Sallie Mae 2013 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

3. Student Loans (Continued)

the loan. Forbearance does not grant any reduction in the total repayment obligation (principal or interest). While

in forbearance status, interest continues to accrue and is capitalized to principal when the loan re-enters

repayment status. Our forbearance policies include limits on the number of forbearance months granted

consecutively and the total number of forbearance months granted over the life of the loan. In some instances, we

require good-faith payments before granting forbearance. Exceptions to forbearance policies are permitted when

such exceptions are judged to increase the likelihood of collection of the loan. Forbearance as a collection tool is

used most effectively when applied based on a customer’s unique situation, including historical information and

judgments. We leverage updated customer information and other decision support tools to best determine who

will be granted forbearance based on our expectations as to a customer’s ability and willingness to repay their

obligation. This strategy is aimed at mitigating the overall risk of the portfolio as well as encouraging cash

resolution of delinquent loans.

Forbearance may be granted to customers who are exiting their grace period to provide additional time to

obtain employment and income to support their obligations, or to current customers who are faced with a

hardship and request forbearance time to provide temporary payment relief. In these circumstances, a customer’s

loan is placed into a forbearance status in limited monthly increments and is reflected in the forbearance status at

month-end during this time. At the end of the granted forbearance period, the customer will enter repayment

status as current and is expected to begin making scheduled monthly payments on a go-forward basis.

Forbearance may also be granted to customers who are delinquent in their payments. In these circumstances,

the forbearance cures the delinquency and the customer is returned to a current repayment status. In more limited

instances, delinquent customers will also be granted additional forbearance time.

During 2009, we instituted an interest rate reduction program to assist customers in repaying their Private

Education Loans through reduced payments, while continuing to reduce their outstanding principal balance. This

program is offered in situations where the potential for principal recovery, through a modification of the monthly

payment amount, is better than other alternatives currently available. Along with demonstrating the ability and

willingness to pay, the customer must make three consecutive monthly payments at the reduced rate to qualify

for the program. Once the customer has made the initial three payments, the loan’s status is returned to current

and the interest rate is reduced for the successive twelve month period.

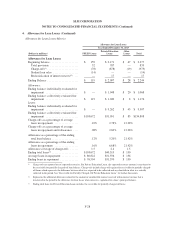

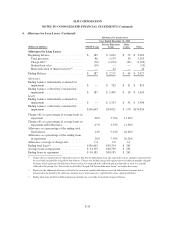

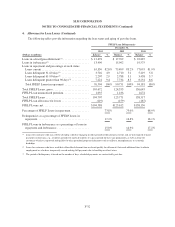

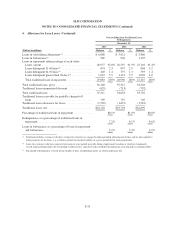

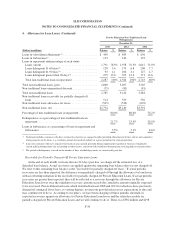

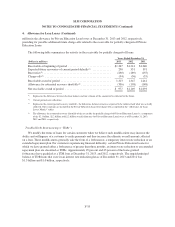

4. Allowance for Loan Losses

Our provisions for loan losses represent the periodic expense of maintaining an allowance sufficient to

absorb incurred probable losses, net of expected recoveries, in the held-for-investment loan portfolios. The

evaluation of the provisions for loan losses is inherently subjective as it requires material estimates that may be

susceptible to significant changes. We believe that the allowance for loan losses is appropriate to cover probable

losses incurred in the loan portfolios. We segregate our Private Education Loan portfolio into two classes of

loans — traditional and non-traditional. Non-traditional loans are loans to (i) customers attending for-profit

schools with an original Fair Isaac and Company (“FICO”) score of less than 670 and (ii) customers attending

not-for-profit schools with an original FICO score of less than 640. The FICO score used in determining whether

a loan is non-traditional is the greater of the customer or cosigner FICO score at origination. Traditional loans are

defined as all other Private Education Loans that are not classified as non-traditional.

F-27