Wells Fargo 2008 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

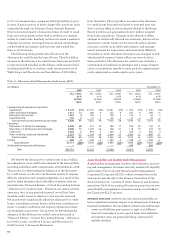

behind a Wells Fargo first mortgage and segregated these

indirect loans into a liquidating portfolio. As previously dis-

closed, while the $11.9 billion of loans in this liquidating port-

folio represented about 3% of total loans outstanding at

December 31, 2007, these loans represented the highest risk

in our $84.2 billion Home Equity portfolio. The loans in the

liquidating portfolio were primarily sourced through whole-

sale (brokers) and correspondents. Additionally, they are

largely concentrated in geographic markets that have experi-

enced the most abrupt and steepest declines in housing

prices. We continued to provide home equity financing

directly to our customers, but stopped originating or acquir-

ing new home equity loans through indirect channels unless

they are behind a Wells Fargo first mortgage and have a

combined loan-to-value ratio lower than 90%. We also experi-

enced increased net charge-offs in our unsecured consumer

portfolios, such as credit cards and lines of credit, in part due

to growth and in part due to increased economic stress in

households.

Full year 2007 auto portfolio net charge-offs were $1.02 bil-

lion (3.45% of average loans), compared with $857 million

(3.15%) in 2006. These results were consistent with our expec-

tations and reflected planned lower growth in originations and

an improvement in collection activities within this business.

The provision for credit losses was $4.94 billion in 2007,

an increase of $2.74 billion from $2.20 billion in 2006, due to

higher net charge-offs and the 2007 credit reserve build of

$1.4 billion, primarily for higher net loss content that we esti-

mated in the Home Equity portfolio. The allowance for credit

losses, which consists of the allowance for loan losses and the

reserve for unfunded credit commitments, was $5.52 billion

(1.44% of total loans) at December 31, 2007, compared with

$3.96 billion (1.24%) at December 31, 2006.

At December 31, 2007, total nonaccrual loans were

$2.68 billion (0.70% of total loans) up from $1.67 billion (0.52%)

at December 31, 2006. The majority of the increase in nonac-

crual loans was concentrated in the first mortgage portfolio

($209 million in Wells Fargo Home Mortgage and $343 million

in Wells Fargo Financial) and was due to the national rise in

mortgage default rates. Total NPAs were $3.87 billion (1.01% of

total loans) at December 31, 2007, compared with $2.42 billion

(0.76%) at December 31, 2006. Due to illiquid market conditions,

we are now holding more foreclosed properties than we have

historically. Foreclosed assets were $1.18 billion at December 31,

2007, compared with $745 million at December 31, 2006.

Foreclosed assets, a component of total NPAs, included

$649 million and $423 million in residential property and auto

loans, and $535 million and $322 million of foreclosed real

estate securing GNMA loans at December 31, 2007 and 2006,

respectively, consistent with regulatory reporting require-

ments. The foreclosed real estate securing GNMA loans of

$535 million represented 14 basis points of the ratio of NPAs

to loans at December 31, 2007. Both principal and interest

for the GNMA loans secured by the foreclosed real estate are

collectible because the GNMA loans are insured by the FHA

or guaranteed by the Department of Veterans Affairs.

The Company and each of its subsidiary banks remained

“well capitalized” under applicable regulatory capital adequa-

cy guidelines. The ratio of common stockholders’ equity to

total assets was 8.28% at December 31, 2007, compared with

9.51% at December 31, 2006. Our total RBC ratio at December

31, 2007, was 10.68% and our Tier 1 RBC ratio was 7.59%,

exceeding the minimum regulatory guidelines of 8% and 4%,

respectively, for bank holding companies. Our RBC ratios at

December 31, 2006, were 12.49% and 8.93%, respectively. Our

Tier 1 leverage ratios were 6.83% and 7.88% at December 31,

2007 and 2006, respectively, exceeding the minimum regula-

tory guideline of 3% for bank holding companies.

Risk Factors

An investment in the Company involves risk, including the

possibility that the value of the investment could fall substan-

tially and that dividends or other distributions on the invest-

ment could be reduced or eliminated. We discuss below and

elsewhere in this Report, as well as in other documents we

file with the SEC, risk factors that could adversely affect our

financial results and condition and the value of, and return

on, an investment in the Company. We refer you to the

Financial Review section and Financial Statements (and

related Notes) in this Report for more information about

credit, interest rate, market and litigation risks, and to the

“Regulation and Supervision” section of our 2008 Form 10-K

for more information about legislative and regulatory risks.

Any factor described below or elsewhere in this Report or in

our 2008 Form 10-K could by itself, or together with other fac-

tors, adversely affect our financial results and condition.

Refer to our quarterly reports on Form 10-Q filed with the

SEC in 2009 for material changes to the discussion of risk

factors. There are factors not discussed below or elsewhere in

this Report that could adversely affect our financial results

and condition.

In accordance with the Private Securities Litigation Reform

Act of 1995, we caution you that one or more of these same

risk factors could cause actual results to differ significantly

from projections or forecasts of our financial results and con-

dition and expectations for our operations and business that

we make or express in forward-looking statements in this

Report and in presentations and other Company communica-

tions. We make forward-looking statements when we use

words such as “believe,” “expect,” “anticipate,” “estimate,”

“project,” “forecast,” “will,” “may,” “can” and similar expres-

sions. Do not unduly rely on forward-looking statements, as

actual results could differ significantly. Forward-looking

statements speak only as of the date made, and we do not