SunTrust 2014 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

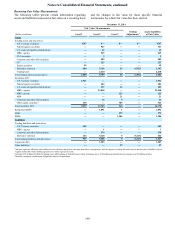

Notes to Consolidated Financial Statements, continued

147

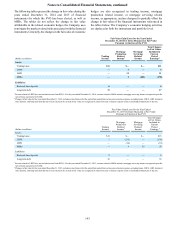

to borrower-specific credit risk were $12 million. In addition to

borrower-specific credit risk, there are other, more significant,

variables that drive changes in the fair values of the loans,

including interest rates and general conditions in the markets

for the loans.

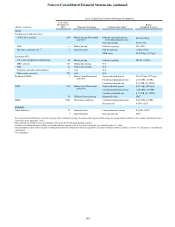

Corporate and other LHFS

As discussed in Note 10, “Certain Transfers of Financial Assets

and Variable Interest Entities,” the Company was previously the

primary beneficiary of a CLO entity, which resulted in the

Company consolidating the entity's underlying loans. During

the second quarter of 2014, in connection with the sale of

RidgeWorth, the Company determined it was no longer the

primary beneficiary of the CLO, and accordingly, the CLO was

deconsolidated. Prior to the second quarter of 2014, the

Company elected to measure the loans of the CLO at fair value

because the loans were periodically traded by the CLO. For the

years ended December 31, 2014 and 2013, the Company

recognized an immaterial amount of gains due to changes in fair

value attributable to borrower-specific credit risk in the

Consolidated Statements of Income. For the year ended

December 31, 2012, gains the Company recognized due to

changes in fair value attributable to borrower-specific credit risk

in the Consolidated Statements of Income were $10 million.

LHFI

Level 3 LHFI predominantly includes mortgage loans that are

deemed not marketable, largely due to the identification of loan

defects. The Company chooses to fair value these mortgage

LHFI to eliminate the complexities and inherent difficulties of

achieving hedge accounting and to better align reported results

with the underlying economic changes in value of the loans and

related hedge instruments. The Company values these loans

using a discounted cash flow approach based on assumptions

that are generally not observable in current markets, such as

prepayment speeds, default rates, loss severity rates, and

discount rates. These assumptions have an inverse relationship

to the overall fair value. Level 3 LHFI also includes mortgage

loans that are valued using collateral based pricing. Changes in

the applicable housing price index since the time of the loan

origination are considered and applied to the loan's collateral

value. An additional discount representing the return that a buyer

would require is also considered in the overall fair value.

Mortgage Servicing Rights

The Company records MSR assets at fair value. These values

are determined by projecting cash flows, which are then

discounted. The fair values of MSRs are impacted by a variety

of factors, including prepayment assumptions, spreads,

delinquency rates, contractually specified servicing fees,

servicing costs, and underlying portfolio characteristics. For

additional information, see Note 9, "Goodwill and Other

Intangible Assets." The underlying assumptions and estimated

values are corroborated by values received from independent

third parties based on their review of the servicing portfolio, and

comparisons to market transactions. Because these inputs are

not transparent in market trades, MSRs are classified as level 3

assets.

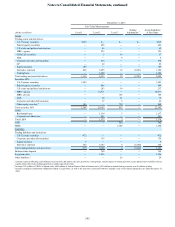

Liabilities

Trading liabilities and derivatives

Trading liabilities are primarily comprised of derivative

contracts, but also include various contracts involving U.S.

Treasury securities, equity securities, and corporate and other

debt securities that the Company uses in certain of its trading

businesses. The Company employs the same valuation

methodologies for these derivative contracts and securities as

are discussed within the corresponding sections herein under

“Trading Assets and Derivatives and Securities Available for

Sale.”

During the second quarter of 2009, in connection with its

sale of Visa Class B shares, the Company entered into a

derivative contract whereby the ultimate cash payments

received or paid, if any, under the contract are based on the

ultimate resolution of litigation involving Visa. The value of the

derivative was estimated based on the Company’s expectations

regarding the ultimate resolution of that litigation, which

involved a high degree of judgment and subjectivity.

Accordingly, the value of the derivative liability is classified as

a level 3 instrument. See Note 16, "Guarantees," for a discussion

of the valuation assumptions.

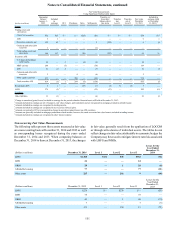

Brokered time deposits

The Company elected to measure certain CDs at fair value.

These debt instruments included embedded derivatives that

were generally based on underlying equity securities or equity

indices, but may have been based on other underlyings that may

or may not have been clearly and closely related to the host debt

instrument. The Company measured certain of these instruments

at fair value to better align the economics of the CDs with the

Company’s risk management strategies. The Company

evaluated, on an instrument specific basis, whether a new

issuance should be measured at fair value.

The Company classified these CDs as level 2 instruments

due to the Company’s ability to reasonably measure all

significant inputs based on observable market variables. The

Company employed a discounted cash flow approach to the host

debt component of the CD, based on observable market interest

rates for the term of the CD, and an estimate of the Bank’s credit

risk. For the embedded derivative features, the Company used

the same valuation methodologies as if the derivative were a

standalone derivative, as discussed herein under “Derivative

contracts.”

For brokered time deposits carried at fair value at December

31, 2013, the Company estimated credit spreads above LIBOR

based on credit spreads from actual or estimated trading levels

of the debt or other relevant market data. For the years ended

December 31, 2014 and 2013, the Company recognized an

immaterial amount of losses due to changes in its own credit

spread on its brokered time deposits carried at fair value. For

the year ended December 31, 2012, the Company recognized

$15 million of losses due to changes in its own credit spread on

its brokered time deposits carried at fair value. At December 31,

2014 the Company did not have any brokered time deposits

carried at fair value.