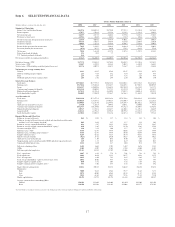

SunTrust 2008 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

sale, in part due to the elimination of Alt-A loans from the warehouse. The increase was also a result of lower valuation

losses on illiquid and delinquent warehouse loans and the earlier recognition of servicing value and origination fees resulting

from our election to record certain mortgage loans at fair value beginning in May 2007. The prior period also included $42.2

million of income reductions recorded in conjunction with our election to record certain loans held for sale at fair value.

These increases in income when compared with 2007 were offset by an increase in our reserve for write-downs on mortgage

loans that we anticipate we will have to repurchase from prior sales. This reserve is established at the time of the sale based

on expectations for the volume of repurchases and the severity of losses upon ultimate disposition. In the current

environment, higher customer default rates, heightened scrutiny of loan documentation by investors, and larger write-downs

upon repurchase are all impacting the level of required reserves. In addition to this offset to mortgage production related

income, we also incurred negative valuation adjustments on our portfolio loans and loans held for sale carried at fair value

and lower fee income associated with lower production volume. While loan production is down, the percentage of agency

eligible secondary market production increased to approximately 98% of secondary market production compared to

approximately 85% in 2007. Agency eligible loans, also known as conforming loans, are defined as mortgage loans eligible

for secondary market purchase by GNMA, FNMA, or FHLMC. To be considered eligible, loans must adhere to maximum

loan amount guidelines, debt-to-income ratio limits, and stricter documentation requirements. In addition, dramatically lower

mortgage rates near the end of 2008 drove a significant increase in application activity, which has continued into early 2009.

Investment banking income increased $21.6 million, or 10.1%, compared to 2007, due to increases in direct finance and bond

underwriting fees. These increases were partially offset by a decrease in M&A fees.

Net gain on the sale of businesses consists of an $89.4 million gain on the sale of our remaining interest in Lighthouse

Investment Partners during the first quarter of 2008, an $81.8 million gain on the sale of TransPlatinum, our former fuel card

and fleet management subsidiary in the third quarter of 2008, a $29.6 million gain on the sale of First Mercantile, a

retirement plan services subsidiary, during the second quarter of 2008, and a $2.7 million loss on the sale of a majority

interest in Zevenbergen Capital Investments during the fourth quarter of 2008. A gain of $32.3 million was recognized in

2007 upon the merger of Lighthouse Partners.

During the first quarter of 2008, Visa completed its IPO and upon the closing, approximately 2 million of our Class B shares

were mandatorily redeemed for $86.3 million, which was recorded as a gain in noninterest income.

Net securities gains of $1.1 billion for 2008 included a $732.2 million gain on the sale and contribution of a portion of our

investment in Coke common stock in addition to a $413.1 million gain on the sale of MBS held in conjunction with our risk

management strategies associated with economically hedging the value of MSRs. These gains were partially offset by the

recognition through earnings of $83.8 million in charges related to certain ABS that were determined in 2008 to be other-

than-temporarily impaired. The net securities gains of $243.1 million for 2007 included a $234.8 million gain on the sale of

4.5 million shares of Coke common stock. For additional information on transactions related to our holdings in Coke

common stock, refer to “Investment in Common Shares of The Coca-Cola Company” within this MD&A.

During the fourth quarter of 2007, we completed multiple sale/leaseback transactions, consisting of over 300 of our branch

properties and various individual office buildings. In total, we sold and concurrently leased back $545.9 million in land and

buildings with associated accumulated depreciation of $285.7 million. For the year ended December 31, 2007, we recognized

$118.8 million of the gain immediately while the remaining $385.4 million in gains were deferred and will be recognized

ratably over the expected term of the respective leases, predominantly 10 years, as an offset to net occupancy expense.

During 2008, we completed sale/leaseback transactions, consisting of 152 branch properties and various individual office

buildings. In total, we sold and concurrently leased back $201.9 million in land and buildings with associated accumulated

depreciation of $110.3 million. For the year ended December 31, 2008, we recognized $37.0 million of the gain immediately

while the remaining $160.3 million in gains were deferred and will be recognized ratably over the expected term of the

respective leases, predominantly as an offset to net occupancy expense.

Other income decreased $110.3 million, or 31.5%, compared to 2007. The decline was primarily due to gains in 2007 on

private equity transactions that did not recur in 2008.

26