began failing in February 2008 have been considered level 3 securities due

to the significant decrease in the volume and level of activity in these markets which has necessitated the use of

significant unobservable inputs into our valuations. We classify ARS as securities available for sale or trading securities.

As of December 31, 2009, the fair value of ARS purchased is approximately $176.4 million in trading assets and $156.4

million in available for sale securities. ARS include municipal bonds, nonmarketable preferred equity securities, and

ABS collateralized by student loans or trust preferred bank obligations. Under a functioning market, ARS could be

remarketed with tight interest rate caps to investors targeting short-term investment securities that repriced generally

every 7 to 28 days. Unlike other short-term instruments, these ARS do not benefit from backup liquidity lines or letters

of credit and, therefore, as auctions began to fail, investors were left with securities that were more akin to longer-term,

20-30 year, illiquid bonds, with the anticipation that auctions will continue to fail in the foreseeable future. The

combination of materially increased tenors, capped interest rates and general market illiquidity has had a significant

impact on the risk profiles of these securities and has resulted in the use of valuation techniques and models that rely on

significant inputs that are largely unobservable.

We saw a reduction in our level 3 portfolios during 2009 due to sales, paydowns, transfers of assets from level 3 to level

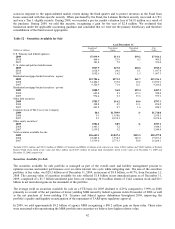

2, and/or continued deterioration in values of certain securities, in particular, private MBS. At December 31, 2009, we

hold assets in two SIVs that are in receivership and are carried at a fair value of approximately $126.1 million. Our

holdings of SIV assets decreased by $61.9 million during 2009, due to settlements or partial paydown of approximately

$83.6 million, offset by gains of approximately $21.7 million. The gain resulted primarily from the improvement in the

cash positions of the SIVs as well as modest improvements in the value of the underlying assets. Our level 3 portfolio

has experienced a significant number and amount of downgrades during this time of economic turmoil. While our level

3 municipal securities and equity securities are of high credit quality, certain vintages of private MBS have suffered

from deterioration in credit quality leading to downgrades. At December 31, 2009, our private MBS contained

approximately $314 million of 2007 vintage securities available for sale and trading securities and approximately $19

million of 1999-2006 vintage securities available for sale and trading securities that had been downgraded to

non-investment grade levels by at least one nationally recognized rating agency. The vast majority of these securities

had high investment grade ratings at the time of origination or purchase. All of these securities that are classified as

available for sale are also included as part of our quarterly OTTI evaluation process. See Note 5, “Securities Available

for Sale,” to the Consolidated Financial Statements for details regarding impairment recognized through earnings on

private MBS during the year ended December 31, 2009.

Residual and other retained interests classified as securities available for sale or trading securities are valued based on

internal models that incorporate assumptions, such as prepayment speeds, estimated credit losses, and discount rates

which are generally not observable in the current markets. Generally, we attempt to obtain pricing for our securities

from a third party pricing provider or third party brokers who have experience in valuing certain investments. This

pricing may be used as either direct support for our valuations or used to validate outputs from our own proprietary

models. We evaluate third party pricing to determine the reasonableness of the information relative to changes in market

data such as any recent trades we executed, market information received from outside market participants and analysts,

and/or changes in the underlying collateral performance. When actual trades are not available to corroborate pricing

information received, we will use industry standard or proprietary models to estimate fair value, and will consider

assumptions such as relevant market indices that correlate to the underlying collateral, prepayment speeds, default rates,

loss severity rates, and discount rates.

Due to the continued illiquidity and credit risk of level 3 securities, these market values are highly sensitive to

assumption changes and market volatility. In many instances, pricing assumptions for level 3 securities may fall within

45