Telus 2011 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2011 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

44 . TELUS 2011 ANNUAL REPORT

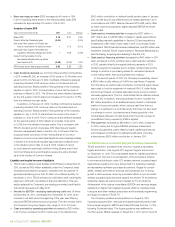

The following key assumptions were made at the time the 2011 targets were announced in December 2010. Preliminary pension assumptions were

revised in the 2010 MD&A dated February 24, 2011, as noted.

Assumptions for 2011 original targets Results or expectations

Ongoing intense wireline and wireless

competition in both business and consumer

markets

Confirmed by: (i) Activities of the dominant Internet and TV service provider in Western Canada,

Shaw Communications, such as the introduction of new generation PVRs, increases in certain

Internet service speeds, more customization choices for TV, Internet and home phone services,

and continued promotional discounts to new subscribers; (ii) wireless entrants pursuing subscriber

growth by using forms of unlimited and flat-rate voice, text and data plans, as well as adopting

a device subsidy approach and beginning to offer smartphones; and (iii) the loss of a federal

government wireless contract to a low-priced bid by an incumbent competitor, which contributed

11 basis points to higher churn in 2011.

Despite ongoing intense competition, TELUS has experienced more moderate residential NAL

losses due to the positive effect of bundled service offers including Optik TV and Optik High

Speed Internet services. TELUS has also experienced more moderate losses in business NALs

in 2011 when compared to 2010, due in part to the implementation of wholesale lines in the

first half of 2011.

Nine facilities-based wireless carriers operated in Canada in 2011: three established national

companies (TELUS, Bell Mobility and Rogers Wireless); two provincial incumbents (SaskTel

Mobility and MTS Mobility); and four new entrants (Wind, Videotron, Public Mobile and Mobilicity).

The four new entrants expanded their market coverage in 2011, and captured an estimated

more than one-third share of total market net additions in 2011 or about 4% of the cumulative

subscriber market.

New entrant EastLink is expected to begin providing services in Atlantic Canada in 2012.

In contrast, Shaw announced in September that it had stopped construction of a conventional

wireless network and service in Western Canada due to high costs and other factors. Instead,

Shaw announced that it is building metropolitan area Wi-Fi networks using unlicensed public

spectrum to extend delivery of its services beyond the home.

Continued downward re-pricing of legacy services Confirmed. Ongoing price competition and net losses in network access lines, net of local rate

increases were reflected in an 8.1% decline in wireline voice local revenues and a 10% decline

in wireline long distance revenue.

Wireless industry penetration of the Canadian

popu lation to increase between 4.5 and

5.0 per centage points, with wireless industry

subscriber growth to accelerate due to a

combination of increased competition, accel -

erated adoption of smartphones and use of

data applications, and the emergence of new

types of wireless devices such as tablets

The popularity of smartphones is confirmed, as evidenced by a smartphone adoption rate of

74% of TELUS’ fourth quarter gross postpaid additions, up from 46% in the fourth quarter of 2010.

TELUS estimates the wireless industry penetration gain in 2011 is slightly lower than expected,

at approximately 4.3 percentage points.

TELUS wireless domestic voice ARPU erosion

offset by increases in data and international

roaming ARPU growth

Confirmed. A 9.4% decline in voice ARPU was more than offset by a 38% increase in data ARPU,

resulting in a 2.5% increase in blended ARPU. International roaming ARPU grew due to the

expanding base of HSPA devices and new international roaming agreements. CDMA devices,

which are a decreasing proportion of the subscriber base, have limited international roaming

capability as few countries outside Canada and the United States implemented this technology.

Wireless acquisition and retention expenses

to increase due to increases in loading

of smartphones, including upgrades, and

to support a larger subscriber base

Confirmed. Wireless COA per gross subscriber addition was $386 in 2011, up 10% from 2010,

while total COA costs were $694 million in 2011, up 16% from 2010. Retention spending as a

percentage of network revenue was 12.4% in 2011, up from 11.6% in 2010, while total retention

costs were $626 million, up 17% from 2010. These increases were substantially caused by higher

device subsidies arising from higher sales of smartphones and greater competitive intensity.

Continued wireline broadband expansion

and upgrades supporting Optik TV and Optik

High Speed Internet subscriber revenue

growth that offsets the continued erosion

in NAL-related revenues

Confirmed. See Building national capabilities in Section 2.2 for expansion and upgrade activities

in 2011. Total subscriptions to TELUS TV and high-speed Internet increased by 271,000 in 2011,

exceeding the 164,000 combined decrease in total NALs and dial-up Internet subscriptions for the

same period. As a result, TELUS had its first increase in total wireline customer connections in

seven years.

Total wireline data revenues increased by $310 million in 2011, including growth in revenue from

Optik TV and Optik High Speed Internet services, which more than offset the $173 million net

decline in legacy wireline voice local, long distance and other revenues.