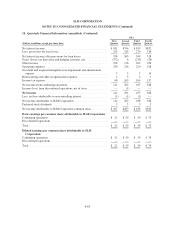

Sallie Mae 2013 Annual Report Download - page 227

Download and view the complete annual report

Please find page 227 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232

|

|

To be eligible, FFELP loans must meet the requirements of the HEA and regulations issued under the HEA.

Generally, these regulations require that lenders determine whether the applicant is an eligible borrower

attending an eligible institution, explain to borrowers their responsibilities under the loan, ensure that the

promissory notes evidencing the loan are executed by the borrower; and disburse the loan proceeds as required.

After the loan is made, the lender must establish repayment terms with the borrower, properly administer

deferrals and forbearances, credit the borrower for payments made, and report the loan’s status to credit reporting

agencies. If a borrower becomes delinquent in repaying a loan, a lender must perform collection procedures that

vary depending upon the length of time a loan is delinquent. The collection procedures consist of telephone calls,

demand letters, skiptracing procedures and requesting assistance from the guaranty agency.

A lender may submit a default claim to the guaranty agency after a student loan has been delinquent for at least

270 days. The guaranty agency must review and pay the claim within 90 days after the lender filed it. The

guaranty agency will pay the lender interest accrued on the loan for up to 450 days after delinquency. The

guaranty agency must file a reimbursement claim with ED within 45 days (reduced to 30 days July 1, 2006) after

the guaranty agency paid the lender for the default claim. Following payment of claims, the guaranty agency

endeavors to collect the loan. Guaranty agencies also must meet statutory and regulatory requirements for

collecting loans.

If ED determines that a guaranty agency is unable to meet its insurance obligations, the holders of loans

insured by that guaranty agency may submit claims directly to ED and ED is required to pay the full

reimbursements amounts due, in accordance with claim processing standards no more stringent than those

applied by the affected guaranty agency. However, ED’s obligation to pay reimbursement amounts directly in

this fashion is contingent upon ED determining a guaranty agency is unable to meet its obligations. While there

have been situations where ED has made such determinations regarding affected guaranty agencies, there can be

no assurances as to whether ED must make such determinations in the future or whether payments of

reimbursement amounts would be made in a timely manner.

Student Loan Discharges

FFELP Loans are not generally dischargeable in bankruptcy. Under the United States Bankruptcy Code, before

a student loan may be discharged, the borrower must demonstrate that repaying it would cause the borrower or

his family undue hardship. When a FFELP borrower files for bankruptcy, collection of the loan is suspended

during the time of the proceeding. If the borrower files under the “wage earner” provisions of the Bankruptcy

Code or files a petition for discharge on the ground of undue hardship, then the lender transfers the loan to the

guaranty agency which then participates in the bankruptcy proceeding. When the proceeding is complete, unless

there was a finding of undue hardship, the loan is transferred back to the lender and collection resumes.

Student loans are discharged if the borrower died or becomes totally and permanently disabled. A physician

must certify eligibility for a total and permanent disability discharge. Effective January 29, 2007, discharge

eligibility was extended to survivors of eligible public servants and certain other eligible victims of the terrorist

attacks on the United States on September 11, 2001.

If a school closes while a student is enrolled, or within 90 days after the student withdrew, loans made for that

enrollment period are discharged. If a school falsely certifies that a borrower is eligible for the loan, the loan may

be discharged. And if a school fails to make a refund to which a student is entitled, the loan is discharged to the

extent of the unpaid refund.

Rehabilitation of Defaulted Loans

ED is authorized to enter into agreements with the guaranty agency under which the guaranty agency may sell

defaulted loans that are eligible for rehabilitation to an eligible lender. For a loan to be eligible for rehabilitation

the guaranty agency must have received reasonable and affordable payments for 12 months (reduced to 9

payments in 10 months effective July 1, 2006), then the loans will be submitted to a lender, and only after the

A-4