Capital One 2008 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2008 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

87

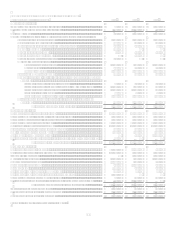

QSPEs. QSPEs are passive entities that are commonly used in mortgage, credit card, auto and installment loan securitization

transactions. SFAS 140 establishes the criteria an entity must satisfy to be a QSPE which includes restrictions on the types of assets a

QSPE may hold, limits on repurchase of assets, the use of derivatives and financial guarantees, and the level of discretion a servicer

may exercise to collect receivables. SPEs that meet the criteria for QSPE status are not required to be consolidated. The Company uses

the QSPE model to conduct off-balance sheet securitization activities. See Note 18 for more information on the Companys off-

balance sheet securitization activities.

In April 2008, The Financial Accounting Standards Board (FASB) voted to eliminate the concept of QSPEs from the accounting

guidance. On September 15, 2008, the FASB issued exposure drafts to amend SFAS 140 and FIN46R. The two proposed Statements

would significantly change accounting for transfers of financials assets, due to elimination of the concept of a QSPE, and would

change the criteria for determining whether to consolidate a VIE. The proposals are currently in a public comment period and are

subject to change. As the proposals stand, however, the change would have a significant impact on the Companys consolidated

financial statements as a result of the loss of sales treatment for assets previously sold to a QSPE, as well as for future sales. As of

December 31, 2008, the total assets of QSPEs to which the Company has transferred and received sales treatment were $45.9 billion.

VIEs: Special purpose entities that are not QSPEs are considered for consolidation in accordance with FIN46(R), which defines a VIE

as an entity that (1) lacks sufficient equity to finance its activities without additional subordinated financial support; (2) has equity

owners that lack the ability to make significant decisions about the entity; or (3) has equity owners do not have the obligation to

absorb expected losses or the right to receive expected returns. In general, a VIE may be formed as a corporation, partnership, limited

liability corporation, or any other legal structure used to conduct activities or hold assets. A VIE often holds financial assets, including

loans or receivables, real estate or other property.

The Company consolidates a VIE if the Company is considered to be its primary beneficiary. The primary beneficiary is subject to

absorbing the majority of the expected losses from the VIEs activities, is entitled to receive a majority of the entities residual returns,

or both.

The Company, in the ordinary course of business, has involvement with or retains interests in VIEs in connection with some of its

securitization activities, servicing activities, the purchase or sale of mortgage-backed and other asset backed securities in connection

with its investment portfolio. The Company also makes loans to VIEs that hold debt, equity, real estate or other assets. In certain

instances, the Company provides guarantees to VIEs or holders of variable interests in VIEs. See Note 13 Mortgage Servicing

Rights; Note 18 Securitizations; Note 19 Commitments, Contingencies and Guarantees; and Note 20 Other Variable Interest

Entities for more detail on the Companys involvement and exposure related to non-consolidated VIEs.

Recent Accounting Pronouncements

In January 2009, the FASB issued FASB Staff Position (FSP) No. EITF 99-20-1, Recognition of Interest Income and Impairment

on Purchased Beneficial Interests and Beneficial Interests That Continue to Be Held by a Transferor in Securitized Financial Assets.

(FSP EITF 99-20) The FSP was issued to achieve more consistent determination of whether an other-than-temporary impairment

has occurred. The FSP also retains and emphasizes the objective of an other-than-temporary impairment assessment and the related

disclosure requirements in SFAS No. 115, Accounting for Certain Investments in Debt and Equity Securities, (SFAS 115) and

other related guidance. FSP EITF 99-20 emphasizes that any other-than-temporary impairment resulting from the application of SFAS

115 or EITF 99-20 shall be recognized in earnings equal to the entire difference between the investments cost and its fair value at the

balance sheet date of the reporting period for which the assessment is made. FSP EITF 99-20 is effective for interim and annual

reporting periods ending after December 15, 2008, and shall be applied prospectively. Retrospective application to a prior interim or

annual reporting period is not permitted. The adoption of FSP EITF 99-20 did not have impact on consolidated earnings or financial

position of the Company. See Note 4 for additional details.

In December 2008, the FASB issued FSP No. FAS 140-4 and FIN 46(R)-8, Disclosures by Public Entities (Enterprises) about

Transfers of Financial Assets and Interests in Variable Interest Entities, (FSP FAS 140-4 and FIN 46(R)-8). FSP FAS 140-4 and

FIN 46(R)-8 amends SFAS 140 and FIN 46(R). This FSP requires public companies to provide additional disclosures about their

involvement with variable interest entities. This FSP is effective for the first reporting period ending after December 15, 2008. This

FSP does not impact the consolidated earnings or financial position of the Company. See Note 20 for additional detail.

In June 2008, the FASB issued FSP EITF 03-6-1, Determining Whether Instruments Granted in Share-Based Payment Transactions

Are Participating Securities. The FSP addresses whether instruments granted in share-based payment transactions are participating

securities prior to vesting and therefore need to be included in the earnings allocation in calculating earnings per share under the two-

class method described in SFAS No. 128, Earnings per Share. (SFAS 128) The FSP requires companies to treat unvested share-

based payment awards that have non-forfeitable rights to dividend or dividend equivalents as a separate class of securities in

calculating earnings per share. The FSP is effective for fiscal years beginning after December 15, 2008; earlier application is not

permitted. We do not expect adoption of FSP EITF 03-6-1 to have a material effect on our results of operations or earnings per share.