Sallie Mae 2013 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

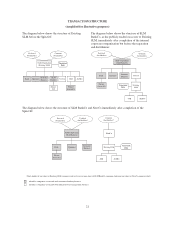

Actions by Federal and State Regulators

Like all depository institutions, Sallie Mae Bank is regulated extensively under federal and state law. Under

federal and state laws and regulations pertaining to the safety and soundness of insured depository institutions,

the UDFI and separately the FDIC as the insurer of bank deposits have the authority to compel or restrict certain

actions on Sallie Mae Bank’s part if they determine that it has insufficient capital or other resources, or is

otherwise operating in a manner that may be deemed to be inconsistent with safe and sound banking practices.

Under this authority, Sallie Mae Bank’s regulators can require it to enter into informal or formal supervisory

agreements, including board resolutions, memoranda of understanding, written agreements and consent or cease

and desist orders, pursuant to which Sallie Mae Bank would be required to take identified corrective actions to

address cited concerns and to refrain from taking certain actions.

Enforcement Powers

We and our nonbank subsidiaries are “institution-affiliated parties” of Sallie Mae Bank, including our

management, employees, agents, independent contractors and consultants, and are generally subject to potential

civil and criminal penalties for violations of law, regulations or written orders of a government agency. Violations

can include failure to timely file required reports, filing false or misleading information or submitting inaccurate

reports. Civil penalties may be as high as $1,000,000 a day for such violations and criminal penalties for some

financial institution crimes may include imprisonment for 20 years. Regulators have flexibility to commence

enforcement actions against institutions and institution-affiliated parties, and the FDIC has the authority to terminate

deposit insurance. When issued by a banking agency, cease and desist and similar orders may, among other things,

require affirmative action to correct any harm resulting from a violation or practice, including restitution,

reimbursement, indemnifications or guarantees against loss. A financial institution may also be ordered to restrict its

growth, dispose of certain assets, rescind agreements or contracts, or take other actions determined to be appropriate

by the ordering agency. The federal banking regulators also may remove a director or officer from an insured

depository institution (or bar them from the industry) if a violation is willful or reckless.

At the time of this filing, Sallie Mae Bank remains subject to a cease and desist order originally issued in

August 2008 by the FDIC and the UDFI. In July 2013, the FDIC notified us that it plans to replace the existing

cease and desist order on Sallie Mae Bank with a new formal enforcement action against Sallie Mae Bank that

would more specifically address certain cited violations of Section 5 of the FTC Act, including practices relating

to payment allocation practices and the disclosures and assessments of certain late fees, as well as alleged

violations under the SCRA. In November 2013, the FDIC notified us that the new formal enforcement action

would be against Sallie Mae Bank and an additional enforcement action would be against SMI, in its capacity as

a servicer of education loans for other financial institutions, and would include civil money penalties and

restitution. Sallie Mae Bank has been notified by the UDFI that it does not intend to join the FDIC in issuing any

new enforcement action. For additional information regarding these regulatory and related matters and the

reserves we have recorded in connection therewith, see Item 3. “Legal Proceedings—Regulatory Matters.” We

and Sallie Mae Bank may be required to, or otherwise determine to, make changes to the business practices and

products of Sallie Mae Bank and our other affiliates to respond to regulatory concerns. Following the Spin-Off,

Sallie Mae Bank will continue to oversee significant activities performed outside Sallie Mae Bank by affiliates.

Standards for Safety and Soundness

The Federal Deposit Insurance Act (the “FDIA”) requires the federal bank regulatory agencies such as the

FDIC to prescribe, by regulation or guideline, operational and managerial standards for all insured depository

institutions, such as Sallie Mae Bank, relating to internal controls, information systems and audit systems, loan

documentation, credit underwriting, interest rate risk exposure, and asset quality. The agencies also must prescribe

standards for asset quality, earnings, and stock valuation, as well as standards for compensation, fees and benefits.

The federal banking regulators have adopted regulations and interagency guidelines prescribing standards for safety

and soundness to implement these required standards. These guidelines set forth the safety and soundness standards

used to identify and address problems at insured depository institutions before capital becomes impaired. Under the

13