SunTrust 2008 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

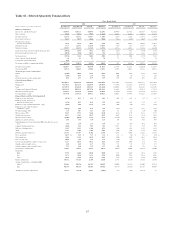

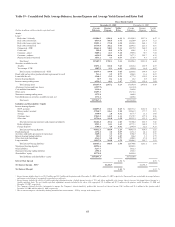

Total noninterest expense increased $60.2 million, or 2.3%, from the same period in 2007. The continuing positive impact of

expense savings initiatives and lower amortization of intangibles was offset by higher credit-related expenses including

operating losses due to fraud, other real estate, and collections, as well as continued investments in the branch distribution

network.

Wholesale

Wholesale’s net income for the twelve months ended December 31, 2008 was $217.3 million, an increase of $21.2 million,

or 10.8%, compared to the same period in 2007. Lower market valuation trading losses in structured products and affordable

housing related noninterest expenses were partially offset by an increase in provision expense, lower merchant banking

gains, and higher incentive-based compensation.

Net interest income was $564.7 million for the twelve months ended December 31, 2008, relatively unchanged from prior

year. Average loan balances increased $4.8 billion, or 16.2%, while the corresponding net interest income declined $7.1

million, or 1.6%. The migration of middle market clients from Retail and Commercial to Wholesale accounted for

approximately $1.8 billion of the increase in average loan balances and increased net interest income $25.8 million. The

remainder of Wholesale’s average loans increased $3.0 billion, or 10.4%, driven by increased corporate banking loans and

lease financing, which was partially offset by reductions in the residential builder portfolio. The corresponding net interest

income declined $32.9 million, or 7.3%, due to a shift in mix away from higher spread residential construction loans to lower

spread commercial loans, as well as an increase in residential construction nonaccrual loans. Total average deposits increased

$3.5 billion, or 63.2%, primarily in higher cost interest-bearing deposits. Deposit-related net interest income decreased $8.9

million, or 6.6%, driven by the lower credit for funds on demand deposits partially offset by the increased volumes in higher

cost deposit products.

Provision for loan losses was $167.4 million, an increase of $120.5 million over the prior year, resulting from higher

residential builder related charge-offs as well as increased charge-offs on middle market clients partially offset by lower

charge-offs in corporate banking.

Noninterest income increased $168.2 million, or 35.0%, primarily due to lower market valuation trading losses in structured

products. In addition, increases in direct finance, loan syndications, credit-related fees, and fixed income sales and trading

were partially offset by a reduction in merchant banking gains and lower revenues in structured leasing, derivatives, and

Affordable Housing.

Noninterest expense increased $6.4 million, or 0.8%, primarily due to the transfer of the middle market business from Retail

and Commercial to Wholesale which accounted for approximately $24.9 million of the increase. The remainder of

Wholesale’s noninterest expense decreased $18.4 million, or 2.3%, primarily due to a decrease in write-downs related to

Affordable Housing properties offset in part by higher incentive-based compensation.

Mortgage

Mortgage reported a net loss for the twelve months ended December 31, 2008 of $561.8 million, compared to $5.4 million in

net income in 2007, a decrease of $567.2 million, principally due to higher credit-related costs.

Net interest income declined $67.0 million, or 12.8%. Average loans increased $0.5 billion, or 1.7%, while the resulting net

interest income declined $78.7 million. Nonaccrual loans accounted for $46.0 million of the net interest income decline as

average nonaccrual loans increased $1.1 billion. Accruing loans declined $0.5 billion, or 1.8%, while net interest income

decreased $32.7 million, or 8.5%. The decline in net interest income was influenced by a change in product mix as declines

in construction-perm and Alt-A balances were replaced with lower yielding prime first lien mortgages. Average mortgage

loans held for sale declined $5.5 billion; however, due to widening spreads, net interest income increased $25.4 million.

Average investment securities were up $0.8 billion while net interest income increased $21.5 million primarily due to

improved spreads. Average deposits increased $0.1 billion, or 4.8%, although net interest income on deposits and other

liabilities decreased $17.7 million primarily due to lower short-term interest rates.

Provision for loan losses increased $410.1 million to $491.3 million due to higher residential mortgage and residential

construction net charge-offs.

Total noninterest income increased $70.2 million, or 19.2%, due to reduced net valuation losses, increased production fee

income, and securities gains in excess of MSRs impairment, partially offset by higher repurchase reserves and lower gains

from the sale of MSRs. Total production income increased $83.2 million, or 85.5%, driven by reduced valuation losses

associated with secondary market loans and the recognition of loan origination fees resulting from our election to record

73