Duke Energy 2013 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2013 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

|

|

162

PART II

DUKE ENERGY CORPORATION • DUKE ENERGY CAROLINAS, LLC • PROGRESS ENERGY, INC. •

DUKE ENERGY PROGRESS, INC. • DUKE ENERGY FLORIDA, INC. • DUKE ENERGY OHIO, INC. • DUKE ENERGY INDIANA, INC.

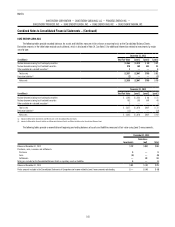

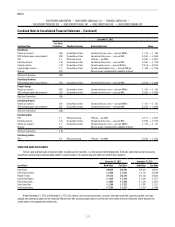

Combined Notes to Consolidated Financial Statements – (Continued)

16. FAIR VALUE MEASUREMENTS

Fair value is the exchange price to sell an asset or transfer a liability in

an orderly transaction between market participants at the measurement date.

The fair value definition focuses on an exit price versus the acquisition cost.

Fair value measurements use market data or assumptions market participants

would use in pricing the asset or liability, including assumptions about risk and

the risks inherent in the inputs to the valuation technique. These inputs may

be readily observable, corroborated by market data, or generally unobservable.

Valuation techniques maximize the use of observable inputs and minimize use

of unobservable inputs. A midmarket pricing convention (the midpoint price

between bid and ask prices) is permitted for use as a practical expedient.

Fair value measurements are classified in three levels based on the fair

value hierarchy:

Level 1 — Unadjusted quoted prices in active markets for identical assets

or liabilities that the reporting entity can access at the measurement date. An

active market is one in which transactions for an asset or liability occur with

sufficient frequency and volume to provide ongoing pricing information.

Level 2 — A fair value measurement utilizing inputs other than quoted prices

included in Level 1 that are observable, either directly or indirectly, for an asset

or liability. Inputs include (i) quoted prices for similar assets or liabilities in

active markets, (ii) quoted prices for identical or similar assets or liabilities in

markets that are not active, (iii) and inputs other than quoted market prices that

are observable for the asset or liability, such as interest rate curves and yield

curves observable at commonly quoted intervals, volatilities, and credit spreads.

A Level 2 measurement cannot have more than an insignificant portion of its

valuation based on unobservable inputs. Instruments in this category include

non-exchange-traded derivatives, such as over-the-counter forwards, swaps

and options; certain marketable debt securities; and financial instruments

traded in less than active markets.

Level 3 — Any fair value measurement which includes unobservable inputs

for more than an insignificant portion of the valuation. These inputs may be

used with internally developed methodologies that result in management’s

best estimate of fair value. Level 3 measurements may include longer-term

instruments that extend into periods in which observable inputs are not

available.

The fair value accounting guidance permits entities to elect to measure

certain financial instruments that are not required to be accounted for at fair

value, such as equity method investments or the company’s own debt, at fair

value. The Duke Energy Registrants have not elected to record any of these

items at fair value.

Transfers between levels represent assets or liabilities that were

previously (i) categorized at a higher level for which the inputs to the estimate

became less observable or (ii) classified at a lower level for which the inputs

became more observable during the period. The Duke Energy Registrant’s policy

is to recognize transfers between levels of the fair value hierarchy at the end

of the period. There were no transfers between levels 1 and 2 during the years

ended December 31, 2013 and 2012. Transfers out of Level 3 during the year

ended December 31, 2013 are the result of forward commodity prices becoming

observable due to the passage of time.

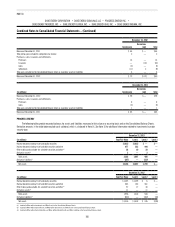

Valuation methods of the primary fair value measurements disclosed

below are as follows.

Investments in equity securities

The majority of investments in equity securities are valued using Level 1

measurements. Investments in equity securities are typically valued at the closing

price in the principal active market as of the last business day of the quarter.

Principal active markets for equity prices include published exchanges such as

NASDAQ and NYSE. Foreign equity prices are translated from their trading currency

using the currency exchange rate in effect at the close of the principal active

market. There was no after-hours market activity that was required to be reflected

in the reported fair value measurements. Investments in equity securities that are

Level 2 or 3 are typically ownership interests in commingled investment funds.

Investments in debt securities

Most investments in debt securities are valued using Level 2

measurements because the valuations uses interest rate curves and credit

spreads applied to the terms of the debt instrument (maturity and coupon

interest rate) and consider the counterparty credit rating. If the market for a

particular fixed income security is relatively inactive or illiquid, the measurement

is Level 3.

Commodity derivatives

Commodity derivatives with clearinghouses are classified as Level 1.

Other commodity derivatives are primarily fair valued using internally developed

discounted cash flow models which incorporate forward price, adjustments for

liquidity (bid-ask spread) and credit or non-performance risk (after reflecting

credit enhancements such as collateral), and are discounted to present value.

Pricing inputs are derived from published exchange transaction prices and

other observable data sources. In the absence of an active market, the last

available price may be used. If forward price curves are not observable for

the full term of the contract and the unobservable period had more than an

insignificant impact on the valuation, the commodity derivative is classified as

Level 3. In isolation, increases (decreases) in natural gas forward prices result

in favorable (unfavorable) fair value adjustments for gas purchase contracts;

and increases (decreases) in electricity forward prices result in unfavorable

(favorable) fair value adjustments for electricity sales contracts. Duke Energy

regularly evaluates and validates pricing inputs used to estimate fair value of

gas commodity contracts by a market participant price verification procedure.

This procedure provides a comparison of internal forward commodity curves to

market participant generated curves.

Interest rate derivatives

Most over-the-counter interest rate contract derivatives are valued using

financial models which utilize observable inputs for similar instruments and

are classified as Level 2. Inputs include forward interest rate curves, notional

amounts, interest rates and credit quality of the counterparties.

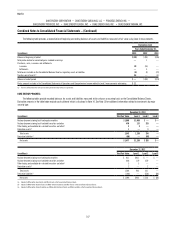

Goodwill and long-lived assets

See Note 11 for a discussion of the valuation of goodwill and long-lived

assets.