Sallie Mae 2013 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

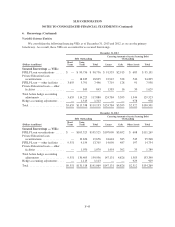

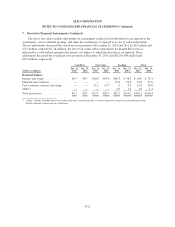

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

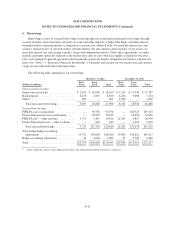

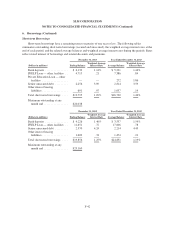

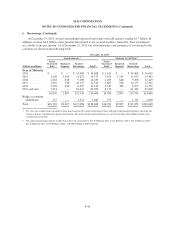

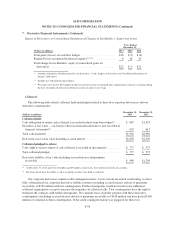

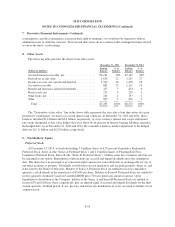

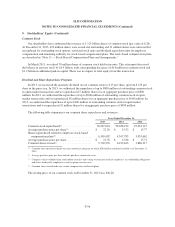

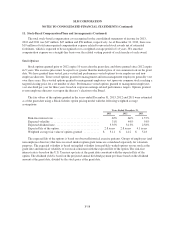

7. Derivative Financial Instruments (Continued)

Cash Flow Hedges

We use cash flow hedges to hedge the exposure to variability in cash flows for a forecasted debt issuance

and for exposure to variability in cash flows of floating rate debt. This strategy is used primarily to minimize the

exposure to volatility from future changes in interest rates. Gains and losses on the effective portion of a

qualifying hedge are recorded in accumulated other comprehensive income and ineffectiveness is recorded

immediately to earnings. In the case of a forecasted debt issuance, gains and losses are reclassified to earnings

over the period which the stated hedged transaction affects earnings. If we determine it is not probable that the

anticipated transaction will occur, gains and losses are reclassified immediately to earnings. In assessing hedge

effectiveness, generally all components of each derivative’s gains or losses are included in the assessment. We

generally hedge exposure to changes in cash flows due to changes in interest rates or total changes in cash flow.

Trading Activities

When derivative instruments do not qualify as hedges, they are accounted for as trading instruments where

all changes in fair value are recorded through earnings. We sell interest rate floors (Floor Income Contracts) to

hedge the embedded Floor Income options in student loan assets. The Floor Income Contracts are written options

which have a more stringent hedge effectiveness hurdle to meet. Specifically, our Floor Income Contracts do not

qualify for hedge accounting treatment because the pay down of principal of the student loans underlying the

Floor Income embedded in those student loans does not exactly match the change in the notional amount of our

written Floor Income Contracts. Additionally, the term, the interest rate index and the interest rate index reset

frequency of the Floor Income Contracts are different from that of the student loans. Therefore, Floor Income

Contracts do not qualify for hedge accounting treatment, and are recorded as trading instruments. Regardless of

the accounting treatment, we consider these contracts to be economic hedges for risk management purposes. We

use this strategy to minimize our exposure to changes in interest rates.

We use basis swaps to minimize earnings variability caused by having different reset characteristics on our

interest-earning assets and interest-bearing liabilities. These swaps possess a term of up to 13 years and are

primarily indexed to LIBOR or Prime rates. The specific terms and notional amounts of the swaps are determined

based on a review of our asset/liability structure, our assessment of future interest rate relationships, and on other

factors such as short-term strategic initiatives. Hedge accounting requires that when using basis swaps, the

change in the cash flows of the hedge effectively offset both the change in the cash flows of the asset and the

change in the cash flows of the liability. Our basis swaps hedge variable interest rate risk; however, they

generally do not meet this effectiveness criterion because the index of the swap does not exactly match the index

of the hedged assets. Additionally, some of our FFELP Loans can earn at either a variable or a fixed interest rate

depending on market interest rates and, therefore, swaps economically hedging these FFELP Loans do not meet

the criteria for hedge accounting treatment. As a result, these swaps are recorded at fair value with changes in fair

value reflected currently in the statement of income.

F-50