SunTrust 2014 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

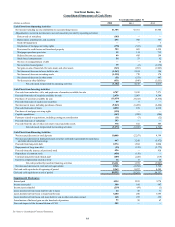

Notes to Consolidated Financial Statements, continued

86

amortized cost basis, the debt security is written down to fair

value, and the full amount of any impairment charge is

recognized as a component of noninterest income in the

Consolidated Statements of Income. If the Company does not

intend to sell the debt security and it is more-likely-than-not that

the Company will not be required to sell the debt security prior

to recovery of its amortized cost basis, only the credit component

of any impairment of a debt security is recognized as a component

of noninterest income in the Consolidated Statements of Income,

with the remaining impairment recorded in OCI.

The OTTI review for marketable equity securities includes

an analysis of the facts and circumstances of each individual

investment and focuses on the severity of loss, the length of time

the fair value has been below cost, the expectation for that

security's performance, the financial condition and near-term

prospects of the issuer, and management's intent and ability to

hold the security to recovery. A decline in value of an equity

security that is considered to be other-than-temporary is

recognized as a component of noninterest income in the

Consolidated Statements of Income.

Nonmarketable equity securities are accounted for under the

cost or equity method and are included in other assets in the

Consolidated Balance Sheets. The Company reviews

nonmarketable securities accounted for under the cost method

on a quarterly basis, and reduces the asset value when declines

in value are considered to be other-than-temporary. Equity

method investments are recorded at cost, adjusted to reflect the

Company’s portion of income, loss, or dividends of the investee.

Realized income, realized losses, and estimated other-than-

temporary unrealized losses on cost and equity method

investments are recognized in noninterest income in the

Consolidated Statements of Income.

For additional information on the Company’s securities

activities, see Note 4, “Trading Assets and Liabilities and

Derivatives,” and Note 5, “Securities Available for Sale.”

Loans Held for Sale

The Company’s LHFS generally includes certain residential

mortgage loans, commercial loans, consumer indirect loans and

student loans. Loans are initially classified as LHFS when they

are identified as being available for immediate sale and a formal

plan exists to sell them. LHFS are recorded at either fair value,

if elected, or the lower of cost or fair value on an individual loan

basis. Origination fees and costs for LHFS recorded at LOCOM

are capitalized in the basis of the loan and are included in the

calculation of realized gains and losses upon sale. Origination

fees and costs are recognized in earnings at the time of origination

for LHFS that are elected to be measured at fair value. Fair value

is derived from observable current market prices, when

available, and includes loan servicing value. When observable

market prices are not available, the Company uses judgment and

estimates fair value using internal models, in which the Company

uses its best estimates of assumptions it believes would be used

by market participants in estimating fair value. Adjustments to

reflect unrealized gains and losses resulting from changes in fair

value and realized gains and losses upon ultimate sale of the

loans are classified as noninterest income in the Consolidated

Statements of Income.

The Company may transfer certain residential mortgage

loans, commercial loans, student loans, and consumer indirect

loans to a held for sale classification at LOCOM. At the time of

transfer, any credit losses subject to charge-off in accordance

with the Company's policy are recorded as a reduction in the

ALLL. Any further or subsequent losses, including those related

to interest rate or liquidity related valuation adjustments, are

recorded as a component of noninterest income in the

Consolidated Statements of Income. The Company may also

transfer loans from held for sale to held for investment. At the

time of transfer, any difference between the carrying amount of

the loan and its outstanding principal balance is recognized as

an adjustment to yield using the effective yield method, unless

the loan was elected upon origination to be accounted for at fair

value. If a held for sale loan for which fair value accounting was

elected is transferred to held for investment, it will continue to

be accounted for at fair value in the held for investment portfolio.

For additional information on the Company’s LHFS activities,

see Note 6, “Loans.”

Loans

Loans that management has the intent and ability to hold for the

foreseeable future or until maturity or pay-off are considered

LHFI. The Company’s loan balance is comprised of loans held

in portfolio, including commercial loans, consumer loans, and

residential loans. Interest income on all types of loans, except

those classified as nonaccrual, is accrued based upon the

outstanding principal amounts using the effective yield method.

Commercial loans (C&I, CRE, and commercial

construction) are considered to be past due when payment is not

received from the borrower by the contractually specified due

date. The Company typically classifies commercial loans as

nonaccrual when one of the following events occurs: (i) interest

or principal has been past due 90 days or more, unless the loan

is both well secured and in the process of collection; (ii)

collection of recorded interest or principal is not anticipated; or

(iii) income for the loan is recognized on a cash basis due to the

deterioration in the financial condition of the debtor. When a loan

is placed on nonaccrual, accrued interest is reversed against

interest income. Interest income on nonaccrual loans, if

recognized, is recognized after the principal has been reduced to

zero. If and when commercial borrowers demonstrate the ability

to repay a loan classified as nonaccrual in accordance with its

contractual terms, the loan may be returned to accrual status upon

meeting all regulatory, accounting, and internal policy

requirements.

Consumer loans (guaranteed and private student loans, other

direct, indirect, and credit card) are considered to be past due

when payment is not received from the borrower by the

contractually specified due date. Guaranteed student loans

continue to accrue interest regardless of delinquency status

because collection of principal and interest is reasonably assured.

Other direct and indirect loans are typically placed on nonaccrual

when payments have been past due for 90 days or more except

when the borrower has declared bankruptcy, in which case, they

are moved to nonaccrual status once they become 60 days past

due. When a loan is placed on nonaccrual, accrued interest is

reversed against interest income. Interest income on nonaccrual

loans, if recognized, is recognized on a cash basis. Nonaccrual

consumer loans are typically returned to accrual status once they

are no longer past due.