SunTrust 2014 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

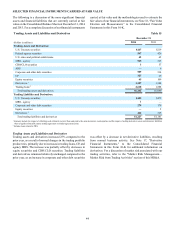

52

similarly to funded loans based on our internal risk rating scale.

These risk classifications, in combination with an analysis of

historical loss experience, probability of commitment usage, and

any other pertinent information, result in the estimation of the

reserve for unfunded lending commitments.

Our financial results are affected by the changes in the

Allowance for Credit Losses. This process involves our analysis

of complex internal and external variables, and it requires that

we exercise judgment to estimate an appropriate Allowance for

Credit Losses. As a result of the uncertainty associated with this

subjectivity, we cannot assure the precision of the amount

reserved should we experience sizeable loan or lease losses in

any particular period. For example, changes in the financial

condition of individual borrowers, economic conditions, or the

condition of various markets in which collateral may be sold

could require us to significantly decrease or increase the level of

the Allowance for Credit Losses. Such an adjustment could

materially affect net income as a result of the change in provision

for credit losses. For additional discussion of the ALLL see the

“Allowance for Credit Losses” and “Nonperforming Assets”

sections in this MD&A as well as Note 6, “Loans,” and Note 7,

“Allowance for Credit Losses,” to the Consolidated Financial

Statements in this Form 10-K.

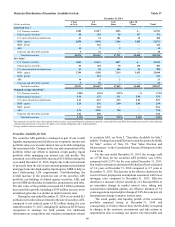

Mortgage Repurchase Reserve

We sell residential mortgage loans to investors through whole

loan sales in the normal course of our business. The investors

are primarily GSEs; however, $30 billion, or approximately

10%, of the population of total loans sold between January 1,

2005 and December 31, 2014 were sold to non-agency investors,

some in the form of securitizations. In association with these

transactions, we provide representations and warranties to the

third party investors that these loans meet certain requirements

as agreed to in investor guidelines. We have experienced

significantly fewer repurchase claims and losses related to loans

sold since 2009 as a result of stronger credit performance, more

stringent credit guidelines, and underwriting process

improvements.

During the third quarter of 2013, we reached agreements

with Freddie Mac and Fannie Mae under which they released us

from certain existing and future repurchase obligations for loans

funded by Freddie Mac between 2000 and 2008 and Fannie Mae

between 2000 and 2012.

Our current estimated liability for contingent losses related

to loans sold (i.e., our mortgage repurchase reserve) was $85

million at December 31, 2014. The liability is recorded in other

liabilities in the Consolidated Balance Sheets, and the related

repurchase provision is recognized in mortgage production

related income in the Consolidated Statements of Income. The

current reserves are deemed to be sufficient to cover probable

estimated losses related to exclusions due to certain defects (MI

related reasons, excessive seller contribution, ineligible property

and other charter violations) as outlined in the settlement

contract, GSE owned loans serviced by third party servicers,

loans sold to private investors, and future indemnifications.

Various factors could potentially impact the accuracy of the

assumptions underlying our mortgage repurchase reserve

estimate. As previously discussed, the level of repurchase

requests we receive is dependent upon the actions of third parties

and could differ from the assumptions that we have made.

Delinquency levels, delinquency roll rates, and our loss severity

assumptions are all highly dependent upon economic factors

including changes in real estate values and unemployment levels

which are, by nature, difficult to predict. Loss severity

assumptions could also be negatively impacted by delays in the

foreclosure process, which is a heightened risk in some of the

states where our loans sold were originated. Moreover, the 2013

agreements with Fannie Mae and Freddie Mac settling certain

aspects of our repurchase obligations preserve their right to

require repurchases arising from certain types of events, and that

preservation of rights can impact our future losses. While the

repurchase reserve includes the estimated cost of settling claims

related to required repurchases, our estimate of losses depends

on our assumptions regarding GSE and other counterparty

behavior, loan performance, home prices, and other factors.

While we have used the best information available in estimating

the mortgage repurchase reserve liability, these and other factors,

along with the discovery of additional information in the future

could result in changes in our assumptions which could

materially impact our results of operations.

See Note 16, “Guarantees” to the Consolidated Financial

Statements in this Form 10-K for further discussion.

Legal and Regulatory Matters

We are parties to numerous claims and lawsuits arising in the

course of our normal business activities, some of which involve

claims for substantial amounts, and the outcomes of which are

not within our complete control or may not be known for

prolonged periods of time. Management is required to assess the

probability of loss and amount of such loss, if any, in preparing

our financial statements.

We evaluate the likelihood of a potential loss from legal or

regulatory proceedings to which we are a party. We record a

liability for such claims only when a loss is considered probable

and the amount can be reasonably estimated. The liability is

recorded in other liabilities in the Consolidated Balance Sheets

and related expense is recorded in the applicable category of

noninterest expense, depending on the nature of the legal matter,

in the Consolidated Statements of Income. Significant judgment

may be required in the determination of both probability of loss

and whether an exposure is reasonably estimable. Our estimates

are subjective based on the status of the legal or regulatory

proceedings, the merits of our defenses, and consultation with

in-house and outside legal counsel. In many such proceedings,

it is not possible to determine whether a liability has been

incurred or to estimate the ultimate or minimum amount of that

liability until the matter is close to resolution. As additional

information becomes available, we reassess the potential liability

related to pending claims and may revise our estimates.

Due to the inherent uncertainties of the legal and regulatory

processes in the multiple jurisdictions in which we operate, our

estimates may be materially different than the actual outcomes,

which could have material effects on our business, financial

condition, and results of operations. See Note 19,

“Contingencies,” to the Consolidated Financial Statements in

this Form 10-K for further discussion.

Estimates of Fair Value

Fair value is the price that could be received to sell an asset or

paid to transfer a liability in an orderly transaction between