Sallie Mae 2013 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

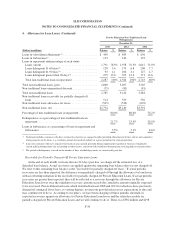

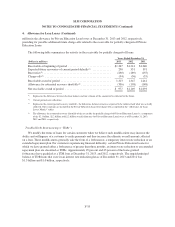

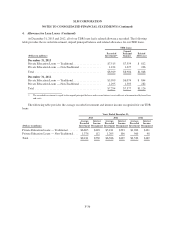

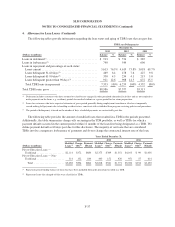

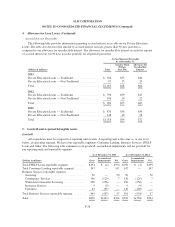

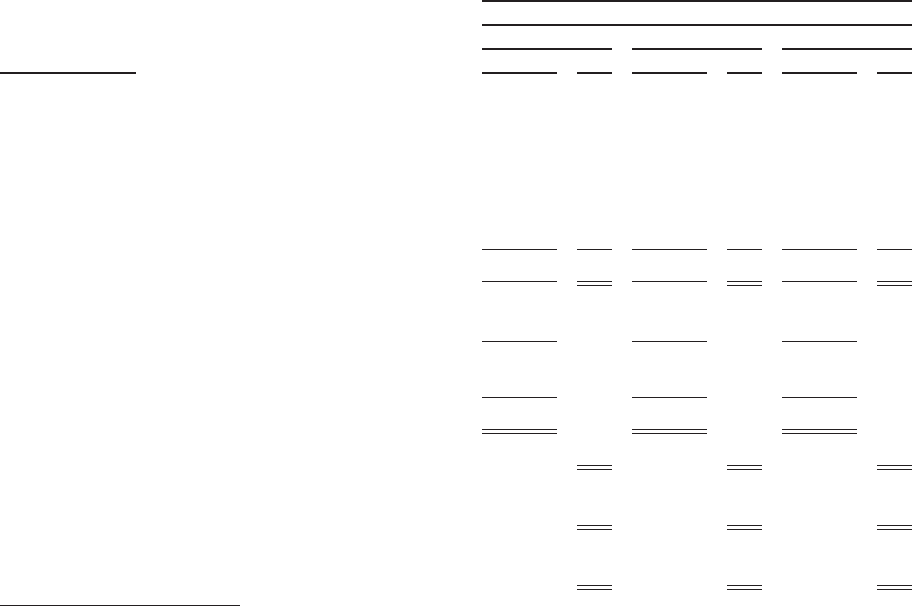

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

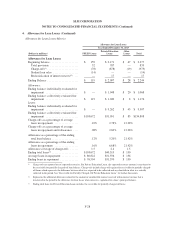

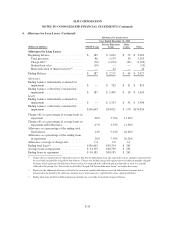

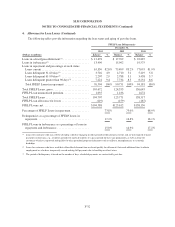

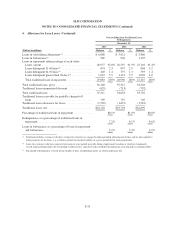

4. Allowance for Loan Losses (Continued)

The following tables provide information regarding the loan status and aging of past due loans.

FFELP Loan Delinquencies

December 31,

2013 2012 2011

(Dollars in millions) Balance % Balance % Balance %

Loans in-school/grace/deferment(1) .................. $ 13,678 $ 17,702 $ 22,887

Loans in forbearance(2) ........................... 13,490 15,902 19,575

Loans in repayment and percentage of each status:

Loans current ................................. 63,330 82.8% 75,499 83.2% 77,093 81.9%

Loans delinquent 31-60 days(3) ................... 3,746 4.9 4,710 5.2 5,419 5.8

Loans delinquent 61-90 days(3) ................... 2,207 2.9 2,788 3.1 3,438 3.7

Loans delinquent greater than 90 days(3) ............ 7,221 9.4 7,734 8.5 8,231 8.6

Total FFELP Loans in repayment ................. 76,504 100% 90,731 100% 94,181 100%

Total FFELP Loans, gross ......................... 103,672 124,335 136,643

FFELP Loan unamortized premium ................. 1,035 1,436 1,674

Total FFELP Loans .............................. 104,707 125,771 138,317

FFELP Loan allowance for losses ................... (119) (159) (187)

FFELP Loans, net ............................... $104,588 $125,612 $138,130

Percentage of FFELP Loans in repayment ............ 73.8% 73.0% 68.9%

Delinquencies as a percentage of FFELP Loans in

repayment ................................... 17.2% 16.8% 18.1%

FFELP Loans in forbearance as a percentage of loans in

repayment and forbearance ...................... 15.0% 14.9% 17.2%

(1) Loans for customers who may still be attending school or engaging in other permitted educational activities and are not required to make

payments on the loans, e.g., residency periods for medical students or a grace period for bar exam preparation, as well as loans for

customers who have requested and qualify for other permitted program deferments such as military, unemployment, or economic

hardships.

(2) Loans for customers who have used their allowable deferment time or do not qualify for deferment, that need additional time to obtain

employment or who have temporarily ceased making full payments due to hardship or other factors.

(3) The period of delinquency is based on the number of days scheduled payments are contractually past due.

F-32