SunTrust 2008 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

in their homes. Finally, it should be noted that funds

received through the Capital Purchase Program come

with interest costs, certain conditions, and a

commitment to repay. Additional information regarding

our participation in this program is available under

the investor relations section of our website at

www.suntrust.com.

Let me be very clear that managing responsibly through

this crisis — controlling what we can control — is

our most immediate priority. We are focused on the

fundamentals: serving clients, making sound credit

decisions, managing our risk profile, and operating

as efficiently as possible. Doing all this does not mean

that we can not, and should not, also be looking beyond

the current turmoil to market stabilization and the

ultimate resumption of economic growth that history

tells us will, at some point, be forthcoming.

Our performance on the other side of this tough cycle will

in large part be driven by initiatives we are pursuing today

to increase efficiency, expand our revenue generation

capability, improve the profitability of the balance sheet,

and prudently manage credit.

Focus on Efciency

Today, SunTrust is a leaner, more efficient, and more

productive organization than was the case just a short

time ago. This improvement is the direct result of the

ongoing success of a program initiated in 2007 called

“E2” (for “Excellence in Execution”). The overall program

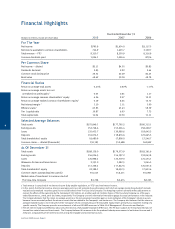

goal is to achieve $600 million in run-rate savings

during 2009, which is over 11% of our 2006 noninterest

expense base. Steady progress toward that goal was

achieved in 2008.

It was financially advantageous to have the E2 program

in place and yielding results well before economic

conditions soured and pressure on revenue growth

increased. Further, a real cultural shift has taken place

within in our organization around efficiency and

productivity that augurs well for the future. In the

meantime, in response to the difficult operating

climate, we undertook additional and meaningful

actions to rein in expenses. For instance, management

recommended to the Board that no annual cash bonuses

be paid to select members of the executive leadership

group for 2008. Furthermore, we will not provide

merit increases during 2009 for SunTrust’s broader

leadership group comprising over 4,000 individuals.

We are committed to producing ongoing and sustainable

savings that will result in a more efficient organization.

Investing for Future Growth

Success in reducing the growth rate of expenses is

permitting increased investment to improve the future

revenue-generating capacity of the organization. Examples

include several small acquisitions that augment existing

capabilities and expand our product offerings. For

example, SunTrust’s position in the higher-growth metro

Atlanta market was strengthened with the acquisition of

a small bank, GB&T Bancshares, while in central Florida

we were pleased to support the FDIC by acquiring the

deposits of a community bank that had been closed

by banking authorities. The capabilities of our wealth

management family office affiliate, GenSpring, and our

RidgeWorth Capital Management arm were also expanded

during the year. Meanwhile, the value of investments in

branch and other retail delivery channels was reflected in

solid deposit growth in 2008.

The investment most visible in the marketplace was in a

reinvigorated brand identity — “Live Solid. Bank Solid.”

— designed to speak to what is important to current

and prospective clients in today’s environment. Research

confirms that what clients want is a solid banking

experience, one that is free of unnecessary barriers

and confusion and that gets the basics right every time,

thus helping them “Live Solid.” As for “Bank Solid,”

that reflects the importance of being financially strong

and delivering exceptional service consistently through

capable and engaged employees.

Specific actions are under way to deliver on the “Bank

Solid” promise. The already high bar on client service

was raised in 2008 by setting new client experience

standards across the organization. Leveraging client

segmentation is creating a better understanding of client

needs. Products, policies, and procedures are being

simplified, and channel access expanded.

Improving Protability while Managing Risk

To improve profitability, higher margin, higher risk-adjusted

return products and services are targeted for growth,

while lower-return assets and higher-cost deposits are

being reduced. Increasing commercial loans, for example,

is a priority while it is prudent in the current economy to

reduce our exposure to certain other loan categories such

as residential construction loans.

Even though loan demand typically softens in a

recessionary environment, the lending business — our

cornerstone business — is of critical importance. It is not

just a source of revenue but also is central to supporting

SunTrust 2008 Annual Report

2