Capital One 2008 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2008 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

|

|

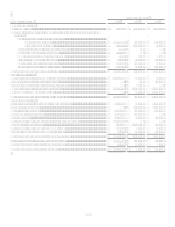

148

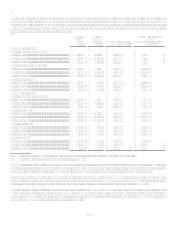

As of December 31, 2008, the Banks each exceeded the minimum regulatory requirements to which it was subject. The Banks all were

considered well-capitalized under applicable capital adequacy guidelines. Also as of December 31, 2008, the Corporation was

considered well-capitalized under Federal Reserve capital standards for bank holding companies and, therefore, exceeded all

minimum capital requirements. There have been no conditions or events since that we believe would have changed the capital

category of the Corporation or either of the Banks.

Regulatory

Filing

Basis

Ratios

Applying

Subprime

Guidance

Ratios

Minimum for Capital

Adequacy Purposes

To Be Well Capitalized

Under

Prompt Corrective Action

Provisions

December 31, 2008

Capital One Financial Corp.(1)

Tier 1 Capital .......................................................... 13.76% 12.76% 4.00% N/A

Total Capital ........................................................... 16.60 15.48 8.00 N/A

Tier 1 Leverage....................................................... 11.13 11.13 4.00 N/A

Capital One Bank (USA) N.A.

Tier 1 Capital .......................................................... 13.02% 9.99% 4.00% 6.00 %

Total Capital ........................................................... 15.65 12.26 8.00 10.00

Tier 1 Leverage....................................................... 11.79 11.79 4.00 5.00

Capital One, N.A.

Tier 1 Capital .......................................................... 10.54% N/A 4.00% 6.00 %

Total Capital ........................................................... 11.86 N/A 8.00 10.00

Tier 1 Leverage....................................................... 7.85 N/A 4.00 5.00

December 31, 2007

Capital One Financial Corp.(1)

Tier 1 Capital .......................................................... 10.13% 9.49% 4.00% N/A

Total Capital ........................................................... 13.05 12.29 8.00 N/A

Tier 1 Leverage....................................................... 9.00 9.00 4.00 N/A

Capital One Bank

Tier 1 Capital .......................................................... 13.48% 10.45% 4.00% 6.00 %

Total Capital ........................................................... 16.57 13.06 8.00 10.00

Tier 1 Leverage....................................................... 12.81 12.81 4.00 5.00

Capital One, N.A.

Tier 1 Capital .......................................................... 10.75% N/A 4.00% 6.00 %

Total Capital ........................................................... 12.11 N/A 8.00 10.00

Tier 1 Leverage....................................................... 8.37 N/A 4.00 5.00

Superior Bank(2)

Tier 1 Capital .......................................................... 15.07% N/A 4.00% 6.00 %

Total Capital ........................................................... 16.33 N/A 8.00 10.00

Tier 1 Leverage....................................................... 6.71 N/A 4.00 5.00

(1) The regulatory framework for prompt corrective action is not applicable for bank holding companies.

(2) During 2008, Superior Bank merged with and into CONA

COBNA treats a portion of its loans as subprime under the Guidelines issued by the four federal banking agencies that comprise the

Federal Financial Institutions Examination Council (FFIEC), and has assessed its capital and allowance for loan and lease losses

accordingly. Under the Guidelines, COBNA exceeds the minimum capital adequacy guidelines as of December 31, 2008.

For purposes of the Guidelines, the Corporation has treated as subprime all loans in COBNAs targeted subprime programs to

customers either with a FICO score of 660 or below or with no FICO score. COBNA holds on average 200% of the total risk-based

capital charge that would otherwise apply to such assets. This results in higher levels of regulatory capital at COBNA.

Additionally, regulatory restrictions exist that limit the ability of COBNA and CONA to transfer funds to the Corporation. As of

December 31, 2008, retained earnings of COBNA and CONA were $239.3 million and zero million, respectively. The retained

earnings of COBNA are available for payment as dividends to the Corporation without prior approval of the OCC while a dividend

payment by CONA would require prior approval of the OCC.