Sallie Mae 2013 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

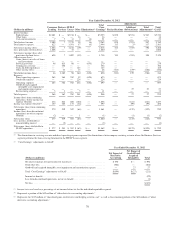

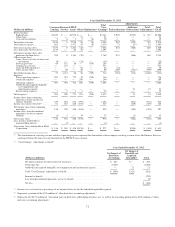

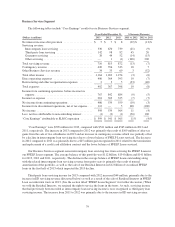

Differences between “Core Earnings” and GAAP

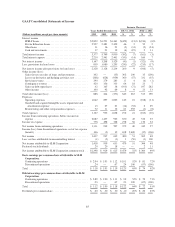

The two adjustments required to reconcile our “Core Earnings” results to our GAAP results of operations

relate to differing treatments for: (1) our use of derivative instruments to hedge our economic risks that do not

qualify for hedge accounting treatment or do qualify for hedge accounting treatment but result in ineffectiveness;

and (2) the accounting for goodwill and acquired intangible assets. The following table reflects aggregate

adjustments associated with these areas.

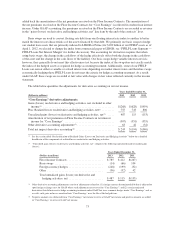

Years Ended December 31,

(Dollars in millions) 2013 2012 2011

“Core Earnings” adjustments to GAAP:

Net impact of derivative accounting ........................ $243 $(194) $(540)

Net impact of goodwill and acquired intangible assets ......... (13) (27) (21)

Net income tax effect ................................... (96) 99 219

Net effect from discontinued operations .................... (6) (1) (2)

Total “Core Earnings” adjustments to GAAP ................ $128 $(123) $(344)

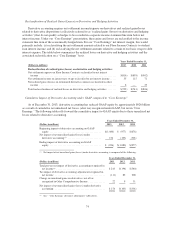

1) Derivative Accounting: “Core Earnings” exclude periodic unrealized gains and losses that are caused by

the mark-to-market valuations on derivatives that do not qualify for hedge accounting treatment under GAAP, as

well as the periodic unrealized gains and losses that are a result of ineffectiveness recognized related to effective

hedges under GAAP. These unrealized gains and losses occur in our Consumer Lending, FFELP Loans and

Other business segments. Under GAAP, for our derivatives that are held to maturity, the cumulative net

unrealized gain or loss over the life of the contract will equal $0 except for Floor Income Contracts, where the

cumulative unrealized gain will equal the amount for which we sold the contract. In our “Core Earnings”

presentation, we recognize the economic effect of these hedges, which generally results in any net settlement

cash paid or received being recognized ratably as an interest expense or revenue over the hedged item’s life.

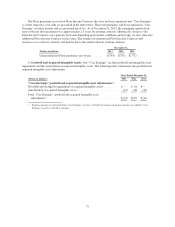

The accounting for derivatives requires that changes in the fair value of derivative instruments be

recognized currently in earnings, with no fair value adjustment of the hedged item, unless specific hedge

accounting criteria are met. We believe that our derivatives are effective economic hedges, and as such, are a

critical element of our interest rate and foreign currency risk management strategy. However, some of our

derivatives, primarily Floor Income Contracts and certain basis swaps, do not qualify for hedge accounting

treatment and the stand-alone derivative must be marked-to-market in the income statement with no

consideration for the corresponding change in fair value of the hedged item. These gains and losses recorded in

“Gains (losses) on derivative and hedging activities, net” are primarily caused by interest rate and foreign

currency exchange rate volatility and changing credit spreads during the period as well as the volume and term of

derivatives not receiving hedge accounting treatment.

Our Floor Income Contracts are written options that must meet more stringent requirements than other

hedging relationships to achieve hedge effectiveness. Specifically, our Floor Income Contracts do not qualify for

hedge accounting treatment because the pay down of principal of the student loans underlying the Floor Income

embedded in those student loans does not exactly match the change in the notional amount of our written Floor

Income Contracts. Additionally, the term, the interest rate index, and the interest rate index reset frequency of the

Floor Income Contract can be different than that of the student loans. Under derivative accounting treatment, the

upfront payment is deemed a liability and changes in fair value are recorded through income throughout the life

of the contract. The change in the value of Floor Income Contracts is primarily caused by changing interest rates

that cause the amount of Floor Income earned on the underlying student loans and paid to the counterparties to

vary. This is economically offset by the change in value of the student loan portfolio earning Floor Income but

that offsetting change in value is not recognized. We believe the Floor Income Contracts are economic hedges

because they effectively fix the amount of Floor Income earned over the contract period, thus eliminating the

timing and uncertainty that changes in interest rates can have on Floor Income for that period. Therefore, for

purposes of “Core Earnings,” we have removed the unrealized gains and losses related to these contracts and

72