Sallie Mae 2013 Annual Report Download - page 187

Download and view the complete annual report

Please find page 187 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

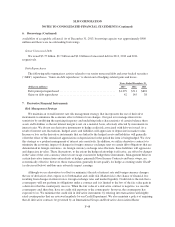

7. Derivative Financial Instruments (Continued)

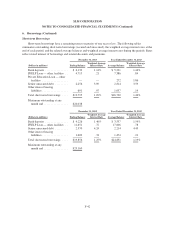

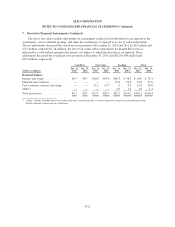

Agreement. Depending on the nature of the derivative transaction, bilateral collateral arrangements generally are

required as well. When we have more than one outstanding derivative transaction with the counterparty, and

there exists legally enforceable netting provisions with the counterparty (i.e., a legal right to offset receivable and

payable derivative contracts), the “net” mark-to-market exposure, less collateral the counterparty has posted to

us, represents exposure with the counterparty. When there is a net negative exposure, we consider our exposure

to the counterparty to be zero. At December 31, 2013 and 2012, we had a net positive exposure (derivative gain

positions to us less collateral which has been posted by counterparties to us) related to SLM Corporation and

Sallie Mae Bank derivatives of $83 million and $79 million, respectively.

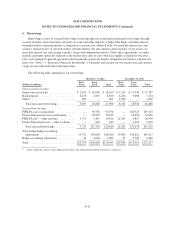

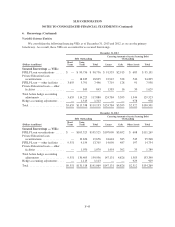

Our on-balance sheet securitization trusts have $10.7 billion of Euro and British Pound Sterling

denominated bonds outstanding as of December 31, 2013. To convert these non-U.S. dollar denominated bonds

into U.S dollar liabilities, the trusts have entered into foreign-currency swaps with highly–rated counterparties. In

addition, the trusts have entered into $12.8 billion of interest rates swaps which are primarily used to convert

Prime received on securitized student loans to LIBOR paid on the bonds. At December 31, 2013, the net positive

exposure on swaps in securitization trusts is $968 million.

Our securitization trusts had total net exposure of $772 million related to financial institutions located in

France; of this amount, $577 million carries a guaranty from the French government. The total exposure relates

to $5.1 billion notional amount of cross-currency interest rate swaps held in our securitization trusts, of which

$3.4 billion notional amount carries a guaranty from the French government. Counterparties to the cross currency

interest rate swaps are required to post collateral when their credit rating is withdrawn or downgraded below a

certain level. As of December 31, 2013, no collateral was required to be posted and we are not holding any

collateral related to these contracts. Adjustments are made to our derivative valuations for counterparty credit

risk. The adjustments made at December 31, 2013 related to derivatives with French financial institutions

(including those that carry a guaranty from the French government) decreased the derivative asset value by

$63 million. Credit risks for all derivative counterparties are assessed internally on a continual basis.

Accounting for Derivative Instruments

Derivative instruments that are used as part of our interest rate and foreign currency risk management

strategy include interest rate swaps, basis swaps, cross-currency interest rate swaps, and interest rate floor

contracts with indices that relate to the pricing of specific balance sheet assets and liabilities. The accounting for

derivative instruments requires that every derivative instrument, including certain derivative instruments

embedded in other contracts, be recorded on the balance sheet as either an asset or liability measured at its fair

value. As more fully described below, if certain criteria are met, derivative instruments are classified and

accounted for by us as either fair value or cash flow hedges. If these criteria are not met, the derivative financial

instruments are accounted for as trading.

Fair Value Hedges

Fair value hedges are generally used by us to hedge the exposure to changes in fair value of a recognized

fixed rate asset or liability. We enter into interest rate swaps to economically convert fixed rate assets into

variable rate assets and fixed rate debt into variable rate debt. We also enter into cross-currency interest rate

swaps to economically convert foreign currency denominated fixed and floating debt to U.S. dollar denominated

variable debt. For fair value hedges, we generally consider all components of the derivative’s gain and/or loss

when assessing hedge effectiveness and generally hedge changes in fair values due to interest rates or interest

rates and foreign currency exchange rates or the total change in fair values.

F-49