SunTrust 2008 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

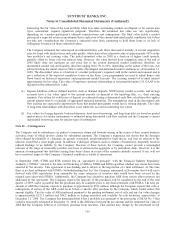

Credit Risk

The credit risk associated with the underlying cash flows of an instrument carried at fair value was a consideration in

estimating the fair value of certain financial instruments. Credit risk was considered in the valuation through a variety of

inputs, as applicable, including, the actual default and loss severity of the collateral, the instrument’s spread in relation

to U.S. Treasury rates, the capital structure of the security and level of subordination, or the rating on a security/obligor

as defined by nationally recognized rating agencies. The assumptions used to estimate credit risk applied relevant

information that a market participant would likely use in valuing an instrument.

For loan products that the Company has elected to carry at fair value, the Company has considered the component of the

fair value changes due to instrument-specific credit risk, which is intended to be an approximation of the fair value

change attributable to changes in borrower-specific credit risk. For the year ended December 31, 2008, SunTrust

recognized a loss on loans accounted for at fair value of approximately $46.6 million, due to changes in fair value

attributable to borrower-specific credit risk. Due to the fact that an insignificant percentage of the loans carried at fair

value during the year ended December 31, 2007 were on nonaccrual status or past due or had other characteristics

generating borrower-specific credit risk, the Company did not ascribe any significant fair value changes to borrower-

specific credit risk during that period. In addition to borrower-specific credit risk, there are other, more significant

variables that will drive changes in the fair value of the loans, including changes in interest rates and general conditions

in the principal markets for the loans.

For the publicly-traded fixed rate debt carried at fair value, the Company estimated credit spreads above U.S. Treasury

rates, based on credit spreads from actual or estimated trading levels of the debt. Prior to the second quarter of 2008, the

Company had estimated the impacts of its own credit spreads over LIBOR; however, given the volatility in the interest

rate markets during 2008, the Company analyzed the difference between using U.S. Treasury rates and LIBOR. While

the historical analysis indicated only minor differences, the Company believes that beginning in the second quarter of

2008 a more accurate depiction of the impacts of changes in its own credit spreads is to base such estimation on the U.S.

Treasury rate, which reflects a risk-free interest rate. Further supporting this decision, LIBOR has recently exhibited

extreme volatility and remained at elevated levels due to the global credit crisis. A reason the Company had selected

LIBOR in the past was due to the presence of LIBOR-based interest rate swap contracts that the Company had

historically used to hedge its interest rate exposure on these debt instruments under SFAS No. 133. The Company may,

however, also purchase fixed rate trading securities in an effort to hedge its fair value exposure to its fixed rate debt. The

Company may also continue to use interest rate swap contracts to hedge interest exposure on future fixed rate debt

issuances pursuant to the provisions of SFAS No. 133. The Company recognized a gain of approximately $398.1 million

for the year ended December 31, 2008, and a gain of approximately $157.5 million for the year ended December 31,

2007, due to changes in its own credit spread on its public debt as well as its brokered deposits. Credit spreads widened

throughout 2008 in connection with the continued deterioration of the broader financial markets and in the financial

services industry, in particular.

150