SunTrust 2014 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

Notes to Consolidated Financial Statements, continued

148

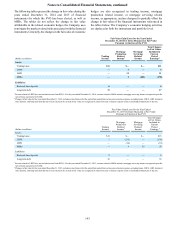

Long-term debt

The Company has elected to measure at fair value certain fixed

rate debt issuances of public debt which are valued by obtaining

quotes from a third party pricing service and utilizing broker

quotes to corroborate the reasonableness of those marks.

Additionally, information from market data of recent observable

trades and indications from buy side investors, if available, are

taken into consideration as additional support for the value. Due

to the availability of this information, the Company determined

that the appropriate classification for the debt is level 2. The

election to fair value the debt was made to align the accounting

for the debt with the accounting for the derivatives without

having to account for the debt under hedge accounting, thus

avoiding the complex and time consuming fair value hedge

accounting requirements.

The Company’s public debt carried at fair value impacts

earnings predominantly through changes in the Company’s

credit spreads as the Company has entered into derivative

financial instruments that economically convert the interest rate

on the debt from a fixed to a floating rate. The estimated earnings

impact from changes in credit spreads above U.S. Treasury rates

were losses of $19 million and gains of $40 million and $78

million for the years ended December 31, 2014, 2013, and 2012,

respectively.

At December 31, 2014, the Company did not measure any

issued securities of a CLO at fair value. Previously, the Company

classified these types of securities as level 2, as the primary

driver of their fair values were the loans owned by the CLO,

which the Company also elected to measure at fair value prior

to the deconsolidation of the CLO, as discussed herein under

“Loans Held for Sale and Loans Held for Investment–Corporate

and other LHFS.”

Other liabilities

The Company’s other liabilities that are carried at fair value on

a recurring basis include contingent consideration obligations

related to acquisitions. Contingent consideration associated

with acquisitions is adjusted to fair value until settled. As the

assumptions used to measure fair value are based on internal

metrics that are not market observable, the earn-out is

considered a level 3 liability. Additionally, the derivative that

the Company obtained as a result of its sale of Visa Class B

shares was included in other liabilities at December 31, 2013.

This derivative was included in derivative contracts at

December 31, 2014 and accordingly, reclassified to derivative

contracts in the prior year level 3 assumptions and reconciliation

below for comparability.

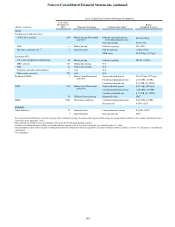

The valuation technique and range, including weighted

average, of the unobservable inputs associated with the

Company's level 3 assets and liabilities are as follows:

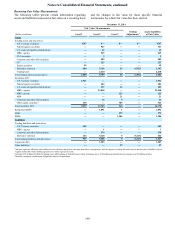

Level 3 Significant Unobservable Input Assumptions

(Dollars in millions)

Fair value

December 31,

2014 Valuation Technique Unobservable Input 1Range

(weighted average)

Assets

Trading assets and derivatives:

Derivative contracts, net 2$20 Internal model Pull through rate 40-100% (75%)

MSR value 39-218 bps (107 bps)

Securities AFS:

U.S. states and political subdivisions 12 Cost N/A

MBS - private 123 Third party pricing N/A

ABS 21 Third party pricing N/A

Corporate and other debt securities 5 Cost N/A

Other equity securities 785 Cost N/A

Residential LHFS 1 Monte Carlo/Discounted

cash flow Option adjusted spread 145-225 (157 bps)

Conditional prepayment rate 1-30 CPR (15 CPR)

Conditional default rate 0-3 CDR (0.75 CDR)

LHFI 269 Monte Carlo/Discounted

cash flow Option adjusted spread 0-450 (286 bps)

Conditional prepayment rate 4-30 CPR (13.75 CPR)

Conditional default rate 0-7 CDR (1.75 CDR)

3 Collateral based pricing Appraised value NM 4

MSRs 1,206 Monte Carlo/Discounted

cash flow Conditional prepayment rate 2-47 CPR (11 CPR)

Option adjusted spread (1.34%)-122.1% (9.96%)

Liabilities

Other liabilities 327 Internal model Loan production volume 0-150% (107%)

1 For certain assets and liabilities where the Company utilizes third party pricing, the unobservable inputs and their ranges are not reasonably available to the Company, and therefore, have

been noted as not applicable, "N/A."

2 Represents the net of IRLC assets and liabilities entered into by the Mortgage Banking segment and includes the derivative liability associated with the Company's sale of Visa shares.

3 Input assumptions relate to the Company's contingent consideration obligations related to acquisitions. See Note 16, "Guarantees," for additional information.

4 Not meaningful.