SunTrust 2014 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

54

executed, market information received from outside market

participants and analysts, and/or changes in the underlying

collateral performance.

We also gather third party broker quotes or use industry-

standard or proprietary models to estimate the fair value of these

instruments particularly when pricing service information or

observable market trades are not available. In most cases, the

current market conditions cause the broker quotes to be

indicative and the price indications and broker quotes to be

supported by very limited to no recent market activity. In those

instances, we weighted the third party information according to

our judgment of it being a reasonable indication of the

instrument's fair value.

When fair values are estimated based on models, we

consider relevant market indices that correlate to the underlying

collateral, along with assumptions such as liquidity discounts,

interest rates, prepayment speeds, default rates, loss severity

rates, and discount rates. In markets with higher liquidity, we

have more pricing information from third parties and a reduction

in the need to use internal pricing models to estimate fair value.

Even when third party pricing is available, we continued to

classify certain assets as level 3 as we believe that this third party

pricing relied on significant unobservable assumptions, as

evidenced by a persistently wide bid-ask price range and

variability in pricing from the pricing services, particularly for

the vintages and exposures we hold.

As certain markets recover, we are able to reduce our

exposure to many of our level 3 instruments through sales,

maturities, or other distributions at prices approximating our

previous estimates, thereby corroborating the valuation

approaches used.

All of the techniques used and information obtained in the

valuation process provide a range of estimated values, which

were evaluated and compared in order to establish an estimated

value that, based on management's judgment, represented a

reasonable estimate of the instrument's fair value. It was not

uncommon for the range of value of these instruments to vary

widely; in such cases, we selected an estimated value that we

believed was the best indication of value based on the yield a

market participant in this current environment would expect. Due

to the continued illiquidity and credit risk of level 3 securities,

these market values are highly sensitive to assumption changes

and market volatility. Improvements may be made to our pricing

methodologies on an ongoing basis as observable and relevant

information becomes available to us.

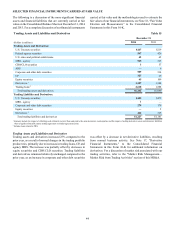

Most derivative instruments are level 1 or level 2

instruments, except for the IRLCs and the Visa litigation related

derivative, which are level 3 instruments. See Note 17,

“Derivative Financial Instruments,” to the Consolidated

Financial Statements in this Form 10-K for a detailed discussion

regarding derivative contracts and valuation.

At December 31, 2014, level 3 trading assets and derivatives

and level 3 securities AFS totaled $25 million and $946 million,

respectively. Our level 3 securities AFS portfolio included FHLB

and Federal Reserve Bank stock, as well as certain municipal

bond securities, some of which are only redeemable with the

issuer at par and cannot be traded in the market; as such, no

significant observable market data for these instruments is

available. These nonmarketable securities AFS totaled

approximately $797 million at December 31, 2014. The

remaining level 3 securities, both trading assets and securities

AFS, are predominantly private ABS and MBS, including

interests retained from Company-sponsored securitizations or

purchased from third party securitizations. For all level 3

securities, little or no market activity exists for either the security

or the underlying collateral and therefore, the significant

assumptions used to value the securities are not market

observable.

Level 3 trading assets and derivatives decreased by $47

million, or 65%, during the year ended December 31, 2014,

primarily due to sales of securities. Level 3 securities AFS

decreased by $7 million, or 1%, during the year ended

December 31, 2014 due to continued paydowns and sales

partially offset by purchases. During the year ended

December 31, 2014, we recognized $264 million in net gains

through earnings related to trading and derivative assets and

liabilities classified as level 3, primarily due to $252 million in

IRLC related gains and $12 million in net gains from trading

securities.

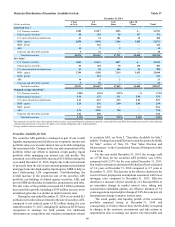

Loans

The fair values of LHFI and LHFS are based on observable

current market prices in the secondary loan market in which loans

trade, as either whole loans or as ABS. When security prices are

obtained in the secondary loan market, we will translate these

prices into whole loan prices by incorporating adjustments for

estimated credit enhancement costs, loan servicing fees, and

various other transformation costs, when material. The fair value

of a loan is impacted by the nature of the asset and the market

liquidity. Level 3 loans are predominantly mortgage loans that

have been deemed not marketable, largely due to borrower

defaults or the identification of other loan defects. When

estimating fair value for these loans, we use a discounted cash

flow approach based on assumptions that are generally not

observable in the current markets, such as prepayment speeds,

default rates, loss severity rates, and liquidity discounts. Absent

comparable current market data, we believe that the fair value

derived from these various approaches is a reasonable

approximation of the prices that we would receive upon sale of

the loans.

Other Intangible Assets and Other Assets

We record all MSRs at fair value on a recurring basis. The fair

value of MSRs is based on discounted cash flow analyses and

can be highly variable quarter to quarter as market conditions

and projected interest rates change. We provide disclosure of the

key economic assumptions used to measure MSRs and residual

interests and a sensitivity analysis to adverse changes to these

assumptions in Note 9, “Goodwill and Other Intangible Assets,”

to the Consolidated Financial Statements in this Form 10-K. This

sensitivity analysis does not take into account hedging activities

discussed in the “Other Market Risk” section of this MD&A.

The fair values of OREO and other repossessed assets are

measured on a non-recurring basis and are typically determined

based on recent appraisals by third parties and other market

information. Our OREO properties are concentrated in Georgia,

Florida, and North Carolina. Further deterioration in property

values in those states or changes to our disposition strategies

could cause our estimates of OREO values to decline which

would result in further write-downs.