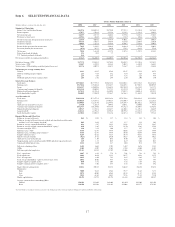

SunTrust 2008 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

In October 2008, the United States government established the EESA in response to instability in the financial markets. The

specific implications of the EESA include the authorization given to the Secretary of the Treasury to establish the Troubled

Asset Relief Program to purchase troubled assets from financial institutions. The definition of troubled assets is broad but

includes residential and commercial mortgages, as well as mortgage-related securities originated on or before March 14,

2008, if the Secretary determines the purchase promotes financial market stability. To date, the Treasury has not purchased

troubled assets under its authority to do so under the EESA.

Alternatively, the Treasury has focused on providing assistance through the associated Capital Purchase Program “(CPP”)

and Targeted Investment Program by purchasing preferred equity interests in the country’s largest financial institutions. In an

attempt to revitalize the struggling economy and inject necessary liquidity and capital into the banking system, the

government purchased $207.5 billion dollars in preferred stock in certain institutions during 2008. During the fourth quarter

of 2008, we sold $4.9 billion in preferred stock and related warrants, the maximum amount allowed under the CPP, to the

Treasury. Our decision to participate was made to enhance our already solid capital position and to allow us to further expand

our business. We believe that our decision to sell the maximum shares was prudent in order to bolster capital as a result of

increasingly adverse economic results. Upon receipt of the funds, we developed strategies and tactics to deploy the capital in

a fashion that balances supporting economic stability, safety and soundness, and earnings. Specifically, the additional capital

has been deployed thus far by increasing our agency MBS and loans, as well as by decreasing short-term borrowings. We

recognize our responsibility to use proceeds from the CPP in a manner that is consistent with the public interest and are

committed to providing timely public disclosure of our deployment of the CPP proceeds. See additional discussion in the

“Capital Resources” and “Liquidity Risk” sections of this MD&A.

The degree of government intervention through the purchase of direct investments in private and public companies is

unprecedented. As a result, the complete effect and impact from these actions is uncertain. In addition, several federal, state,

and local legislative proposals are pending that may affect our business. It is unclear whether these will be enacted, and if so,

the impact they will have on our industry. We remain active and vigilant in monitoring these developments and supporting

the interests of our shareholders, while also supporting the broader economy.

In addition, during October 2008, the FDIC announced the TLGP, under which it would temporarily guarantee certain new

debt issued by insured banks and qualifying bank holding companies and temporarily expand its insurance to cover all

noninterest-bearing transaction accounts. It was also announced that the Federal Reserve would serve as a buyer of

commercial paper. These actions, among others, were anticipated to stimulate consumer confidence in the economy and

financial institutions, as well as encourage financial institutions to continue lending to businesses, consumers, and each other.

We have issued $3.0 billion in debt under the TLGP, which provides us with a lower cost of funding due to narrower credit

spreads realized in association with the FDIC guarantee. See additional discussion in the “Other Short-Term Borrowings and

Long-Term Debt” section of this MD&A.

In December, the Federal Reserve (“Fed”) took unprecedented action in lowering the federal funds rate by 75 basis points to

a targeted range of zero to one-quarter percent. The Board of Governors also lowered the discount rate 75 basis points to

one-half percent. This action was the seventh rate cut of the year causing the Prime rate to decline 400 basis points since

January 1, 2008 to 3.25% at year end. Further, the Fed increased its Term Auction Facility (“TAF”) program offerings during

the year by $445 billion, which are similar borrowing instruments to term federal funds. In addition, due to the continuing

strain on the financial markets, the Fed has offered numerous temporary liquidity facilities in an effort to stabilize credit

markets and improve the access to credit of businesses and households. See the “Liquidity Risk” section in this MD&A for

additional discussion of the Fed’s actions.

While our most immediate priority is to maintain the fundamental financial strength of the organization, we continue to run a

successful organization serving clients, making sound credit decisions, generating deposits, and operating as efficiently as

possible. To this end, during the year we grew average loans and consumer and commercial deposits 4.5% and 3.4%,

respectively, and improved our loan and deposit mix while maintaining our net interest income at levels comparable to the

prior year. We also experienced growth in certain fee income associated with our core businesses. Further, we tightly

managed growth of core operating expenses, which reflected the continuing success of our ongoing program to improve

efficiency and productivity, although expenses continue to be pressured by increased credit-related costs. We solidified our

capital position during the year through the preferred stock issuance discussed above and also completed three separate

transactions to optimize our long-term holdings of Coke common stock. See “Investment in Common Shares of The Coca-

Cola Company” in this MD&A for additional discussion. We are pursuing initiatives that will expand our revenue generation

capacity, improve efficiency, increase profitability on a risk adjusted basis, and prudently manage credit. To that end, the

most important factors upon which management has and will continue to focus include prudent lending practices, credit loss

mitigation, expense management, growing customer relationships, and increasing brand awareness.

Successfully managing through the current credit cycle is of critical importance. Given the significant downturn in the

economy during 2008, we expect this credit cycle to be protracted. Credit quality deteriorated significantly in 2008 due to the

20