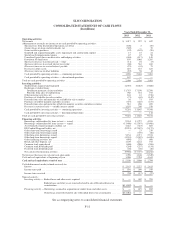

Sallie Mae 2013 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

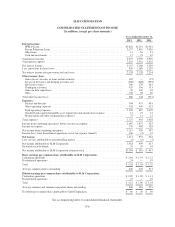

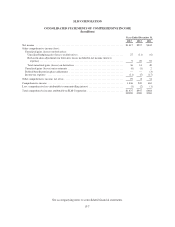

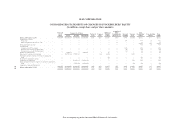

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. Significant Accounting Policies (Continued)

other inputs are used to model fair value such as prices of similar instruments, yield curves, volatilities,

prepayment speeds, default rates and credit spreads (including for our liabilities), relying first on observable data

from active markets. Depending on current market conditions, additional adjustments to fair value may be based

on factors such as liquidity, credit, and bid/offer spreads. Transaction costs are not included in the determination

of fair value. When possible, we seek to validate the model’s output to market transactions. Depending on the

availability of observable inputs and prices, different valuation models could produce materially different fair

value estimates. The values presented may not represent future fair values and may not be realizable.

We categorize our fair value estimates based on a hierarchical framework associated with three levels of

price transparency utilized in measuring financial instruments at fair value. Classification is based on the lowest

level of input that is significant to the fair value of the instrument. The three levels are as follows:

• Level 1 — Quoted prices (unadjusted) in active markets for identical assets or liabilities that we have

the ability to access at the measurement date. The types of financial instruments included in level 1 are

highly liquid instruments with quoted prices.

• Level 2 — Inputs from active markets, other than quoted prices for identical instruments, are used to

determine fair value. Significant inputs are directly observable from active markets for substantially the

full term of the asset or liability being valued.

• Level 3 — Pricing inputs significant to the valuation are unobservable. Inputs are developed based on

the best information available. However, significant judgment is required by us in developing the

inputs.

Loans

Loans, consisting primarily of federally insured student loans and Private Education Loans, that we have the

ability and intent to hold for the foreseeable future are classified as held-for-investment and are carried at

amortized cost. Amortized cost includes the unamortized premiums, discounts, and capitalized origination costs

and fees, all of which are amortized to interest income as further discussed below. Loans which are held-for-

investment also have an allowance for loan loss as needed. Any loans we have not classified as held-for-

investment are classified as held-for-sale, and carried at the lower of cost or fair value. Loans are classified as

held-for-sale when we have the intent and ability to sell such loans. Loans which are held-for-sale do not have

the associated premium, discount, and capitalized origination costs and fees amortized into interest income. In

addition, once a loan is classified as held-for-sale, there is no further adjustment to the loan’s allowance for loan

losses that existed immediately prior to the reclassification to held-for-sale.

As market conditions permit, we may securitize loans as a source of financing for those loans. If we elect to

use a securitization program to finance loans, loans are selected based on the required characteristics to structure

the desired transaction at the most favorable financing terms (e.g., type of loan, mix of interim vs. repayment

status, credit rating and maturity dates). Due to some of the structuring terms, certain transactions may qualify for

sale treatment while others do not qualify for sale treatment and are recorded as financings. All of our student

loans are initially categorized as held-for-investment until there is certainty as to each specific loan’s ultimate

financing because we do not securitize all loans and currently all of our securitizations do not qualify for sale

treatment. It is only when we have selected the loans to securitize and that securitization transaction qualifies as a

sale do we transfer the loans into the held-for-sale classification and carry them at the lower of cost or fair value.

If we anticipate recognizing a gain related to the impending securitization, then the fair value of the loans is

higher than their respective cost basis and no valuation allowance is recorded.

F-14