Capital One 2008 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2008 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

69

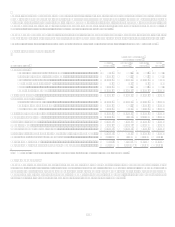

The precision of the measures used to manage interest rate risk is limited due to the inherent uncertainty of the underlying forecast

assumptions. These measures do not consider the impact of the effects of changes in the overall level of economic activity associated

with various interest rate scenarios. In addition, the measurement of interest rate sensitivity includes assumptions on the ability of

management to take action to mitigate further exposure to changes in interest rates, including, within legal and competitive

constraints, the re-pricing of interest rates on outstanding credit card loans and deposits.

The Company manages and mitigates its interest rate sensitivity through several techniques, which include, but are not limited to,

changing the maturity and re-pricing characteristics of various balance sheet categories and by entering into interest rate derivatives.

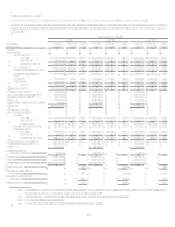

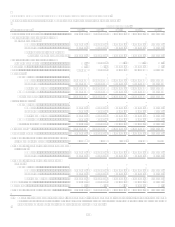

Table 14 reflects the interest rate repricing schedule for earning assets and interest-bearing liabilities as of December 31, 2008.

Table 14: Interest Rate Sensitivity

As of December 31, 2008

Subject to Repricing

(Dollars in Millions)

Within

180 Days

>180 Days-

1 Year

>1 Year-

5 Years

Over

5 Years

Earning assets:

Federal funds sold and resale agreement...............................................

.

$ 637 $ $ $

Interest-bearing deposits at other banks ................................................

.

4,807

Securities available for sale...................................................................

.

10,641 3,265 16,158 939

Mortgage loans held for sale(1)...............................................................

.

15 11 54 14

Other .....................................................................................................

.

2,366

Loans held for investment.....................................................................

.

42,858 11,956 41,403 4,801

Total earning assets ........................................................................................

.

61,324 15,232 57,615 5,754

Interest-bearing liabilities:

Interest-bearing deposits .......................................................................

.

63,628 12,698 18,794 2,207

Senior and subordinated notes ..............................................................

.

1,444 2,931 3,934

Other borrowings ..................................................................................

.

9,337 626 3,239 1,668

Total interest-bearing liabilities......................................................................

.

74,409 13,324 24,964 7,809

Non-rate related net items...............................................................................

.

11,308 (103) (1,725) 3,946

Interest sensitivity gap ....................................................................................

.

(1,778) 1,805 30,927 1,891

Impact of swaps..............................................................................................

.

5,519 (2,549) (5,611) 2,641

Impact of consumer loan securitizations.........................................................

.

(6,061) (1,152) 3,702 1,207

Interest sensitivity gap adjusted for impact of securitizations and swaps.......

.

(2,320) 408 29,018 5,739

Adjusted gap as a percentage of managed assets............................................

.

(1.11)% 0.19% 13.83% 2.73 %

Adjusted cumulative gap ................................................................................

.

(165 ) 1,912 27,106 32,845

Adjusted cumulative gap as a percentage of managed assets .........................

.

(1.11)% (0.91)% 12.92% 15.65 %

(1) Mortgage loans held for sale line item excludes the related lower of cost or market adjustments.

Foreign Exchange Risk

The Company is exposed to changes in foreign exchange rates which may impact translated income and expense associated with

foreign operations. In order to limit earnings exposure to foreign exchange risk, the Companys Asset/Liability Management Policy

requires that material foreign currency denominated transactions be hedged. As of December 31, 2008, the estimated reduction in 12-

month earnings due to adverse foreign exchange rate movements corresponding to a 95% probability is less than 2%. The precision of

this estimate is also limited due to the inherent uncertainty of the underlying forecast assumptions.