Sallie Mae 2013 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

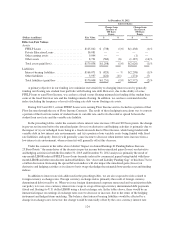

risk exposures, management is able to identify potential risks and develop appropriate responses and mitigation

strategies. Our Board of Directors has agreed our Risk Appetite Framework with management and directed

management to continue its development and evolution with the Audit Committee of our Board of Directors.

Risk Categories

We evaluate our significant risks using the following categories: (1) credit; (2) market; (3) funding &

liquidity; (4) compliance; (5) legal; (6) operational; (7) reputational/political; (8) governance; and (9) strategy.

Credit Risk. Credit risk is the risk to earnings or capital resulting from an obligor’s failure to meet the terms

of any contract with us or otherwise fail to perform as agreed. Credit risk is found in all activities where success

depends on counterparty, issuer or borrower performance.

We have credit or counterparty risk exposure with borrowers and cosigners with whom we have made

Private Education Loans, the various counterparties with whom we have entered into derivative contracts and the

various issuers with whom we make investments. Credit and counterparty risks are overseen by our Chief Credit

Officer, his staff and the internal Credit Committee he chairs. Our Chief Credit Officer reports regularly to our

Board and Finance and Operations and Audit Committees of our Board of Directors.

The credit risk related to Private Education Loans is managed within a credit risk infrastructure which

includes: (i) a well-defined underwriting, asset quality and collection policy framework; (ii) an ongoing

monitoring and review process of portfolio concentration and trends; (iii) assignment and management of credit

authorities and responsibilities; and (iv) establishment of an allowance for loan losses that covers estimated

losses based upon portfolio and economic analysis.

Credit risk related to derivative contracts is managed by reviewing counterparties for credit strength on an

ongoing basis and through our credit policies, which place limits on the amount of exposure we may take with

any one counterparty and, in most cases, require collateral to secure the position. The credit and counterparty risk

associated with derivatives is measured based on the replacement cost should the counterparties with contracts in

a gain position to the Company fail to perform under the terms of the contract.

Market Risk. Market risk is the risk to earnings or capital resulting from changes in market conditions, such

as interest rates, credit spreads, commodity prices or volatilities. We are exposed to various types of market risk,

in particular the risk of loss resulting in a mismatch between the maturity/duration of assets and liabilities,

interest rate risk and other risks that arise through the management of our investment, debt and student loan

portfolios. Market risk exposures are managed primarily through our internal Asset and Liability Committee. The

responsibilities of this committee include: maintaining oversight and responsibility for all risks associated with

managing our assets and liabilities, and recommending limits to be included in our risk appetite and investment

structure. These activities are closely tied to those related to the management of our funding and liquidity risks.

The Finance and Operations Committee of our Board of Directors periodically reviews and approves the

investment and asset and liability management policies and contingency funding plan developed and

administered by our internal Asset and Liability Committee. The Finance and Operations Committee of our

Board of Directors as well as our Executive Vice President — Banking and Finance report to the full Board of

Directors on matters of market risk management.

Funding and Liquidity Risk. Funding and liquidity risk is the risk to earnings, capital or the conduct of our

business arising from the inability to meet our obligations when they become due without incurring unacceptable

losses, such as the ability to fund liability maturities and deposit withdrawals, or invest in future asset growth and

business operations at reasonable market rates, as well as the inability to fund Private Education Loan

originations. Our three primary liquidity needs include our ongoing ability to meet our funding needs for our

businesses throughout market cycles, including during periods of financial stress and to avoid any mismatch

between the maturity of assets and liabilities; our ongoing ability to fund originations of Private Education

Loans; and servicing our indebtedness and bank deposits. Key objectives associated with our funding liquidity

needs relate to our ability to access the capital markets at reasonable rates and to continue to maintain retail

deposits and funding sources through Sallie Mae Bank.

119