Sallie Mae 2013 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2013 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

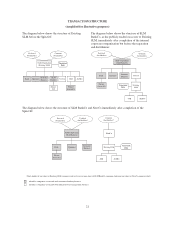

Other Significant Sources of Regulation

Many aspects of our businesses are subject to regulation by federal and state regulation and administrative

oversight. Some of the most significant of these are described below.

HEA

We are subject to the HEA and our student loan operations are periodically reviewed by ED and Guarantors.

As a servicer of federal student loans, we are subject to ED regulations regarding financial responsibility and

administrative capability that govern all third-party servicers of insured student loans. In connection with our

servicing operations, we must comply with, on behalf of Guarantor clients, ED regulations that govern Guarantor

activities as well as agreements for reimbursement between ED and our Guarantor clients.

Federal Financial Institutions Examination Council

As a third-party service provider to financial institutions, we are also subject to examination by the Federal

Financial Institutions Examination Council (the “FFIEC”). The FFIEC is a formal interagency body of the U.S.

government empowered to prescribe uniform principles, standards, and report forms for the federal examination

of financial institutions by the FRB, the FDIC, the National Credit Union Administration, the Office of the

Comptroller of the Currency and the CFPB and to make recommendations to promote uniformity in the

supervision of financial institutions.

Consumer Protection and Privacy

Our originating and servicing of federal and Private Education Loans and our debt collection and

receivables management activities subject us to federal and state consumer protection, privacy and related laws

and regulations. Some of the more significant laws and regulations that are applicable to our business include:

• various laws governing unfair, deceptive or abusive acts or practices;

• the federal Truth-In-Lending Act and Regulation Z issued by the FRB, which governs disclosures of

credit terms to consumer borrowers;

• the Fair Credit Reporting Act and Regulation V issued by the FRB, which governs the use and provision

of information to consumer reporting agencies;

• the ECOA and Regulation B issued by the FRB, which prohibits discrimination on the basis of race, creed

or other prohibited factors in extending credit;

• the SCRA, which applies to all debts incurred prior to commencement of active military service

(including education loans) and limits the amount of interest, including service and renewal charges and

any other fees or charges (other than bona fide insurance) that are related to the obligation or liability;

• the Fair Debt Collection Act, which governs the manner in which consumer debts may be collected by

collection agencies;

• the Truth in Savings Act and Regulation DD issued by the FRB, which requires disclosure of deposit

terms to consumers;

• Regulation CC issued by the FRB, which relates to the availability of deposit funds to consumers;

• the Right to Financial Privacy Act, which imposes a duty to maintain the confidentiality of consumer

financial records and prescribes procedures for complying with administrative subpoenas of financial

records;

• the Electronic Funds Transfer Act and Regulation E issued by the FRB, which governs automatic deposits

to and withdrawals from deposit accounts and customers’ rights

17