Wells Fargo 2008 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

We use four key variables to calculate our annual pension

cost: size and characteristics of the employee population,

actuarial assumptions, expected long-term rate of return on

plan assets, and discount rate. We describe below the effect

of each of these variables on our pension expense.

SIZE AND CHARACTERISTICS OF THE EMPLOYEE POPULATION

Pension expense is directly related to the number of employ-

ees covered by the plans, and other factors including salary,

age and years of employment.

ACTUARIAL ASSUMPTIONS To estimate the projected benefit

obligation, actuarial assumptions are required about factors

such as the rates of mortality, turnover, retirement, disability

and compensation increases for our participant population.

These demographic assumptions are reviewed periodically.

In general, the range of assumptions is narrow.

EXPECTED LONG-TERM RATE OF RETURN ON PLAN ASSETS We

determine the expected return on plan assets each year based

on the composition of assets and the expected long-term rate

of return on that portfolio. The expected long-term rate of

return assumption is a long-term assumption and is not

anticipated to change significantly from year to year.

To determine if the expected rate of return is reasonable,

we consider such factors as (1) long-term historical return

experience for major asset class categories (for example,

large cap and small cap domestic equities, international

equities and domestic fixed income), and (2) forward-looking

return expectations for these major asset classes. Our expected

rate of return for 2009 is 8.75%, the same rate used for 2008

and 2007. Differences in each year, if any, between expected

and actual returns are included in our net actuarial gain or

loss amount, which is recognized in other comprehensive

income. We generally amortize any net actuarial gain or loss

in excess of a 5% corridor (as defined in FAS 87) in net peri-

odic pension expense calculations over the next five years.

Due to the dramatic downturn in market conditions during

2008, our actual rate of return for 2008 was negative, and was

therefore significantly less than our long-term expected rate

of return of 8.75%. This difference will increase our 2009 pen-

sion expense by approximately $600 million due to higher

actuarial loss amortization combined with a lower rate of

return component of pension expense, as compared to our

2008 pension expense. Although our plan assets experienced

a negative return in 2008, our plan assets have earned an

average annualized rate of return of about 9% over the last

25 years. Our average remaining service period is approxi-

mately 10 years. See Note 20 (Employee Benefits and Other

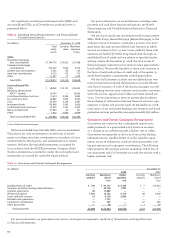

Expenses) to Financial Statements for information on funding,

changes in the pension benefit obligation, and plan assets

(including the investment categories, asset allocation and

the fair value).

If we were to assume a 1% increase/decrease in the expected

long-term rate of return, holding the discount rate and other

actuarial assumptions constant, 2009 pension expense would

decrease/increase by approximately $74 million.

DISCOUNT RATE We use a discount rate to determine the pre-

sent value of our future benefit obligations. The discount rate

reflects the current rates available on long-term high-quality

fixed-income debt instruments, and is reset annually on the

measurement date. To determine the discount rate, we

review, with our independent actuary, spot interest rate yield

curves based upon yields from a broad population of high-

quality bonds, adjusted to match the timing and amounts of

the Cash Balance Plan’s expected benefit payments. We used

a discount rate of 6.75% in 2008 and 6.25% in 2007.

If we were to assume a 1% increase in the discount rate,

and keep the expected long-term rate of return and other

actuarial assumptions constant, pension expense would

decrease by approximately $72 million. If we were to assume

a 1% decrease in the discount rate, and keep other assump-

tions constant, 2009 pension expense would increase by

approximately $70 million. The decrease in pension expense

due to a 1% increase in discount rate differs slightly from the

increase in pension expense due to a 1% decrease in discount

rate due to the impact of the 5% gain/loss corridor.

Income Taxes

We are subject to the income tax laws of the U.S., its states

and municipalities and those of the foreign jurisdictions in

which we operate. We account for income taxes in accor-

dance with FAS 109, Accounting for Income Taxes, as inter-

preted by FIN 48, Accounting for Uncertainty in Income Taxes.

Our income tax expense consists of two components: current

and deferred. Current income tax expense approximates

taxes to be paid or refunded for the current period and

includes income tax expense related to our uncertain tax

positions. We determine deferred income taxes using the bal-

ance sheet method. Under this method, the net deferred tax

asset or liability is based on the tax effects of the differences

between the book and tax bases of assets and liabilities, and

recognized enacted changes in tax rates and laws in the peri-

od in which they occur. Deferred income tax expense results

from changes in deferred tax assets and liabilities between

periods. Deferred tax assets are recognized subject to man-

agement’s judgment that realization is “more likely than not.”

Uncertain tax positions that meet the more likely than not

recognition threshold are measured to determine the amount

of benefit to recognize. An uncertain tax position is measured

at the largest amount of benefit that management believes is

greater than 50% likely of being realized upon settlement.

Foreign taxes paid are generally applied as credits to reduce

federal income taxes payable. We account for interest and

penalties as a component of income tax expense.

The income tax laws of the jurisdictions in which we oper-

ate are complex and subject to different interpretations by

the taxpayer and the relevant government taxing authorities.

In establishing a provision for income tax expense, we must

make judgments and interpretations about the application of

these inherently complex tax laws. We must also make esti-

mates about when in the future certain items will affect tax-

able income in the various tax jurisdictions by the govern-