Sallie Mae 2008 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2008 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

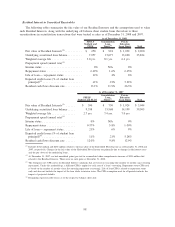

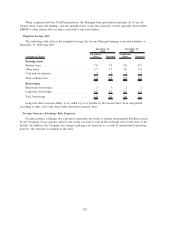

• Cost of funds assumptions related to the underlying auction rate securities bonds ($2.3 billion face

amount of bonds) within FFELP loan ($1.7 billion face amount of bonds) and Private Education Loan

($0.6 billion face amount of bonds) trusts were increased to take into account the expectations these

auction rate securities will continue to reset at higher rates for an extended period of time. This resulted

in a $116 million unrealized mark-to-market loss.

• The discount rate assumption related to the Private Education Loan and FFELP Residual Interests was

increased. The Company assessed the appropriateness of the current risk premium, which is added to

the risk free rate for the purpose of arriving at a discount rate, in light of the current economic and

credit uncertainty that exists in the market as of December 31, 2008. This discount rate is applied to

the projected cash flows to arrive at a fair value representative of the current economic conditions. The

Company increased the risk premium by 1,550 basis points and 390 basis points for Private Education

and FFELP, respectively, to take into account the current level of cash flow uncertainty and lack of

liquidity that exists with the Residual Interests. This resulted in a $904 million unrealized mark-to-mar-

ket loss.

The Company recorded net unrealized mark-to-market losses related to the Residual Interests of

$425 million during the year ended December 31, 2008. The mark-to-market losses were primarily related to

the increase in the discount rate assumptions discussed above which resulted in a $904 million mark-to-market

loss. This was partially offset by an unrealized mark-to-market gain of $555 million related to the Floor

Income component of the Residual Interest primarily due to the significant decrease in interest rates from

December 31, 2007 to December 31, 2008.

The Company recorded impairments to the Retained Interests of $254 million and $157 million,

respectively, for the years ended December 31, 2007 and 2006. The impairment charges were the result of

FFELP loans prepaying faster than projected through loan consolidations ($110 million and $104 million for

the years ended December 31, 2007 and 2006, respectively), impairment to the Floor Income component of

the Company’s Retained Interest due to increases in interest rates during the period ($24 million and

$53 million for the years ended December 31, 2007 and 2006, respectively), and increases in prepayments,

defaults, and the discount rate related to Private Education Loans ($120 million for the year ended

December 31, 2007). In addition, the Company recorded an unrealized mark-to-market loss under SFAS No. 155

of $25 million for the year ended December 31, 2007.

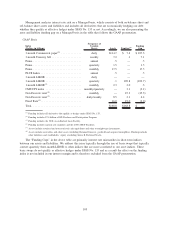

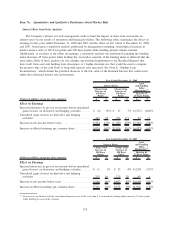

CONTRACTUAL CASH OBLIGATIONS

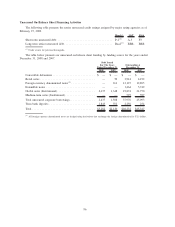

The following table provides a summary of our obligations associated with long-term notes at

December 31, 2008. For further discussion of these obligations, see Note 7, “Borrowings,” to the consolidated

financial statements. The Company has no outstanding equity forward positions outstanding after the contract

settlement on January 9, 2008. See Note 11, “Stockholders’ Equity,” to the consolidated financial statements.

1 Year

or Less

2to3

Years

4to5

Years

Over

5 Years Total

Long-term notes:

Unsecured borrowings ................. $ — $14,184 $ 5,324 $11,674 $ 31,182

Term bank deposits ................... — 727 381 — 1,108

Secured borrowings

(1)

................. 6,722 14,390 13,262 48,199 82,573

Total contractual cash obligations

(2)

....... $6,722 $29,301 $18,967 $59,873 $114,863

(1)

Includes Financial Interpretation (“FIN”) No. 46(R) long-term beneficial interests of $80.6 billion of notes issued by consolidated

variable interest entities in conjunction with our on-balance sheet securitization transactions and included in long-term notes in

the consolidated balance sheet. Timing of obligations is estimated based on the Company’s current projection of prepayment

speeds of the securitized assets.

(2)

Only includes principal obligations and specifically excludes SFAS No. 133 derivative market value adjustments of $3.4 billion

for long-term notes. Interest obligations on notes is predominantly variable in nature, resetting quarterly based on 3 month

LIBOR.

101