Sallie Mae 2013 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

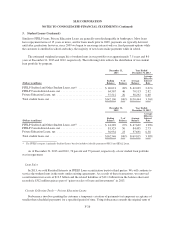

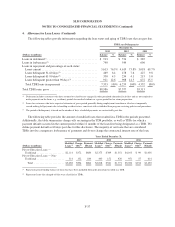

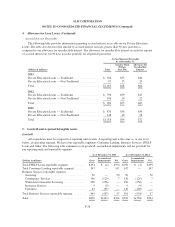

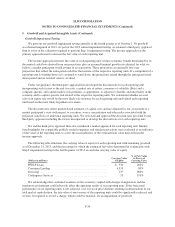

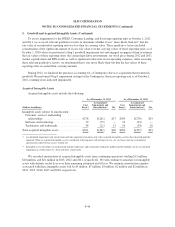

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

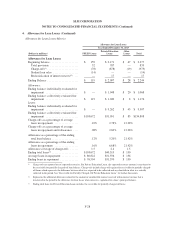

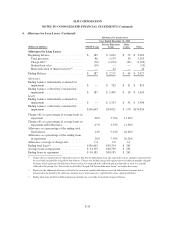

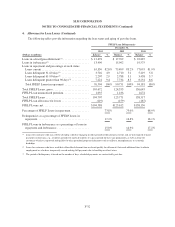

4. Allowance for Loan Losses (Continued)

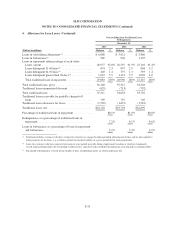

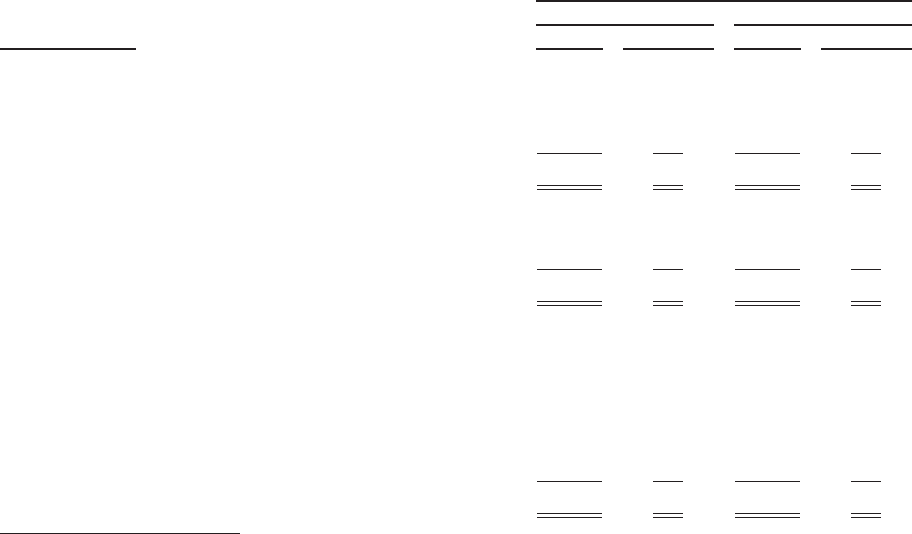

Key Credit Quality Indicators

FFELP Loans are substantially insured and guaranteed as to their principal and accrued interest in the event

of default; therefore, the key credit quality indicator for this portfolio is loan status. The impact of changes in

loan status is incorporated quarterly into the allowance for loan losses calculation.

For Private Education Loans, the key credit quality indicators are school type, FICO scores, the existence of

a cosigner, the loan status and loan seasoning. The school type/FICO score are assessed at origination and

maintained through the traditional/non-traditional loan designation. The other Private Education Loan key quality

indicators can change and are incorporated quarterly into the allowance for loan losses calculation. The following

table highlights the principal balance (excluding the receivable for partially charged-off loans) of our Private

Education Loan portfolio stratified by the key credit quality indicators.

Private Education Loans

Credit Quality Indicators

December 31, 2013 December 31, 2012

(Dollars in millions) Balance(3) % of Balance Balance(3) % of Balance

Credit Quality Indicators

School Type/FICO Scores:

Traditional ........................................ $36,140 93% $35,347 92%

Non-Traditional(1) ................................... 2,860 7 3,207 8

Total ............................................... $39,000 100% $38,554 100%

Cosigners:

With cosigner ...................................... $26,321 67% $24,907 65%

Without cosigner ................................... 12,679 33 13,647 35

Total ............................................... $39,000 100% $38,554 100%

Seasoning(2):

1-12 payments ..................................... $ 5,171 14% $ 7,371 19%

13-24 payments .................................... 5,511 14 6,137 16

25-36 payments .................................... 5,506 14 6,037 16

37-48 payments .................................... 5,103 13 4,780 12

More than 48 payments .............................. 11,181 29 8,325 22

Not yet in repayment ................................ 6,528 16 5,904 15

Total ............................................... $39,000 100% $38,554 100%

(1) Defined as loans to customers attending for-profit schools (with a FICO score of less than 670 at origination) and customers attending not-

for-profit schools (with a FICO score of less than 640 at origination).

(2) Number of months in active repayment for which a scheduled payment was due.

(3) Balance represents gross Private Education Loans.

F-31