SunTrust 2008 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2008 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

In addition, SunTrust sets pension asset values equal to their market value, in contrast to the use of a smoothed asset value

that incorporates gains and losses over a period of years. Utilization of market value of assets provides a more realistic

economic measure of the plan’s funded status and cost. Assumed discount rates and expected returns on plan assets affect the

amounts of net periodic benefit cost. A 25 basis point decrease in the discount rate or expected long-term return on plan

assets would increase the Retirement Benefits net periodic benefit cost approximately $11 million and $5 million,

respectively.

Assumed healthcare cost trend rates have a significant effect on the amounts reported for the other postretirement plans. As

of December 31, 2008, SunTrust assumed that retiree health care costs will increase at an initial rate of 8.50% per year.

SunTrust assumed a healthcare cost trend that recognizes expected medical inflation, technology advancements, rising cost of

prescription drugs, regulatory requirements and Medicare cost shifting. SunTrust expects this annual cost increase to

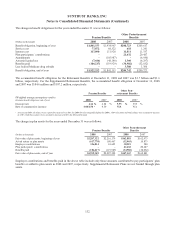

decrease over a 6-year period to 5.25% per year. Due to changing medical inflation, it is important to understand the effect of

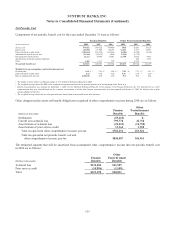

a one-percent point change in assumed healthcare cost trend rates. These amounts are shown below:

(Dollars in thousands) 1% Increase 1% Decrease

Effect on other postretirement benefit obligation $12,844 ($11,202)

Effect on total service and interest cost 730 (630)

Note 17 – Derivative Financial Instruments

The Company enters into various derivatives both in a dealer capacity to facilitate client transactions and as an end user as a

risk management tool. Where contracts have been entered into with clients, the Company generally manages the risk

associated with these contracts within the framework of its VaR approach that monitors total exposure daily and seeks to

manage the exposure on an overall basis. Derivatives are used as a risk management tool to hedge the Company’s exposure

to changes in interest rates or other identified market risks, either economically or in accordance with the hedge accounting

provisions of SFAS No. 133. The Company may also enter into derivative positions, on a limited basis, to capitalize upon

arbitrage opportunities in the market. In addition, as a normal part of its operations, the Company enters into IRLCs on

mortgage loans that are accounted for as freestanding derivatives under SFAS No. 133 and has certain contracts containing

embedded derivatives that are carried, in their entirety, at fair value under SFAS No. 155 or SFAS No. 159. All derivatives

are carried at fair value in the Consolidated Balance Sheets in trading assets, other assets, trading liabilities, or other

liabilities. The gains and losses associated with these instruments are either recorded in other comprehensive income, net of

tax, or within the Consolidated Statements of Income depending upon the use and designation of the derivatives.

Derivatives offered to clients include interest rate, credit, equity, commodity, and foreign exchange contracts. The

Company’s risk management derivatives are based on underlying risks primarily related to interest rates, equity valuations,

foreign exchange rates, or credit, and include swaps, options, swaptions, credit default swaps, currency swaps, and futures

and forwards. Swaps are contracts in which a series of net cash flows, based on a specific notional amount that is related to

an underlying risk, are exchanged over a prescribed period. Options, generally in the form of caps and floors, are contracts

that transfer, modify, or reduce an identified risk in exchange for the payment of a premium when the contract is issued.

Swaptions are contracts that provide the option to enter into a specified swap agreement with the issuer on a specified future

date. Credit default swaps provide credit protection for the buyer of the contract through a guarantee, by the seller of the

contract, of the creditworthiness of the underlying fixed income product. Currency swaps involve the exchange of principal

and interest in one currency for another. Futures and forwards are contracts for the delayed delivery or net settlement of an

underlying, such as a security or interest rate index, in which the seller agrees to deliver on a specified future date, either a

specified instrument at a specified price or yield or the net cash equivalent of an underlying.

Credit and Market Risk Associated with Derivatives

Derivatives expose the Company to credit risk. If the counterparty fails to perform, the credit risk at that time would be equal

to the net derivative asset position, if any, for that counterparty. The Company minimizes the credit or repayment risk in

derivative instruments by entering into transactions with high quality counterparties that are reviewed periodically by the

Company’s Credit Risk Management division. The Company’s derivatives may also be governed by an International Swaps

and Derivatives Associations Master Agreement (“ISDA”); depending on the nature of the derivative transactions, bilateral

collateral agreements may be in place as well. When the Company has more than one outstanding derivative transaction with

a single counterparty and there exists a legally enforceable master netting agreement with the counterparty, the Company

considers its exposure to the counterparty to be the net market value of all positions with that counterparty if such net value is

136