SunTrust 2014 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

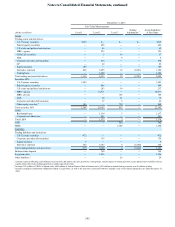

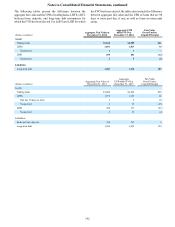

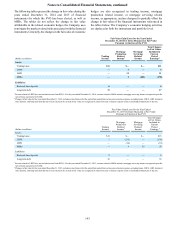

Notes to Consolidated Financial Statements, continued

138

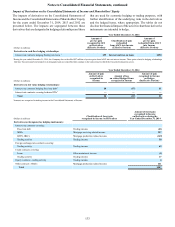

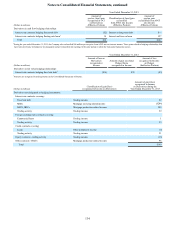

are expected to be reclassified to net interest income over the

next twelve months in connection with the recognition of interest

income on these hedged items. The amount to be reclassified

into income includes both active and terminated or de-designated

cash flow hedges. The Company may choose to terminate or de-

designate a hedging relationship in this program due to a change

in the risk management objective for that specific hedge item,

which may arise in conjunction with an overall balance sheet

management strategy.

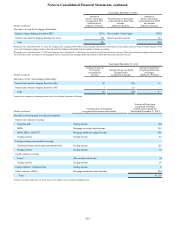

During 2008, the Company executed zero-cost equity

collars on 60 million common shares of The Coca-Cola

Company pursuant to the Agreements, which were to be

derivatives in their entirety. The Company designated the collars

as cash flow hedges of the Company's probable forecasted sales

of The Coca-Cola Company common shares. The risk

management objective was to hedge the cash flows on the

forecasted sales of The Coca-Cola Company common shares at

market values equal to or above the call strike price and equal

to or below the put strike price. The Company assessed hedge

effectiveness on a quarterly basis and measured hedge

ineffectiveness with the effective portion of the changes in fair

value of the Agreements recognized in AOCI and any ineffective

portions recognized in trading income.

During 2012, the Company and The Coca-Cola Company

Counterparty accelerated the termination of the Agreements, and

the Company sold in the market or to The Coca-Cola Company

Counterparty 59 million of its 60 million shares of The Coca-

Cola Company and contributed the remaining 1 million shares

to the SunTrust Foundation for a net gain of $1.9 billion, which

is net of a $305 million loss related to the derivative contract

termination of the Agreements. Upon approval by the Board to

terminate the Agreements and sell and donate The Coca-Cola

Company shares, the Agreements no longer qualified as cash

flow hedges. Thus, subsequent changes in value of the

Agreements, totaling $60 million, were recognized in net

securities (losses)/gains in the Consolidated Statements of

Income. Amounts recognized in AOCI in the Consolidated

Statements of Shareholders' Equity during the period the

Agreements qualified as cash flow hedges totaled $365 million

in losses. These amounts remained in AOCI until the sale of The

Coca-Cola Company shares, at which time the amounts were

reclassified to net securities (losses)/gains in the Consolidated

Statements of Income. See additional discussion regarding The

Coca-Cola Company Agreements in the "Securities Available for

Sale" sections of MD&A in this Form 10-K.

Fair Value Hedges

The Company enters into interest rate swap agreements as part

of the Company’s risk management objectives for hedging its

exposure to changes in fair value due to changes in interest rates.

These hedging arrangements convert Company-issued fixed rate

long-term debt to floating rates. Consistent with this objective,

the Company reflects the accrued contractual interest on the

hedged item and the related swaps as part of current period

interest. There were no components of derivative gains or losses

excluded in the Company’s assessment of hedge effectiveness

related to the fair value hedges.

Economic Hedging and Trading Activities

In addition to designated hedging relationships, the Company

also enters into derivatives as an end user to economically hedge

risks associated with certain non-derivative and derivative

instruments, along with entering into derivatives in a trading

capacity with its clients.

The primary risks that the Company economically hedges

are interest rate risk, foreign exchange risk, and credit risk.

Economic hedging objectives are accomplished by entering into

offsetting derivatives either on an individual basis or collectively

on a macro basis and generally accomplish the Company’s goal

of mitigating the targeted risk. To the extent that specific

derivatives are associated with specific hedged items, the

notional amounts, fair values, and gains/(losses) on the

derivatives are illustrated in the tables in this footnote.

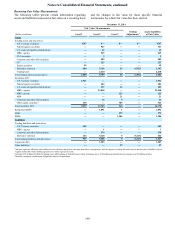

• The Company utilizes interest rate derivatives to mitigate

exposures from various instruments.

The Company is subject to interest rate risk on its fixed

rate debt. As market interest rates move, the fair value of

the Company’s debt is affected. To protect against this

risk on certain debt issuances that the Company has

elected to carry at fair value, the Company has entered

into pay variable-receive fixed interest rate swaps that

decrease in value in a rising rate environment and increase

in value in a declining rate environment.

The Company is exposed to risk on the returns of certain

of its brokered deposits that are carried at fair value. To

hedge against this risk, the Company has entered into

interest rate derivatives that mirror the risk profile of the

returns on these instruments.

The Company is exposed to interest rate risk associated

with MSRs, which the Company hedges with a

combination of mortgage and interest rate derivatives,

including forward and option contracts, futures, and

forward rate agreements.

The Company enters into mortgage and interest rate

derivatives, including forward contracts, futures, and

option contracts to mitigate interest rate risk associated

with IRLCs and mortgage LHFS.

• The Company is exposed to foreign exchange rate risk

associated with certain commercial loans.

• The Company enters into CDS to hedge credit risk associated

with certain loans held within its Wholesale Banking segment.

The Company accounts for these contracts as derivatives and,

accordingly, recognizes these contracts at fair value, with

changes in fair value recognized in other noninterest income

in the Consolidated Statements of Income.

• Trading activity, as illustrated in the tables within this footnote,

primarily includes interest rate swaps, equity derivatives,

CDS, futures, options, foreign currency contracts, and

commodities. These derivatives are entered into in a dealer

capacity to facilitate client transactions or are utilized as a risk

management tool by the Company as an end user in certain

macro-hedging strategies. The macro-hedging strategies are

focused on managing the Company’s overall interest rate risk

exposure that is not otherwise hedged by derivatives or in

connection with specific hedges and, therefore, the Company

does not specifically associate individual derivatives with

specific assets or liabilities.