SunTrust 2014 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

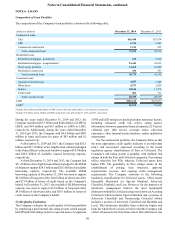

Notes to Consolidated Financial Statements, continued

88

of internal and external influences on credit quality that are not

fully reflected in the historical loss or other risk rating data. These

influences may include elements such as changes in credit

underwriting, concentration risk, macroeconomic conditions,

and/or recent observable asset quality trends.

The Company’s charge-off policy meets regulatory

minimums. Commercial loans are charged off when they are

considered uncollectible. Losses on unsecured consumer loans

are generally recognized at 120 days past due, except for losses

on guaranteed student loans which are recognized at 270 days

past due. However, if the borrower is in bankruptcy, the loan is

charged-off in the month the loan becomes 60 days past due.

Losses, as appropriate, on secured consumer loans, including

residential real estate, are typically recognized at 120 or 180 days

past due, depending on the loan and collateral type, in compliance

with the FFIEC guidelines. However, if the borrower is in

bankruptcy, the secured asset is evaluated once the loan becomes

60 days past due. The loan value in excess of the secured asset

value is written down or charged-off after the valuation occurs.

Additionally, if a residential loan is discharged in Chapter 7

bankruptcy and not reaffirmed by the borrower, the Company's

policy is to immediately charge-off the excess of the carrying

amount over the fair value of the collateral.

The Company uses numerous sources of information when

evaluating a property’s value. Estimated collateral valuations are

based on appraisals, broker price opinions, recent sales of

foreclosed properties, automated valuation models, other

property-specific information, and relevant market information,

supplemented by the Company’s internal property valuation

analysis. The value estimate is based on an orderly disposition

inclusive of marketing costs. In limited instances, the Company

adjusts externally provided appraisals for justifiable and well-

supported reasons, such as an appraiser not being aware of certain

property-specific factors or recent sales information. Appraisals

generally represent the “as is” value of the property but may be

adjusted based on the intended disposition strategy of the

property.

For commercial and CRE loans secured by property, an

acceptable third party appraisal or other form of evaluation, as

permitted by regulation, is obtained prior to the origination of

the loan and upon a subsequent transaction involving a material

change in terms. In addition, updated valuations may be obtained

during the life of a transaction, as appropriate, such as when a

loan's performance materially deteriorates. In situations where

an updated appraisal has not been received or a formal evaluation

performed, the Company monitors factors that can positively or

negatively impact property value, such as the date of the last

valuation, the volatility of property values in specific markets,

changes in the value of similar properties, and changes in the

characteristics of individual properties. Changes in collateral

value affect the ALLL through the risk rating or impaired loan

evaluation process. Charge-offs are recognized when the amount

of the loss is quantifiable and timing is known. The charge-off

is measured based on the difference between the loan’s carrying

value, including deferred fees, and the estimated realizable value

of the loan, net of estimated selling costs. When valuing a

property for the purpose of determining a charge-off, a third party

appraisal or an independently derived internal evaluation is

generally employed.

For mortgage loans secured by residential property where

the Company is proceeding with a foreclosure action, a new

valuation is obtained prior to the loan becoming 180 days past

due and, if required, the loan is written down to its realizable

value, net of estimated selling costs. In the event the Company

decides not to proceed with a foreclosure action, the full balance

of the loan is charged-off. If a loan remains in the foreclosure

process for 12 months past the original charge-off, the Company

obtains a new valuation annually. Any additional loss based on

the new valuation is charged-off. At foreclosure, a new valuation

is obtained and the loan is transferred to OREO at the new

valuation less estimated selling costs; any loan balance in excess

of the transfer value is charged-off. Estimated declines in value

of the residential collateral between these formal evaluation

events are captured in the ALLL based on changes in the house

price index in the applicable MSA or other market information.

In addition to the ALLL, the Company also estimates

probable losses related to unfunded lending commitments, such

as letters of credit and binding unfunded loan commitments.

Unfunded lending commitments are analyzed and segregated by

risk similar to funded loans based on the Company’s internal risk

rating scale. These risk classifications, in combination with

probability of commitment usage, existing economic conditions,

and any other pertinent information, result in the estimation of

the reserve for unfunded lending commitments. The reserve for

unfunded lending commitments is reported on the Consolidated

Balance Sheets in other liabilities and the provision associated

with changes in the unfunded lending commitment reserve is

reported in the Consolidated Statements of Income in provision

for credit losses. For additional information on the Company's

allowance for credit loss activities, see Note 7, “Allowance for

Credit Losses.”

Premises and Equipment

Premises and equipment are carried at cost less accumulated

depreciation and amortization. Depreciation is calculated

predominantly using the straight-line method over the assets’

estimated useful lives. Leasehold improvements are amortized

using the straight-line method over the shorter of the

improvements' estimated useful lives or the lease term.

Construction and software in process includes costs related to

in-process branch expansion, branch renovation, and software

development projects. Upon completion, branch and office

related projects are maintained in premises and equipment while

completed software projects are reclassified to other assets in the

Consolidated Balance Sheets. Maintenance and repairs are

charged to expense, and improvements that extend the useful life

of an asset are capitalized and depreciated over the remaining

useful life. Premises and equipment are evaluated for impairment

whenever events or changes in circumstances indicate that the

carrying value of the asset may not be recoverable. For additional

information on the Company’s premises and equipment

activities, see Note 8, “Premises and Equipment.”

Goodwill and Other Intangible Assets

Goodwill represents the excess purchase price over the fair value

of identifiable net assets of acquired companies. Goodwill is

assigned to reporting units, which are operating segments or one

level below an operating segment, as of the acquisition date.

Goodwill is assigned to the Company’s reporting units that are