Telus 2011 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2011 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

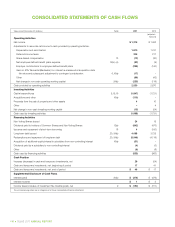

TELUS 2011 ANNUAL REPORT . 101

MANAGEMENT’S DISCUSSION & ANALYSIS: 11

11.2 Free cash flow

Free cash flow does not have any standardized meaning prescribed

by IFRS-IASB and should not be considered an alternative to the

Consolidated statements of cash flows. TELUS reports free cash flow

because it is a key measure used by management to evaluate the

Company’s performance. Free cash flow excludes certain working capital

changes and other sources and uses of cash, as found in the Consoli-

dated statements of cash flows. Investors are cautioned that free cash

flow as reported by TELUS may not be comparable to free cash flow

reported by other companies, and differs from standardized free cash

flow defined by the CICA’s Canadian Performance Reporting Board.

Management’s definition of free cash flow provides an indication of how

much cash generated by operations is available after capital expendi-

tures, but before dividends, acquisitions, proceeds from divested assets

and changes in certain working capital items (such as trade receivables

and trade payables).

Free cash flow calculation

Years ended December 31 ($ millions) 2 0 11 2010

EBITDA (see Section 11.1) 3,778 3,650

Deduct Transactel gain (17) –

Restructuring costs net of cash payments (48) (24)

Items from the Consolidated statements of cash flows

Share-based compensation (12) (30)

Net employee defined benefit plans

expense (recovery) (32) (9)

Employer contributions to employee

defined benefit plans (298) (140)

Interest paid (378) (479)

Interest received 1 3

Income taxes refunded (paid), net (150) (311)

Capital expenditures (1,847) (1,721)

Free cash flow (management’s definition) 997 939

The Canadian Performance Reporting Board defined standardized

free cash flow to foster comparability of the measure between entities.

Standardized free cash flow is an indication of an entity’s capacity to

generate discretionary cash from operations, comprising cash flows from

operating activities less net capital expenditures and those dividends

that are more representative of interest costs. It does not necessarily

represent the cash flow in the period available for management to use

at its discretion, which may be affected by other sources and non-

discretionary uses of cash. The following reconciles management’s

definition of free cash flow with standardized free cash flow and Cash

provided by operating activities.

Free cash flow reconciliation

Years ended December 31 ($ millions) 2 0 11 2010

Cash provided by operating activities 2,550 2,670

Deduct stipulated dividends n/a n/a

Deduct capital expenditures (1,847) (1,721)

Proceeds from disposition of capital assets 4 1

Standardized free cash flow (CICA guideline) 707 950

Deduct proceeds from disposition of capital assets (4) (1)

Adjustments to reconcile to cash provided

by operating activities 294 (10)

Free cash flow (management’s definition) 997 939

11.3 Definitions of wireless operating indicators

These measures are industry metrics and are useful in assessing the

operating performance of a wireless company.

Average revenue per subscriber unit per month (ARPU) is calcu-

lated as Network revenue divided by the average number of subscriber

units on the network during the period and expressed as a rate per

month. Data ARPU is a component of ARPU, calculated on the same

basis for revenue derived from services such as text messaging,

mobile computing, personal digital assistance devices, Internet browser

activity and pay-per-use downloads.

Churn per month is calculated as the number of subscriber units

disconnected during a given period divided by the average number of

subscriber units on the network during the period, and expressed as

a rate per month. A prepaid subscriber is disconnected when the sub-

scriber has no usage for 90 days following expiry of the prepaid card.

Cost of acquisition (COA) consists of the total of handset subsidies,

commissions, and advertising and promotion expenses related to the

initial subscriber acquisition during a given period. As defined, COA

excludes costs to retain existing subscribers (retention spend).

COA per gross subscriber addition is calculated as cost of acquisition

divided by gross subscriber activations during the period.

Retention spend to Network revenue represents direct costs

associated with marketing and promotional efforts aimed at the retention

of the existing subscriber base divided by Network revenue.

11.4 Definitions of liquidity and capital resource measures

Earnings coverage is defined in the Canadian Securities

Administrators’ National Instrument 41-101 and related instruments,

calculated on a 12-month trailing basis.

Calculation of Earnings coverage

Years ended December 31

($ millions, except ratio) 2 0 11 2010

Net income attributable to Common Shares

and Non-Voting Shares 1,219 1,048

Income taxes 376 335

Gross interest expense (Note 8 of the

Audited consolidated financial statements) 389 527

Numerator 1,984 1,910

Denominator – Gross interest expense 389 527

Ratio (times) 5.1 3.6

The following measures do not have any standardized meaning

prescribed by IFRS-IASB and may not be comparable to similar

measures presented by other issuers.

Dividend payout ratio and dividend payout ratio of adjusted net

earnings: The basic measure is defined as the quarterly dividend

declared per Common Share and Non-Voting Share for the most recently

completed quarter, as reported in the Consolidated financial statements,

multiplied by four and divided by the sum of basic earnings per share

for the most recent four quarters for interim reporting periods (divided

by annual basic earnings per share for fiscal years). The target guideline

for the annual dividend payout ratio is on a prospective basis, rather

than on a trailing basis, and is 55 to 65% of sustainable net earnings.