Telus 2011 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2011 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

TELUS 2011 ANNUAL REPORT . 45

MANAGEMENT’S DISCUSSION & ANALYSIS: 1

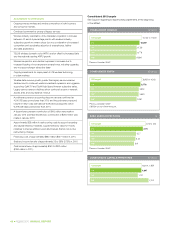

Assumptions for 2011 original targets Results or expectations

A preliminary pension accounting discount rate

was estimated at 5.35% and subsequently set

at 5.25% (60 basis points lower than 2010) and

the preliminary expected long-term return estimated

at 7.25% was subsequently set at 7% (25 basis

points lower than 2010). The defined benefit

pension plans net recovery was set at $34 million

Confirmed. The defined benefit pension plan recovery was $34 million in 2011. Defined benefit

pension plan expenses (recoveries) are set at the beginning of the year.

Defined benefit pension plan contributions,

including a $200 million discretionary contribution,

were estimated to be $298 million in 2011,

up from $137 million in 2010

Confirmed. Contributions to defined benefit plans were $298 million in 2011, including the

$200 million discretionary contribution made in January 2011.

Efficiency initiatives expected to result in

approximately $50 million in restructuring costs

in 2011 ($80 million in 2010 (IFRS)). Incremental

EBITDA savings for 2011, initially estimated at

approximately $75 million, were subsequently

revised to approximately $50 million (incremental

savings of $134 million in 2010)

In 2011, restructuring costs were $35 million, comprised of people-related initiatives and

other initiatives, including the consolidation of real estate. Incremental EBITDA savings were

approximately $69 million.

A reduction in financing costs of approximately

$135 million due to lower debt levels and

interest rates

Confirmed. Financing costs decreased by $145 million in 2011 due to a lower effective interest

rate, lack of an early redemption charge as recorded in 2010 and, to a lesser extent, lower

average debt.

Statutory income tax rate of approximately

26.5 to 27.5% (29% in 2010)

Confirmed. In 2011, the blended statutory income tax rate was 27.2%, while the effective tax rate

was 23.6%.

Cash income taxes of approximately

$130 to $180 million ($311 million in 2010)

Confirmed. The Company revised its full-year expectation to the top half of the original target

range on May 5, 2011, and subsequently, to $150 to $190 million on August 5, 2011. Cash income

taxes paid net of refunds received were $150 million, comprised of instalments for 2011 and final

payments for the 2010 tax year made early in 2011.

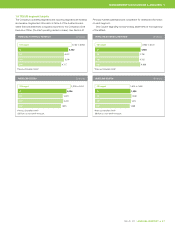

1.5 Financial and operating targets for 2012

The following discussion and assumptions apply to TELUS’ 2012

targets presented in the Scorecard in Section 1.4. The 2012 targets and

assumptions were originally announced on December 16, 2011, in the

Company’s annual financial targets news release and accompanying

investor conference call and webcast.

For 2012, consolidated revenue and EBITDA are expected to benefit

from TELUS’ continued strong execution in wireless and data. Basic

earnings per share is targeted to be 0 to 10% higher due to operating

earnings growth and lower financing costs.

TELUS wireless revenue is forecast to increase principally due to

subscriber growth, and possible ARPU growth. Subscriber loading is

expected to benefit from a Canadian wireless industry penetration gain

similar to 2011 of approximately four to 4.5 percentage points. TELUS

expects to continue to benefit from the Company’s HSPA+ and LTE

network investments, resulting in continued growth, in data and roaming

revenues that will help offset continued declines in voice ARPU. Wireless

EBITDA is expected to increase due to revenue growth, accompanied

by continued large investments in smartphone customer acquisition and

retention costs.

Wireline revenue is expected to reflect continued data revenue

growth from Optik TV and high-speed Internet services, as well as from

business services, offset by continued decreases in local and long dis-

tance service legacy revenues. Wireline EBITDA is expected to decrease,

or post a slight increase, as growth in lower margin data services

including Optik TV is not expected to fully offset declines in higher

margin legacy services.

Consolidated capital expenditures are expected to be at about

the same level as in 2011, or approximately $1.85 billion, driven by

wireless capacity upgrades and ongoing deployment of a new LTE

wireless network in urban markets. While wireline capital investments

are expected to decline, TELUS intends to continue its broadband

infrastructure expansion and upgrades to support strong ongoing growth

in Optik TV and high-speed Internet services. This includes completing

the overlay of VDSL2 technology in Western Canada and VDSL2 bonding

in Eastern Quebec, as well as investing in new state-of-the-art Internet

data centres to support market demand and internal requirements for

cloud computing services. Due to revenue growth, consolidated capital

intensity is expected to be approximately 17% of revenue in 2012,

down from 18% in 2011.

TELUS made a $100 million discretionary special contribution

to its defined benefit pension plans in January 2012. After including this

contri bution, TELUS’ aggregate funded position for its defined benefit

pension plans is expected to be approximately 90% on a solvency basis.

The accelerated discretionary contribution will benefit the 2012 pension

recovery for accounting purposes and, since pension contributions are

tax deductible, reduce cash taxes by approximately $25 million. The

Company’s 2012 pension recovery was initially estimated to be $6 million

and has been revised to an estimated $12 million, or $22 million lower

than in 2011.