Sallie Mae 2008 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2008 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

As discussed above, in 2008, many lenders exited the FFELP marketplace, creating concerns about the

availability of federal loans for students served by this program. As a result, some schools began to decrease

their participation in the FFELP program in July 2008 for the stability of the FDLP. ED estimated that the

FDLP could double its market share.

The Higher Education Act (the “HEA”) regulates every aspect of the federally guaranteed student loan

program, including communications with borrowers, loan originations and default aversion. Failure to service a

student loan properly could jeopardize the guarantee on federal student loans. This guarantee generally covers

98 and 97 percent of the student loan’s principal and accrued interest for loans disbursed before and after

July 1, 2006, respectively. In the case of death, disability or bankruptcy of the borrower, the guarantee covers

100 percent of the loan’s principal and accrued interest.

FFELP loans are guaranteed by state agencies or non-profit companies designated as guarantors, with ED

providing reinsurance to the guarantor. Guarantors are responsible for performing certain functions necessary

to ensure the program’s soundness and accountability. These functions include reviewing loan application data

to detect and prevent fraud and abuse and to assist lenders in preventing default by providing counseling to

borrowers. Generally, the guarantor is responsible for ensuring that loans are serviced in compliance with the

requirements of the HEA. When a borrower defaults on a FFELP loan, we submit a claim to the guarantor

who provides reimbursements of principal and accrued interest subject to the Risk Sharing (See APPENDIX A,

“FEDERAL FAMILY EDUCATION LOAN PROGRAM,” to this document for a description of the role of

guarantors.)

Private Education Loan Products

In addition to federal loan programs, which have statutory limits on annual and total borrowing, we

sponsor a variety of Private Education Loan programs to bridge the gap between the cost of education and a

student’s resources. The majority of our Private Education Loans are made in conjunction with a FFELP

Stafford loan and are marketed to schools through the same marketing channels and by the same sales force as

FFELP loans. As a result of the credit market dislocation discussed above, a large number of lenders have

exited the Private Education Loan business and only a few of the country’s largest banks continue to offer the

product. Private Education Loans are discussed in more detail below.

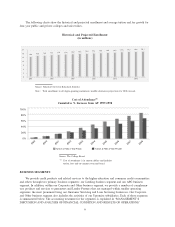

Drivers of Growth in the Student Loan Industry

Growth in our Managed student loan portfolio is driven by the growth in the overall market for student

loans, as well as by our own market share gains. Rising enrollment and college costs have resulted in the size

of the federally insured student loan market more than doubling over the last 10 years. Federally insured

student loan originations grew from $30.0 billion in FFY 1998 to $75.5 billion in FFY 2008.

According to the College Board, tuition and fees at four-year public institutions and four-year private

institutions have increased 50 percent and 27 percent, respectively, in constant, inflation-adjusted dollars, since

AY 1998-1999. Under the FFELP, there are limits to the amount students can borrow each academic year. The

first loan limit increases since 1992 were implemented July 1, 2007. In response to the credit crisis, Congress

significantly increased loan limits again in 2008. As a result, we anticipate that students will rely more on

federal loans to fund their tuition needs. Both federal and private loans as a percentage of total student aid

were 52 percent of total student aid in AY 1997-1998 and 53 percent in AY 2007-2008. Private Education

Loans accounted for 22 percent of total student loans — both federally guaranteed and Private Education

Loans — in AY 2007-2008, compared to 7 percent in AY 1997-1998.

The National Center for Education Statistics predicts that the college-age population will increase

approximately 10 percent from 2008 to 2017. Demand for education credit is expected to increase due to this

population demographic, first-time college enrollments of older students and continuing interest in adult

education.

5