SunTrust 2014 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

Notes to Consolidated Financial Statements, continued

127

will be incurred and the amount of such loss can be reasonably

estimated, the Company records those reserves in other liabilities

in the Consolidated Balance Sheets. See Note 19,

"Contingencies," for additional information on current legal

matters related to representations and warranties.

Loans sold to Ginnie Mae are insured by either the FHA or

VA. As servicer, the Company may elect to repurchase delinquent

loans in accordance with Ginnie Mae guidelines; however, the

loans continue to be insured. The Company indemnifies the FHA

and VA for losses related to loans not originated in accordance

with their guidelines. See Note 19, "Contingencies," for

additional information on current legal matters related to

representations and warranties made in connection with loan

sales and the final settlement of HUD's investigation of the

Company's origination practices for FHA loans.

During the third quarter of 2013, the Company reached

agreements in principle with Freddie Mac and Fannie Mae

relieving the Company of certain existing and future repurchase

obligations related to 2000-2008 vintages for Freddie Mac and

2000-2012 vintages for Fannie Mae. Repurchase requests have

declined significantly in 2014 as a result of the settlements.

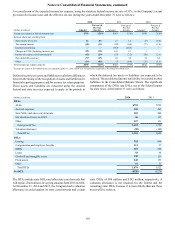

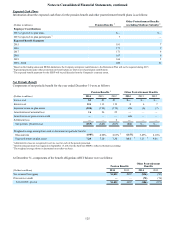

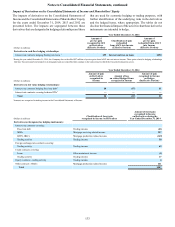

Repurchase requests from GSEs, Ginnie Mae, and non-agency

investors, for all vintages, are illustrated in the following table

that summarizes demand activity for the years ended December

31:

(Dollars in millions) 2014 2013 2012

Beginning pending repurchase

requests $126 $655 $590

Repurchase requests received 158 1,511 1,726

Repurchase requests resolved:

Repurchased (28) (1,134) (769)

Cured (209) (906) (892)

Total resolved (237) (2,040) (1,661)

Ending pending repurchase

requests1$47 $126 $655

Percent from non-agency investors:

Pending repurchase requests 6.7% 2.8% 2.5%

Repurchase requests received 0.9 1.2 1.2

1 Comprised of $44 million, $122 million, and $639 million from the GSEs, and

$3 million, $4 million, and $16 million from non-agency investors at

December 31, 2014, 2013, and 2012, respectively.

The majority of these requests were from the GSEs, with a

limited number of requests from non-agency investors. The

repurchase and make whole requests received have been

primarily due to alleged material breaches of representations

related to compliance with the applicable underwriting

standards, including borrower misrepresentation and appraisal

issues. STM performs a loan-by-loan review of all requests and

contests demands to the extent they are not considered valid.

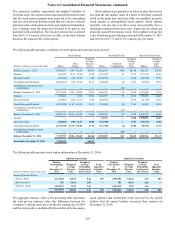

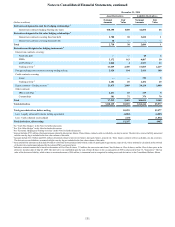

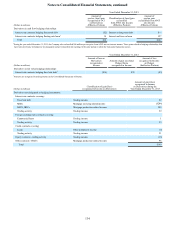

The following table summarizes the changes in the

Company’s reserve for mortgage loan repurchases:

Year Ended December 31

(Dollars in millions) 2014 2013 2012

Balance at beginning of period $78 $632 $320

Repurchase provision 12 114 713

Charge-offs, net of recoveries (5) (668) (401)

Balance at end of period $85 $78 $632

A significant degree of judgment is used to estimate the

mortgage repurchase liability as the estimation process is

inherently uncertain and subject to imprecision. The Company

believes that its reserve appropriately estimates incurred losses

based on its current analysis and assumptions, inclusive of the

Freddie Mac and Fannie Mae settlement agreements, GSE

owned loans serviced by third party servicers, loans sold to

private investors, and future indemnifications. However, the

2013 agreements with Freddie Mac and Fannie Mae settling

certain aspects of the Company's repurchase obligations preserve

their right to require repurchases arising from certain types of

events, and that preservation of rights can impact future losses

of the Company. While the repurchase reserve includes the

estimated cost of settling claims related to required repurchases,

the Company's estimate of losses depends on its assumptions

regarding GSE and other counterparty behavior, loan

performance, home prices, and other factors. The liability is

recorded in other liabilities in the Consolidated Balance Sheets,

and the related repurchase provision is recognized as a contra-

revenue item in mortgage production related income in the

Consolidated Statements of Income.

At December 31, 2014, the carrying value of outstanding

repurchased mortgage loans, net of any allowance for loan losses,

was $312 million, comprised of $300 million LHFI and $12

million LHFS, respectively, of which $29 million LHFI and $12

million LHFS, were nonperforming. At December 31, 2013, the

carrying value of outstanding repurchased mortgage loans, net

of any allowance for loan losses, was $339 million, comprised

of $325 million LHFI and $14 million LHFS, respectively, of

which $54 million LHFI and $14 million LHFS, were

nonperforming.

In addition to representations and warranties related to loan

sales, the Company makes representations and warranties that it

will service the loans in accordance with investor servicing

guidelines and standards, which may include (i) collection and

remittance of principal and interest, (ii) administration of escrow

for taxes and insurance, (iii) advancing principal, interest, taxes,

insurance, and collection expenses on delinquent accounts, (iv)

loss mitigation strategies including loan modifications, and (v)

foreclosures.

The Company normally retains servicing rights when loans

are transferred; however, servicing rights are occasionally sold

to third parties. When MSRs are sold, the Company makes

representations and warranties related to servicing standards and

obligations and recognizes a liability for contingent losses,

separate from the reserve for mortgage loan repurchases, which

totaled $25 million and $21 million at December 31, 2014 and

2013, respectively.