Telus 2011 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2011 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182

|

|

TELUS 2011 ANNUAL REPORT . 169

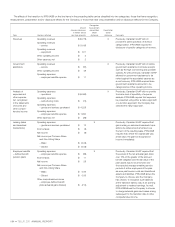

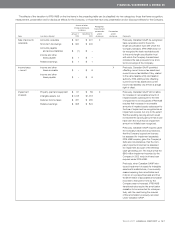

FINANCIAL STATEMENTS & NOTES: 25

Topic

Amount of effect Recognition,

(increase (decrease), measurement,

in millions) presentation Presentation

January 1, December 31, and/or and/or

Line items affected 2010 2010 disclosure disclosure

Comments

Classification of

long-term credit

facility borrowings

Current maturities X

of long-term debt $ß 467 $ß 104

Long-term debt $ (467) $ (104)

Previously, Canadian GAAP provided that

when a debtor used short-term obligations

drawn on a long-term credit facility and

which were subsequently “rolled over”

(e.g. commercial paper), such obligations

were permitted to be classified as a non-

current debt if the underlying long-term

credit facility was classified as non-current.

IFRS-IASB requires that such short-term

obligations drawn on a long-term credit

facility be classified as a current debt.

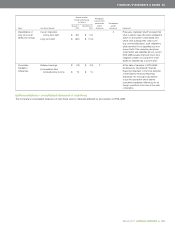

Cumulative

translation

differences

Retained earnings $ (19) $ (19) X

Accumulated other

comprehensive income $ß 19 $ß 19

At the date of transition to IFRS-IASB,

as allowed by International Financial

Reporting Standard 1, First-time Adoption

of International Financial Reporting

Standards, the Company has elected

to use the exemption which deems

cumulative translation differences for all

foreign operations to be zero at the date

of transition.

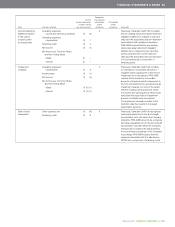

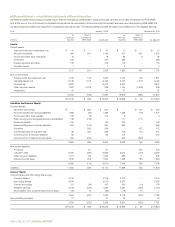

(e) Reconciliations – consolidated statement of cash flows

The Company’s consolidated statement of cash flows was not materially affected by the transition to IFRS-IASB.