SunTrust 2014 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2014 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

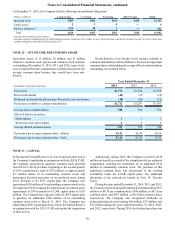

Notes to Consolidated Financial Statements, continued

105

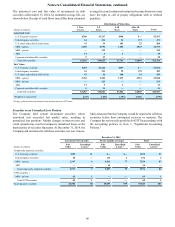

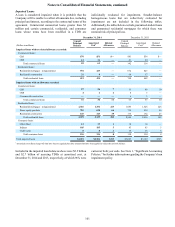

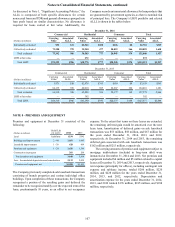

For the year ended December 31, 2014, the table below

represents defaults on loans that were first modified between

the periods January 1, 2013 and December 31, 2014 that

became 90 days or more delinquent or were charged-off during

the period.

Year Ended December 31, 2014

(Dollars in millions) Number of

Loans Amortized

Cost

Commercial loans:

C&I 78 $10

Residential loans:

Residential mortgages 158 19

Home equity products 101 5

Residential construction 6 —

Consumer loans:

Other direct 9 —

Indirect 181 1

Credit cards 145 1

Total TDRs 678 $36

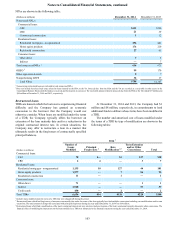

For the year ended December 31, 2013, the table below

represents defaults on loans that were first modified between

the periods January 1, 2012 and December 31, 2013 that

became 90 days or more delinquent or were charged-off during

the period.

Year Ended December 31, 2013

(Dollars in millions) Number of

Loans Amortized

Cost

Commercial loans:

C&I 55 $5

CRE 5 3

Commercial construction 1 —

Residential loans:

Residential mortgages 287 23

Home equity products 188 10

Residential construction 48 3

Consumer loans:

Other direct 15 1

Indirect 207 2

Credit cards 169 1

Total TDRs 975 $48

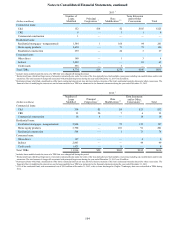

For the year ended December 31, 2012, the following table

represents defaults on loans that were first modified between

the periods January 1, 2011 and December 31, 2012 that

became 90 days or more delinquent or were charged-off during

the period.

Year Ended December 31, 2012

(Dollars in millions) Number of

Loans Amortized

Cost

Commercial loans:

C&I 84 $5

CRE 9 5

Commercial construction 10 7

Residential loans:

Residential mortgages 141 20

Home equity products 164 11

Residential construction 24 3

Consumer loans:

Other direct 4 —

Indirect 43 —

Credit cards 204 1

Total TDRs 683 $52

The majority of loans that were modified and subsequently

became 90 days or more delinquent have remained on

nonaccrual status since the time of modification.

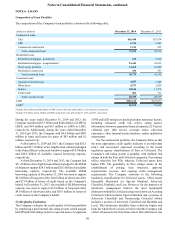

Concentrations of Credit Risk

The Company does not have a significant concentration of risk

to any individual client except for the U.S. government and its

agencies. However, a geographic concentration arises because

the Company operates primarily in the Southeastern and Mid-

Atlantic regions of the U.S. The Company engages in limited

international banking activities. The Company’s total cross-

border outstanding loans were $1.3 billion and $956 million at

December 31, 2014 and 2013, respectively.

The major concentrations of credit risk for the Company

arise by collateral type in relation to loans and credit

commitments. The only significant concentration that exists is

in loans secured by residential real estate. At December 31,

2014, the Company owned $38.8 billion in residential loans,

representing 29% of total LHFI, and had $10.9 billion in

commitments to extend credit on home equity lines and $3.3

billion in mortgage loan commitments. At December 31, 2013,

the Company owned $43.2 billion in residential loans,

representing 34% of total LHFI, and had $11.2 billion in

commitments to extend credit on home equity lines and $2.7

billion in mortgage loan commitments. Of the residential loans

owned at December 31, 2014 and December 31, 2013, 2% and

8%, respectively, were guaranteed by a federal agency or a GSE.

The following table presents loans in the residential

mortgage portfolio at December 31, which included terms such

as a high original LTV ratio (in excess of 80%), an interest only

feature, or a second lien position that may increase the

Company’s exposure to credit risk and result in a concentration

of credit risk. At December 31, 2014 and 2013, borrowers'

current weighted average FICO score on these loans was 754

and 732, respectively.